Related

Financial Planning

Cognitive impairment afflicts approximately half of all 80-year-olds. However, there are steps investors can take to protect themselves financially.

David Laibson is a professor of economics at Harvard University, Cambridge. I spoke with him about how the risks of cognitive impairment and dementia impact investing decisions.

—Charles Rotblut, CFA

Charles Rotblut (CR): You have said that there are two key categories of cognitive function. Could you explain what they are?

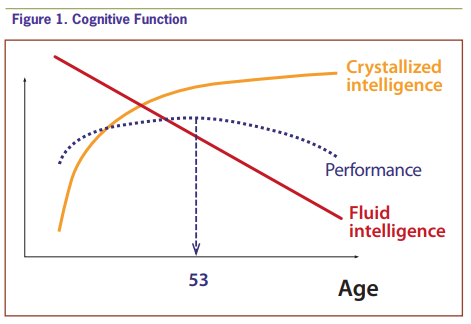

David Laibson (DL): The two categories of intelligence are fluid intelligence, which in essence is our ability to solve a novel problem, and crystallized intelligence, which is our ability, through life course experience, to accumulate knowledge and ultimately solve familiar problems. Fluid intelligence would be the kind of intelligence used to solve a typical IQ question: Take a two-dimensional object, fold it along the lines, and tell us what three-dimensional object it becomes. Crystallized intelligence would represent things like the experience that would enable someone to understand what an expense ratio is because they’ve been reading prospectuses for 30 years.

CR: And how do those change with age?

DL: The good news is that as we progress through the life course, we gain more and more experience and wisdom. And except for dementia, which comes late in the life course, basically it’s a story of improvement: As you get older, you have more experience, you have a greater knowledge of the world, and that makes you a better investor. Again, except for dementia.

The bad news is that fluid intelligence, which is our ability to confront a new problem and figure it out—say, to look at a new financial product and understand whether it’s good for us or bad for us, a product that we’ve never seen before or an investment that we’ve never thought about before or a company we’ve never analyzed before—that ability is declining, and it’s declining from age 20.

So we have these two countervailing trends. As we gain more experience, we become better investors. But our ability to solve novel problems is declining. And that makes us worse investors.

Now, you might say: Well, which trend dominates? Mostly, we’re getting better as we age, until about the 50s. And then, after the 50s, on average, we’re getting worse. After the 50s, the decline in fluid intelligence becomes the dominant force and our ability to make sophisticated decisions, for most people, declines. This does not mean that we fall off the cliff at age 55, but rather that we’re peaking around 50–55, and then we’re gently declining thereafter (Figure 1). The decline tends to become steeper as we age, and by the time we’re in our 80s, for many of us, the ability to make good decisions is significantly compromised, particularly decisions that involve complicated new problems.

CR: So it’s really our ability to analyze that we lose—we have the knowledge, we just can’t apply it correctly—is that what’s occurring?

DL: That’s one way of thinking about it. What I would say is this: We have knowledge, which enables us to do well on familiar problems. For example, if I gave an investor a prospectus and I said, “Find the expense ratio,” and she or he had been doing that for 40 years, they could still do that at age 80 (unless they had dementia). So solving a familiar problem—in this example, finding the expense ratio—they can do.

But suppose I gave an older investor a novel problem, like a new financial product he’s never seen before. Let’s say it’s a complicated variable annuity with some kind of guaranteed income rack. He has never seen that product before (in this example). So the ability to read the fine print, figure that out, understand this thing that they’ve never analyzed before is basically compromised, not for everyone, but for many older adults. That’s the issue that we need to be wary of: The novel problem, even for a healthy older adult, is going to be a challenge.

Now, I want to emphasize that for everyone, dementia is an issue, and dementia hits every aspect of intelligence. It hits our memories, it hits our experiential intelligence, our crystallized intelligence, our fluid intelligence. To the extent that we’re now talking not about just normal aging but about dementia in particular, that’s a problem for every aspect of our decision-making, and there’s no sense in which somehow we’re safe from the challenges of dementia when it comes to a familiar problem. Familiar problem or unfamiliar problem: Dementia is a devastating blow to our ability to make good choices.

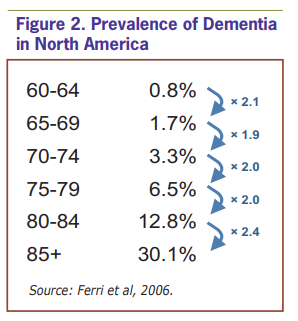

DL: Basically, the likelihood of dementia illness doubles every five years that we age. It starts out at tiny levels in the early 60s. But every five years that we age, the chance of having dementia doubles (Figure 2). By the time we get to our 80s, the likelihood of having dementia is about 20%.CR: What percentage of the population is experiencing dementia?

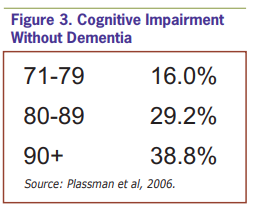

But it’s a little worse than that, because dementia is a severe case of cognitive impairment. There’s another diagnosis, which is called “cognitive impairment not dementia” (CIND), which describes a set of symptoms that are characterized by cognitive decline that is significant, but not so significant that we’re into the realm of dementia. And about 30% of the population in their 80s has the symptoms of CIND (Figure 3). Now, those individuals are also in a very poor position, really an inappropriate position, to make important financial decisions. If you add up the two groups, 20% of those in their 80s with dementia and 30% of those in their 80s with cognitive impairment not dementia, then we’re talking about, in total, half the 80-year-old population that is not in a position to make important financial decisions.

This is not the tail of the dog; this is a huge fraction of the population. We all should recognize that we have to be ready for this. It doesn’t matter if our parents died in a healthy cognitive state; it doesn’t matter how great we feel at 67; the reality is that the probability of cognitive impairment is so great that we need to begin to prepare for this possibility while we’re still healthy in our 60s, if not earlier.

CR: What should an investor do to protect financially against cognitive impairment?

Of the five documents, the first is the will. You want to write the will when you are still completely cognitively high-functioning. It’s not a good idea to wait until decline sets in; these are complicated, subtle issues.

DL: There are five legal documents that the young, healthy investor should execute. And then there is a set of other behaviors that I would recommend that go beyond just filing the right legal documents in preparation for cognitive impairment.

The next important document is a durable or springing power of attorney, which in essence appoints someone to manage your financial affairs in the event of your incapacitation. You know, I’m 45 years old, and it could happen to me tomorrow: I could have a stroke and need someone to make those decisions for me. So it’s not just an issue for people in their 80s, it’s an issue across the entire life span.

The third important document for households with significant assets is a living revocable trust. A living revocable trust in essence protects your assets by putting them into a legal entity that prevents you from disbursing them inappropriately if you’re experiencing decline. It basically puts a trustee in position to protect your assets in the event of your incapacitation.

Those are the three financial documents. There are also two health documents that I would strongly recommend; again, all this needs to be done before cognitive decline sets in, ideally no later than the 60s. Frankly, I would recommend this as soon as you form a family in your 30s or 40s.

One health document is a living will, which in essence is a set of instructions to your family members and physician suggesting how you want health care to be implemented. If you’re in an intensive care unit, do you want every effort to be made to sustain your life, even if the quality of life is abysmal, or do you want palliative care? What kind of health care do you want? How long do you want to stay in an intensive care unit, sustained by machines, etc? That’s a living will, and it can be extremely detailed or extremely vague, basically outlining your philosophy of health care at the end of life.

You also want to appoint a health care proxy. The health care proxy is someone who is basically empowered to make these important medical decisions for you in the event of your incapacitation.

Those are the five documents that I would set up at any age once you’ve formed a family, or at any age if you have significant assets. I mean, if you’re 25 years old and you have $20 million, it would not be a crazy idea to create these documents.

That’s the legal side of preparation. Then there’s, let’s call it, the psychological side of preparation. And I think what you have to do is come to terms with the reality of this kind of data and recognize that you just can’t count on cognitive functioning to be at a high level over your entire life. And you need to begin to plan for that possibility. And there are a few ways to plan for it that are really important.

First, you want to discuss with your family members what should happen in the event of your incapacitation. Of course, not everyone is comfortable doing that, so this is not a global recommendation, but it’s one that I would make strongly to most people, those with well-functioning family ties.

Then you need to think about how to organize your assets so that you don’t end up getting ripped off by con artists or just salespeople with inappropriate products to sell—they may not be illegal products, they may just be inappropriate late in life.

I would urge investors who dabble in securities that are not traded on public exchanges to think about stopping. For example, when I buy and sell a stock on the New York Stock Exchange or NASDAQ, I’m buying a stock that’s set at a market price. I don’t get a bad deal relative to everyone else. I get the same deal that Goldman Sachs gets, basically, when I buy and sell that stock. But when I buy an investment or make an investment that’s not traded on an exchange, well, I’m at the whim of the salesperson, and they might give me a terrible deal, and I wouldn’t know whether it was terrible or not, because there’s no public exchange on which that investment is traded.

For example, imagine your accountant comes to you and says, “Hey, there’s this guy who’s offering shares in a real estate development in the next town; he wants you to plop down $100,000 and you can be a part-owner of this new mall and condo that he’s developing.” Well, there’s no public price for that. And it’s just basically the developer’s word that this is a good investment. So I would suggest that older adults are in a very poor position to evaluate the merits of this type of investment. And I think that even in our 60s, we should curtail the habit of considering investments like that and instead focus our energies on investments that are less likely to go awry.

What are those less-likely-to-go-awry investments? Well, mutual funds. Diversified mutual funds with low fees. That is a much safer place to invest once one is in the position of not being cognitively very high-functioning, because in essence you’re delegating the decision to the mutual fund company. And with a mutual fund company, if the fee is low, there’s not a lot that can go wrong in that relationship, particularly if it’s a passive portfolio. But even if it’s an active portfolio. I would urge older investors to switch from the mentality of “anything goes” to the philosophy that staying in a more regulated, safer space of securities is the right philosophy. And doing that early rather than late is the way to go, because we’re often not in a good position to know whether we are in fact experiencing cognitive decline.

CR: You also like annuities, correct?

DL: Well, that’s complicated. I like them in principle. They have a lot of very appealing properties. For example, the most appealing property is the longevity insurance. It’s amazing how much longevity risk we face: We might die at 60, we might die at 105. An annuity basically passes that risk to the insurance company: If I live a long time, they keep paying out to me; if I die young, well, they get to keep the money. I don’t face the risk, they do, and now I can rest assured that no matter how long I live, there will be a monthly check coming. That’s terrific, great, and it’s the reason economists love annuities.

However, the American public does not love annuities. And whenever the public says “no” and economic theory says “yes,” my gut is to question the economic theory. Maybe we economists have missed something that the American public, deep in their hearts, knows, and maybe that’s why they don’t want annuities, and maybe it’s legitimate that they resist annuities.

I don’t want to tell people that annuities are an absolutely right choice. I do want to say to investors: Consider longevity risk. Consider the fact that you might live a very long time, and if you are spending your money at a normal rate, there’s a risk that you’ll run out if you live to 105. And consider the fact that an annuity is a way of insuring against that bad possibility. But at the end of the day you may decide you still don’t want an annuity—maybe you don’t like the loss of control of your assets, maybe all that fine print in the annuity contract gives you heartburn, maybe you just can’t sleep at night if you can’t lay your hands on your money the next day. Maybe the thought of dying at 70 and losing your money is so terrible that it overwhelms the thought of living to 105 and being a big winner from the annuity. I can’t speculate confidently about why the American public doesn’t want annuities, but I would urge people to think about annuities as an intriguing alternative before they glibly reject that path.

CR: What about getting people to actually do things like take charge of those documents? Any suggestions on how to get somebody, if they’re not working with an adviser who’s pushing them to take some of these steps, to stop procrastinating and actually do some of the things that are important?

DL: Well, the easiest way to get that done is to get an estate lawyer. What I would say is this: Don’t think of this as signing five complicated documents and getting an estate lawyer and talking to your family members and making all these decisions. That’s a lot to think about. Break it into pieces. The first piece is very simple: If you don’t have an estate lawyer, you’ve got to find one. It’s as simple as that. How do you find one? You talk to people who are sophisticated and whom you trust, and you ask them for recommendations. Very, very simple. And then you vet estate lawyers and you ask them about their fees and you ask your friends about their experiences with these attorneys. And hopefully, that process ends pretty quickly with an estate lawyer relationship. That’s one piece.

Once you have that attorney, things can move pretty quickly, because all you’ve got to do is tell the person, “Look, I have trouble, I’m a procrastinator like everyone else on the planet. Let’s set up an appointment to make sure that this process proceeds in a timely manner.” And once you have that appointment, well, there you go: You’re off to the races. It can be four months away; it doesn’t matter. The appointment will provide the discipline. And then you’ll go in, you’ll discuss everything with your attorney, they’ll draft documents, they’ll mail them to you. You should then set up another appointment—even before you’ve read the documents—that will be the signing appointment. You use appointments as deadlines to forestall procrastination.

CR: It seems like loss of control is the hardest thing—particularly for seniors, if they have deteriorating health or some other matters that are coming along. Any suggestions on how someone can deal with or accept the loss of control?

DL: The first thing I would emphasize is that a lot of these things may seem like a loss of control, but in fact, the real loss of control is very minimal. For example, with an annuity, yeah, it’s true that you can’t turn around tomorrow and buy a house in the Caribbean, because your money is locked into the annuity. But I’m not sure that you would want to turn around tomorrow and buy a house in the Caribbean; you need that money to pay your expenses. So yes: It’s true, you lose some optionality. But it’s not clear that you’re losing options that you would want to take anyway.

Moreover, even if you ended up passionately deciding that you must have that house in the Caribbean, your annuity payments can be used as mortgage payments. So you could take out a mortgage, buy that house in the Caribbean, and make your mortgage payments with your annuity. It’s not exactly clear that you’re even precluding anything. I would say that most of what you’re losing is psychological and not really options that should matter to you very much.

CR: Is there anything else that I didn’t ask that should be brought up regarding this topic?

DL: I think the one other thing that I would highlight is that we all—not all, but many of us—make two big mistakes that I want to urge people to avoid making. The first mistake is to think that, for some reason, dementia won’t happen to us. We’re special, we’re different, we’re going to somehow protect ourselves in a way that maybe is unclear in our minds, but will somehow be successful. I think we have to accept the reality that, whether the odds are 30% or 70%, there are significant odds, there is a significant chance, that substantial cognitive decline will affect our own lives, will affect our own cognitive function. That’s the first thing I want people to appreciate. It is a reality for all of us. Not a fate that we’re doomed to accept, but a probability that is substantial for all of us.

The second mistake that I think people make is that they falsely believe that somehow they’re going to magically notice significant cognitive decline setting in, and then at exactly the right moment do all these things, before the cognitive decline is too significant. They’ll somehow time it perfectly. At age 82, they’ll wake up one morning and say, “You know what? I’m losing a lot of cognitive function”; they’ll walk out that day, sign all these documents, and it will all be fine. That’s a grave mistake. We don’t have that ability to suddenly recognize it and do the right thing just before we lose the capacity to make these decisions well. I urge people not to think that cognitive decline only happens to other people, and also not to think that you’re going to be able to somehow time your response perfectly, responding to cognitive decline in real time in your 80s when you see it setting in.

Financial Planning

Retired Investor

Financial Planning

William from GA posted over 14 years ago:

Victor from CA posted over 14 years ago:

Barry from TX posted over 14 years ago:

L from MD posted over 14 years ago:

Donald from MO posted over 14 years ago:

Eric from VA posted over 14 years ago:

Fred from KS posted over 14 years ago:

Bryan from OH posted over 14 years ago:

Ray from MI posted over 14 years ago:

Donald from PA posted over 14 years ago:

James from TX posted over 14 years ago:

Bruce from MA posted over 14 years ago:

William from AZ posted over 14 years ago:

Jim C. from CA posted over 14 years ago:

Thomas from CA posted over 14 years ago:

Elaine from OR posted over 14 years ago:

Edward from UT posted over 14 years ago:

Jeff from NJ posted over 14 years ago:

GFD from IL posted over 14 years ago:

Robert from IL posted over 14 years ago:

Gerald from CA posted over 14 years ago:

Bruce from CA posted over 14 years ago:

Fred from CA posted over 14 years ago:

Mary Boylan from IL posted over 13 years ago:

R Kelly from AZ posted over 13 years ago:

Lorraine Coccaro from CA posted over 13 years ago:

Arthur Bernhardt from WI posted over 13 years ago:

Thomas Grzymala, CFP from VA posted over 13 years ago:

Jack Condrey from CA posted over 13 years ago:

Jay from CO posted over 13 years ago:

Rudolph Heider from MO posted over 13 years ago:

Charles Goetz from NY posted over 13 years ago:

Soleil Thornton from CA posted over 13 years ago:

Ray Robison from VA posted over 13 years ago:

Charles h Wadhams from CA posted over 13 years ago:

M Pirotte from CA posted over 13 years ago:

Peter Mc Dougall from TX posted over 10 years ago:

Geoffrey Stuart from PA posted over 10 years ago:

R Kelly from AZ posted over 10 years ago:

Jerry McCorkle from TX posted over 10 years ago:

T. Kelly from WA posted over 10 years ago:

Donald Griffith from CA posted over 9 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account