{kind=link}

Related

Retirement Planning

by John Sweeney | April 2013

If you’re retired—or nearing it—ensuring that your retirement investment portfolio lasts your lifetime is critical. And that’s not easy because by nature the stock market is volatile. What if a market downturn takes a bite out of your investment portfolio?

While you cannot completely control the market’s impact on your portfolio, there are things you can control that can also make a significant difference in how long your portfolio may last. One: your withdrawal rate from your portfolio. The amount you take can directly impact how long your assets could last in retirement.

But what about in difficult markets? At Fidelity, we still believe in inflation-adjusted withdrawal rates of no more than 4% to 5% a year for individuals who retire at age 65. That’s because we did the analysis using our Retirement Income Planner and an inflation-adjusted withdrawal rate of more than 5% steeply increased the risk of depleting retirement savings during an investor’s lifetime. We also ran some further analysis to determine the influence of different market environments.

[Editor’s note: Fidelity’s Retirement Income Planner is an educational tool developed and offered for use by Strategic Advisers Inc., a registered investment adviser and a Fidelity Investments company. The online tool can be accessed at https://personal.fidelity.com/planning/retirement/income_planner.shtml and is free, though non-Fidelity clients are asked to register.]

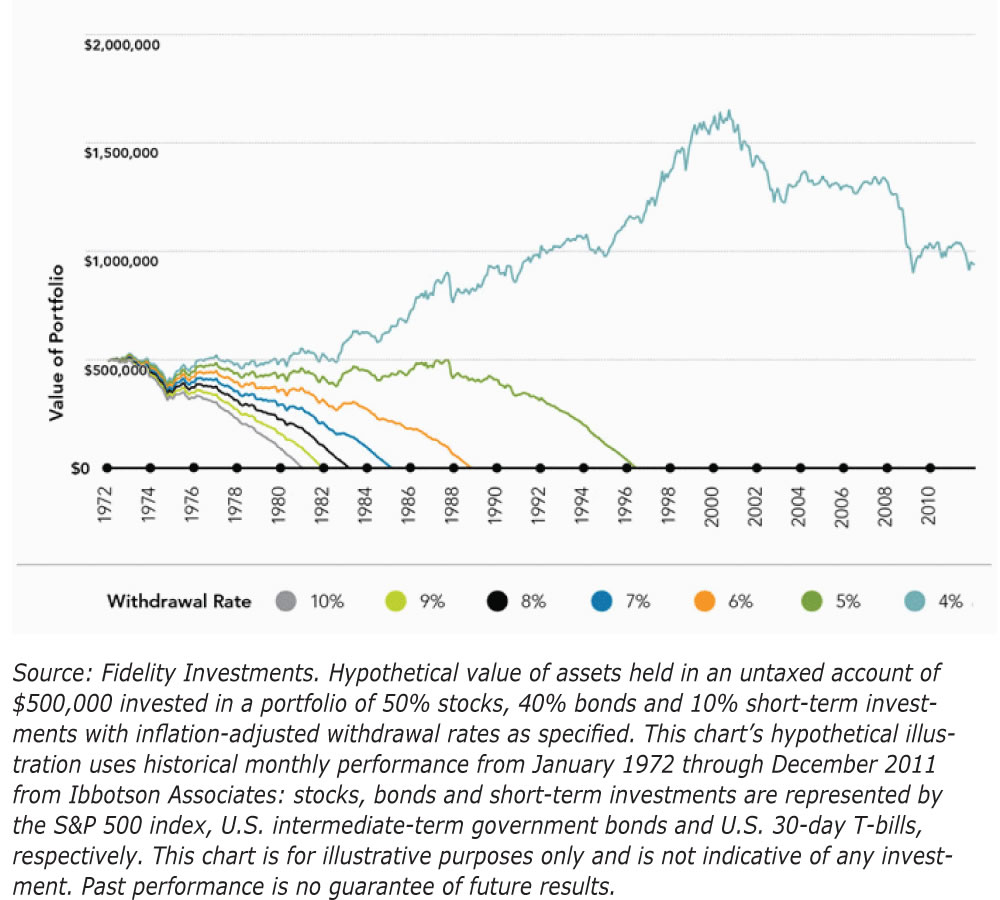

We looked at various withdrawal rates during a hypothetical extended down market. We used the Retirement Income Planner to see how a portfolio might have held up. We used a hypothetical balanced $500,000 portfolio of 50% stocks, 40% bonds and 10% short-term investments—an asset mix used by many retirees. Figure 1 illustrates how long this balanced portfolio might last with inflation-adjusted withdrawal rates between 4% and 10%.

As expected, the higher the withdrawal rate, the lower the number of years our hypothetical portfolio lasted. For instance, at a 10% withdrawal rate, the balanced portfolio only lasted 10 years. At a 4% withdrawal rate, however, the balanced portfolio lasted for 36 years—long enough to provide a 65-year-old with an income stream potentially lasting well into his or her 90s. That’s important because for a healthy 65-year-old couple, there is a 50% chance that at least one of them will survive to age 92½, according to the Society of Actuaries’ Annuity 2000 Mortality Table. (The figures assume a person is in good health.)

We also looked at withdrawal rates another way—how they affected the value of a hypothetical portfolio through up and down markets and periods with very high inflation. We used a hypothetical $500,000 balanced portfolio (50% stocks, 40% bonds, 10% short term) for a couple who retired in 1972 and tracked it through 2011, using actual historical index returns. This period includes the great bull market of the late 20th century—roughly 1982 to 2000. But it also encompasses two of the worst bear markets in Wall Street history, five recessions, two major wars, and the rabid inflation and painfully tight monetary policy of the late 1970s—one of the worst inflationary outbreaks in U.S. history.

As Figure 2 shows, the initial $500,000 would have been exhausted by the late 1980s if funds were drawn down at a 6% rate. (All rates are adjusted annually for inflation.) A 5% withdrawal rate could have extended income from the portfolio for nearly 25 years, but it still would have run out at a time when there would be more than a 50% chance that one member of the couple would need those assets. In this extreme case, only a 4% withdrawal rate would have left enough total assets intact to catch the full tailwind of the long bull market that ran from 1982 to 2000.

Our analysis clearly shows that the amount of the annual withdrawal rate dramatically raised or lowered the chances of a portfolio lasting for a longer period of time. And the risk of running out of money is a real one. Americans are living longer these days, so it’s entirely possible that your retirement could last for 30 years or more.

This chart also illustrates how the combined risks of inflation, market volatility and withdrawal rates run parallel with the risk of longevity itself, which is so easy to underestimate. Additionally, it further illustrates the power of potential stock returns—given enough time—and the critical importance of withdrawal rates. This isn’t to say that a 4% to 5% withdrawal rate offers magical security or assures infinite asset sustainability. Those outcomes depend on market performance. But it is clear that rates much above 5% begin—fairly quickly—to increase depletion risk of a retirement income plan.

Unlike the performance of your investments, your withdrawal rate is one of the variables that you can control and adjust as needed to take into account your age, health, availability of other assets and desire to leave money for your heirs (your asset allocation and actual retirement age are a couple of other key variables that you can influence). Staying within or below a 4% to 5% range (adjusted annually for inflation) will decrease the risk of depleting your retirement savings too soon. A more conservative withdrawal rate may also put you in a better position if a severe market downturn takes place. For this reason, we believe that most retirees should consider using conservative withdrawal rates—particularly if your assets need to support essential expenses. Retirees may feel comfortable taking a higher withdrawal percentage (with greater chances of depleting assets) when running out of money has no severe consequences.

Retirement Planning

Portfolio Strategies

Dominic Gioffre from DE posted over 13 years ago:

Michael Bork from WI posted over 13 years ago:

R Hixson from VA posted over 13 years ago:

Dave Gilmer from WA posted over 13 years ago:

Ed from NJ posted over 13 years ago:

Michael Poizner from CA posted over 13 years ago:

Bill Jones from NM posted over 13 years ago:

Nordron from CO posted over 13 years ago:

R Chichester from NC posted over 13 years ago:

Mike S from Florida posted over 13 years ago:

Ralph Strong from Maryland posted over 13 years ago:

Michael Henry from OR posted over 12 years ago:

Richard Abbott from FL posted over 12 years ago:

Bill Dooley from LA posted over 12 years ago:

William King from HI posted over 12 years ago:

Don Laurino from CA posted over 11 years ago:

Roy Johnson from NY posted over 11 years ago:

Richard Abbott from FL posted over 11 years ago:

Vaidy Bala from AB posted over 11 years ago:

Steve Daniels from CT posted over 11 years ago:

Steve Daniels from CT posted over 11 years ago:

Ira Gerson from IL posted over 11 years ago:

Gordon Spellman from AZ posted over 11 years ago:

ATS from MD posted over 11 years ago:

Mary Medvetz from CA posted over 10 years ago:

Susan Luthy from NV posted over 9 years ago:

James from IN posted over 9 years ago:

Jose from FL posted over 9 years ago:

Michael Murray from VA posted over 9 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account