While several versions of the so-called efficient market hypothesis (EMH) have lost many adherents in recent years, the opposite proposition—that the market is definitely not totally stupid—is clearly valid. This is crucial for investors to remember when investing for yield.

Higher current yield reflects greater risk. This is true across asset types and among securities within the same type. Investors who chase yield are gambling, knowingly or naively, that the market is wrong and that their principal will not be significantly impaired. In the current artificial low-yield climate, risk to capital is real but is being ignored more than usual, as investors seek to replicate the income streams available pre-2007.

This article covers several income-oriented asset types: high-yield bonds, preferred stocks, so-called hybrid preferreds, real estate investment trusts (REITs), master limited partnerships (MLPs), closed-end funds and utility common stocks. While the capital soundness differs by asset type, one key caution is equally true for all: High yield means high risk.

Unfortunately, some securities salespeople gravitate to high-yield offerings since they are an ‘easy sell’ to clients, who seldom ask penetrating questions about attendant risks. Such pitches should be refused, as they are clues to the offerers’ character. The aftermarket, readily accessed via numerous screening tools, can be just as dangerous for do-it-yourself investors without a salesperson making titillating offers.

High-Yield Bonds

Wall Street avoids use of the unappealing term “junk,” but it is appropriate. Rating agencies have had some bad press lately, and their calls are sometimes backward-focused. But when a security is already assigned a lower grade, the rating should be heeded. Other bonds are unrated, and in such cases their yield will signal likely danger.

There is almost never any free lunch in terms of high yield. Issuers, whether corporate or sovereign, do not issue bonds with high interest rates because they feel generous or kind. High coupon rates exist because the market has demanded them (think Greece versus Germany). When an issuer’s credit quality deteriorates, prices must fall as the apparent yield demanded by savvy buyers and holders rises.

Over several decades and business cycles, roughly 5% of outstanding junk bonds default in a typical year. Some will go to zero in bankruptcy, while others (after considerable delay) may pay back some or all of principal and/or interest. In the tech-bubble recession, corporate junk-bond defaults hit 12% for two years running.

A study by fund rating firm Lipper showed that the total return on high-yield bond funds was only 0.25% higher than that on all U.S. government bond funds (for the 20-year period ended in 1995). Surely that was inadequate premium income for the risk taken! The so-called risk premium above Treasury rates was well below average as of May 2013, because the economy has been improving and because investors are reaching for yield.

Historically, junk bond prices follow stocks rather than quality bonds because lower-quality issuers are more economically sensitive. An individual investor must be an exceptional analyst of economic and corporate trends (including the future trends) to choose junk bonds successfully.

Preferred Stocks

Two major types of straight (nonconvertible) preferred stocks exist: traditional preferreds and so-called hybrid preferreds. An excellent free website covering details on publicly traded preferred stocks is QuantumOnline (www.quantumonline.com). It not only summarizes key information such as callability and redemption dates, but in many cases it allows users to click through to an electronic copy of the original prospectus—a rare and often elusive document. [QuantumOnline.com requires visitors to register, but registration is free.]

Hybrid preferreds have extremely thick prospectuses because they are highly complex. Most pay notably above-market cash yields—that itself should be a flag. Often there are automatic-conversion provisions that will turn your holding into common stock and end the high preferred-dividend stream. The conversion usually creates not only a reduction of income, but also a loss of capital, unless the shares of the common stock have risen by a huge percentage. Also, the complex structure of these hybrid issues means they produce interest income (taxable at the holder’s full marginal rate) rather than qualified dividends. QuantumOnline indicates the tax status of income. The high apparent yields offered by hybrids should warn investors to avoid the group.

Conventional preferred stocks stand below bonds and above common stocks in terms of claims on the issuer’s assets and income stream. While preferred stock carries an indenture, its promise is weaker than that of a bond. Preferred stock dividends must be declared by a corporation’s board of directors each quarter. While preferred stock dividends do come before any common stock dividends, they are by no means automatic or guaranteed. Prudence says to look closely at the earnings and dividend records to sense how strong the preferred stock dividend may be.

As to ratings, the aforementioned comments regarding bonds apply equally here. In the present low-yield climate, an investor must also beware of call dates. Most creditworthy issuers are calling preferreds when possible for two reasons: Issuers can refinance at lower cost; and debt interest (presently very low) is tax deductible, while preferred dividends are not.

Carefully calculate the overall net yield-to-call date, using the bond yield-to-maturity formula, on any preferred stock you are considering or already hold. [Yield to maturity measures what you will earn from all possible cash flows. The calculation can be complex, but several websites offer free yield-to-maturity calculators, such as Fidelity.com at https://powertools.fidelity.com/fixedincome/yield.do.]

A high cash yield for a preferred stock in an otherwise low-yield market indicates a risk of a near-term call and/or low quality. The market is not stupid, so expect that what seems too good to be true to be exactly that.

Real Estate Investment Trusts (REITs)

A REIT is a special corporate structure under the IRS code. Qualifying companies pay no federal corporate income tax provided they pass through to shareholders essentially all their otherwise taxable income and capital gains each year. Therefore, REITs tend to yield more than other common stocks. In the reach for yield during recent years, REITs have become quite popular, and many mutual funds, ETFs and closed-end funds have been created to own them, further raising demand and thus lowering yields.

REITs fall broadly into two major types: equity (owning properties) and debt (making loans on real estate or holding realty-backed debt). Both types use leverage (as homeowners do in buying a house), but the debt-type REITs carry leverage to levels that in some cases would make now-failed banks blush. With both types of REITs, investors must look at the distribution rate as definitely not being guaranteed and in no way comparable to that of a bond or even a preferred stock. Dividends are declared every quarter based on business outlook and the ability to pay.

Fortunately, the low interest rates in recent years have allowed all creditworthy REITs to reduce interest cost (both from corporate bonds, if any, and mortgages on property held), so debt coverage has improved. Nevertheless, an investor should look carefully at debt-to-capital ratios and debt-maturity schedules before buying a REIT. Compare to those for comparable REITs—ones in the same type of business.

Type and location of property also affect risk. For example, a firm owning warehouses is at greater risk of tenant vacancy or default than one that owns and operates storage-garage facilities. You as an investor must balance your sense of relative business risk (which may change over time) in light of the relative yields offered by the REITs.

Generally, I resolutely require that a REIT raises its distribution at least once a year, or I will look elsewhere in the population of about 200. A rising payment stream has two advantages: It not only shows that the business is in improving health, but it also creates an automatic annual-review date for shareholders. If a REIT raises its dividend each fourth quarter, for example, an annual signal of whether things are still fine is established.

Mortgage or debt-holding REITs pose special issues and must be regarded with extreme caution at present. If you have any doubt about a REIT’s assets, a quick check of its corporate website, or the online corporate profile offered by many financial sites, will give you the important figures. Another excellent clue is the yield on its shares. Anything in or near double digits should be a red flag.

Mortgage REITs are special favorites of investors who grab for high yield without understanding the accompanying risks. Do not be self-deluded! A typical mortgage REIT owns paper yielding about 5% on average, with its higher-rate loans being paid off as creditworthy homeowners refinance. How can its stock pay a yield of 10%, 12% or more? Through the “magic” of leverage. If the REIT borrows enough money at today’s short-term rates (plus or minus 1% in late April 2013), it can create a positive spread between its asset returns (5%, in this example) and the cost of its capital.

Two things can go wrong: Short-term rates eventually will stop being held low by the Federal Reserve, or long-term rates will rise due to inflation or a healthier economy. Both could also happen. When short-term rates do rise, the REIT will have reduced earnings per share and the dividend will be reduced. Shares will fall in price, giving holders a capital loss. A third thing could go wrong, too: The underlying mortgages go into default. (This was viewed as being unthinkable until 2008.)

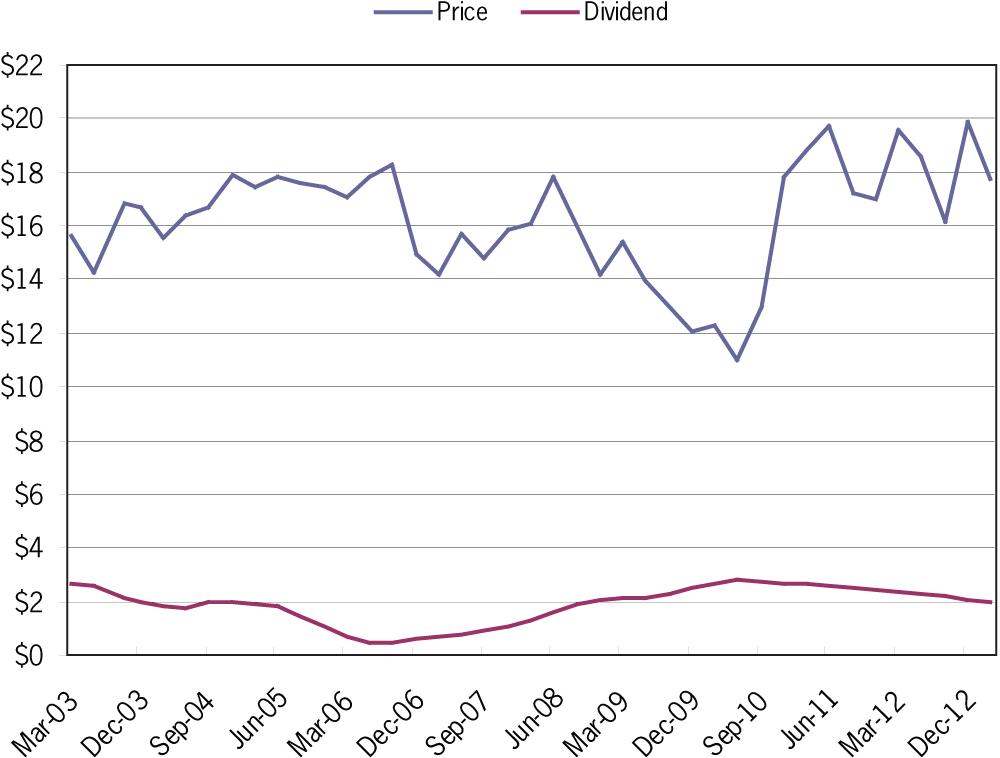

A long-term chart history of the largest mortgage REIT, Annaly Capital Management Inc. (NLY), is something every investor should examine before considering any mortgage REIT’s stock. The dividend you get at any time from this or any REIT is not guaranteed, as Figure 1 shows. Do not think of an REIT’s dividend like bond interest! I expect further reductions in common dividends here and from other mortgage REITs, as interest rates move as described above. Your income will fall, and your principal will shrink.

*Share prices are as of ex-dividend dates, from March 27, 2003, through March 27, 2013. Rolling dividends, calculated as the cumulative dividend paid for the current and previous three quarters, are displayed. Sources: Annaly Capital Management and Yahoo! Finance.

I recommend BigCharts.com (www.bigcharts.com) for analyzing prices and dividend history, though other good sites may be available. Using the advanced charts feature on Big Charts, you can plot earnings per share and dividends for 10 years or more, right under the stock price chart.

A final note about REITs (which I like, but which are not the simplest assets): Many investors enjoy the distribution stream from their REITs because typically a large portion of the payment is considered a return of capital for IRS purposes and therefore not taxed under current tax laws. As with any investment, return of capital decreases the owner’s cost basis. So upon sale, there is a capital gain to be taxed. And politics will determine future capital gains rates. Many investors prefer to own REITs in their tax-deferred or tax-free (Roth IRA) accounts to lower their current tax liability.

Master Limited Partnerships (MLPs)

There are broadly two pure MLP types: One primarily harvests assets (oil, gas, timber), and a second acts as mainly a transporter (pipeline). But there is a third variety that performs a mix of functions. Those that harvest assets have higher risk and potentially higher reward, since their profits and probably their distributions will vary with the quantity of product produced and the price of a product. These typically trade at higher yields than the pipelines, which are mainly toll collectors. Within the asset-harvesting types, proven reserves and their locations will be major drivers of perceived desirability and therefore price and yield.

Generally, an investor can expect a steady or gradually rising distribution pattern from the pipeline type of MLPs. Their profit fluctuates mildly with the overall economy, and demand for energy has tended to rise over time. Here, I would apply my rule of requiring an annual increase in payments as a criterion for buying or holding, as there are competitors available that do pass the test.

The same is not true for the resource-owning MLPs, however. They hope not to cut dividend rates, but a prolonged period of low prices or falling production may force unfavorable action by directors. In both cases, fortunately, significant non-cash charges such as depreciation or depletion create cash flow beyond reported earnings, possibly cushioning payouts during slack times.

The market factors in all these uncertainties and generally demands a higher cash yield from MLPs whose business models are more risky—those that produce resources. So an investor should not assume the latest distribution rate represents a future guarantee. The degree of debt financing can also affect the dependability of payments. Either business prudence or contractual loan terms can sometimes force cuts in distribution rates if business goes soft. The more leverage, the greater the risk. The bottom line for investors is, again, that high yield has a meaning and one should reach for it only after having carefully studied and decided to accept the attendant risks.

As with REITs, distributions from MLPs usually include significant returns of capital and the cost basis is reduced accordingly upon sale. Also, MLPs generate K-1 tax documents with mild resulting filing complexity, rather than 1099 income as from a REIT, and reporting often runs well into March or later, creating stress and a last-minute rush in filing taxes. This is one reason many investors and some institutions avoid MLPs, creating an inefficient (low-demand) market, which raises yield. There is one other important tax warning regarding MLPs: The IRS code imposes an unrelated business income tax on qualified retirement accounts that earn $1,000 or more in reported K-1 income, and losses do not offset gains. For this reason holding MLPs in an IRA or similar vehicle is risky; consult your personal tax adviser!

Taxation-Risk Issues for REITs and MLPs

Washington is looking for revenue, and anything that focuses on higher-income households seems a target as a “loophole.” Thus, REITs and MLPs might be at risk for a change in taxation, with taxes imposed at the corporate level.

In at least the near term, it will be argued by strong lobbies that changing the rules would cost jobs, and assets would be priced down because distribution rates would be reduced. That scenario played out in Canada in 2011 when (less long-established) royalty trust tax rules were repealed.

In a balanced-power Congress, I believe the worst fate for REITs and MLPs might be a grandfathering of the present tax rules for existing entities, and reduced or eliminated tax benefits for any newly created entities. However, watch the 2014 election polls in advance: If the president’s party were to win both houses of Congress, the odds of getting comprehensive tax reform legislation passed improve.

Closed-End Funds

Most recently issued closed-end funds (CEFs) at least begin their lives with “managed” or flat-distribution policies, typically offering the investor about an 8% annual cash return. This structure helps Wall Street market new closed-end funds, and the high yields tend to cushion the prices from falling sharply in the aftermarket. The problem is that underlying securities in the funds cannot dependably pay 8% (or more, before expenses).

There are two ways to continue high distributions: Use leverage as REITs do (although much lower rates are allowed under Securities and Exchange Commission rules for closed-end funds), or pay out more than is being earned.

Excess distributions by nature reduce assets per share in a fund. Such a process becomes increasingly untenable over multiple years. Imagine a fund earning $0.60 per share on a starting $10 asset base, but paying $1.00 annually. The net asset value (NAV) per share is depleted by $0.40 per year, making it increasingly impossible to earn the starting amount, and raising the unearned deficit over time. The eventual likely outcome is a cut in payments, which will also slash the market price, a double whammy.

Once again, reaching for high yield is a recipe for high risk and probable loss. The website CEF Connect (www.cefconnect.com) is an excellent resource for data on closed-end funds; one figure that is updated quarterly and can signal likelihood of future trouble is found under the Distributions tab at a fund’s page: undistributed net investment income per share (UNII/share).

Utility Common Stocks

As with other investments providing current yield, utility stocks have risen in price and declined in yield in recent years as investors have sought alternatives to government bonds, whose yields are now negative after taxes and inflation. Here again, the temptation is to reach for the higher-yielding utilities, but, predictably, this means taking on the risk of a dividend cut. Many analysts advise watching the payout ratio (dividend rate divided by latest earnings per share) of utilities as a good warning device. My caution would be that utility earnings can vary considerably across all types because of regulatory lags regarding allowed rates, and earnings of gas and electric companies can fluctuate notably with the weather.

The rubric of requiring at least an annual dividend increase is important. It shows the firm is still healthy in directors’ eyes, and it provides a scheduled “annual checkup” as a signal for investors. Dozens of utilities pass this test, and while they trade at lower percentage yields (less risk) than those with flat dividends, they are safer and more likely to provide future price appreciation driven by rising dividends.

One utility group in particular is of major current concern: telephone stocks. The phone business is commoditized and subject to price wars. People eventually can spend only a limited amount of hours (and money) texting, downloading and grabbing songs. The time limit may be reached soon. Check out the available stock list: Most are losing money, and those with positive earnings per share are paying out more than they earn, or nearly all [e.g., AT&T Inc. (T) and Verizon Communications Inc. (VZ)].

This spring’s casualty was CenturyLink Inc. (CTL), whose earnings have declined despite economic recovery. Its board cut the annual dividend from $2.90 per share to $2.16 per share. A wise investor could see it coming: Why would CenturyLink yield over 7% while AT&T and Verizon returned 4.5% to 5%? CenturyLink’s stock dropped from $42 to $32 on the news. A nearly 25% capital loss wipes out many years of approximately 2% higher yield!

Here is another example: Since 2010, Frontier Communications Corp. (FTR) has twice cut its payments—from $1.00 per share to $0.75 per share—and now pays $0.40 per share annually. In five years its stock has fallen from over $12 to $4 recently. The high yield (still 9.8%!) was only apparently as high as the numbers said. Once again, the market is not stupid. Investors playing the yield-reach game got burned.

Relative quality, and therefore income and capital safety, can also be seen in local pairs of electric companies. Look at 10-year charts, including dividends, for NextEra Energy Inc. (NEE) and TECO Energy Inc. (TE) in Florida, and UNS Energy Corp. (UNS) and Pinnacle West Capital Corp. ![]() (PNW) in Arizona. Relative yield always tells the tale of risk.

(PNW) in Arizona. Relative yield always tells the tale of risk.

Conclusion

Table 1 summarizes the key considerations and strategy for each security type covered here.

The market, while not reliably efficient, is not dependably stupid. Income vehicles trading at higher yields within their asset classes do so because of greater risk—of reduced income payments and the underlying asset price.

| Instrument | Considerations | Strategy/Action | |

| High-Yield Bonds* | • These correlate with stocks | • Sell/avoid | |

|

|

• Best bought when economy has been in recession a while | • Not long-term holds | |

| Preferred Stocks* | • Closely watch call dates | • Don’t pay more than two dividends over par | |

| Hybrid Preferreds* | • Adverse auto-convert rules | • Sell/avoid | |

| REITs: Mortgage* | • Mortgage REITs’ dividends ends will be cut if short-term rates rise | • Avoid the tempting high-yield trap | |

| REITs: Equity* | • Annual dividend growth is a MUST | • Selective buy/hold | |

| MLPs* | • Annual dividend growth is a MUST | • Selective buy/hold | |

|

|

• Producers reflect oil and gas prices | • Depends on opinion of energy prices | |

| Telecommunication Utilities* | • Commoditized; high payouts | • Avoid | |

| Electric & Gas Utilities* | • Annual dividend growth is a MUST | • Avoid when rates rise | |

| Closed-End Funds | • Discounts will widen as short-term rates rise or stocks fall | • Don’t pay premiums | |

| • Managed distributions not sure bet | • Avoid most | ||

| *Considerations and actions also apply to exchange-traded funds (ETFs) and mutual funds of this type. | |||

It is tempting but very risky to reach for yield. In some future business downturn, companies seeming to offer higher yields now are most at risk of reducing or skipping their payouts. Unless an investor is unusually prescient and adept at selling or has proven skills at finding lasting bargains among depressed securities, yield chasing is a losing game.

If you need more income than the present rate environment allows, accept lower yield with safety and growth, and sell off a couple of percent of assets annually as an income supplement. Always avoid yield chasing.

Discussion

FREE REPORT

Get your free copy of our special

report analyzing the tech stocks

most likely to outperform the

market.

James Vanek from AZ posted over 13 years ago:

Fernando Robles from FL posted over 13 years ago:

Fernando Robles from FL posted over 13 years ago:

Erik Rosaen from MI posted over 13 years ago:

Kenneth Smith from NJ posted over 13 years ago:

Robert Albers from IL posted over 13 years ago:

Robert Hardy from MI posted over 13 years ago:

David Fulcher from KY posted over 13 years ago:

Mary Niedermeier from WI posted over 13 years ago:

Ryan James from AL posted over 13 years ago:

Henry Hanau from NY posted over 13 years ago:

M Hinnant from GA posted over 13 years ago:

Patrick Calby from IL posted over 12 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account