Over the last five years, investors witnessed the emergence of a new class of equity index products known as strategy indexes, or smart betas.

Smart betas have two distinct features: First, they advocate against traditional capitalization weighting; second, they are based on relatively transparent quantitative methodologies. Whether based on empirical research or actual live history, these smart beta products do seem to offer superior performances relative to traditional indexes, substantiating the claim that cap weighting might be a suboptimal index construct. The transparency mitigates the information asymmetry problems between investors and managers, which reduces ongoing due diligence costs.

In this article, we discuss the advantages of smart betas relative to active management and traditional indexes. We also examine three of the most popular smart beta products. Additionally, in light of the increased investor interest in low-risk strategies following the 2008 financial crisis, we specifically provide an allocation framework for investors who may have different preferences for high Sharpe ratio (higher risk-adjusted return) versus high information ratio (more consistent outperformance over a benchmark such as the S&P 500 index).

Why Smart Beta?

Having experienced the Japanese bubble in the late 1980s and the dot-com bubble in the early 2000s, many investors have become acutely aware that mispricing occurs frequently in the stock market. In the presence of mispricing, a traditional capitalization-weighted index overweights overpriced stocks and underweights underpriced stocks, which leads to a suboptimal portfolio outcome. Until recently, it was assumed that active management was the only way to take advantage of market mispricing and to outperform the “market” index.

However, active managers, on average, have not delivered on the promise of outperformance. Many academic studies have documented persistent active manager underperformance versus traditional index products. High fees, excess trading and, in some cases, outright lack of skill have plagued the active industry.

Smart betas are non-cap-weighted index strategies based on transparent quantitative methodologies. Deviating from cap weighting in a systematic way helps address the flaws of cap-weighted indexing. Having a transparent and mechanistic index methodology, which can be scrutinized, significantly reduces the information asymmetry issue, which lowers due diligence costs and the total cost for investment. Moreover, the moniker of “index” means that these products are usually offered at a significantly lower price relative to active funds, which again reduces the investment costs.

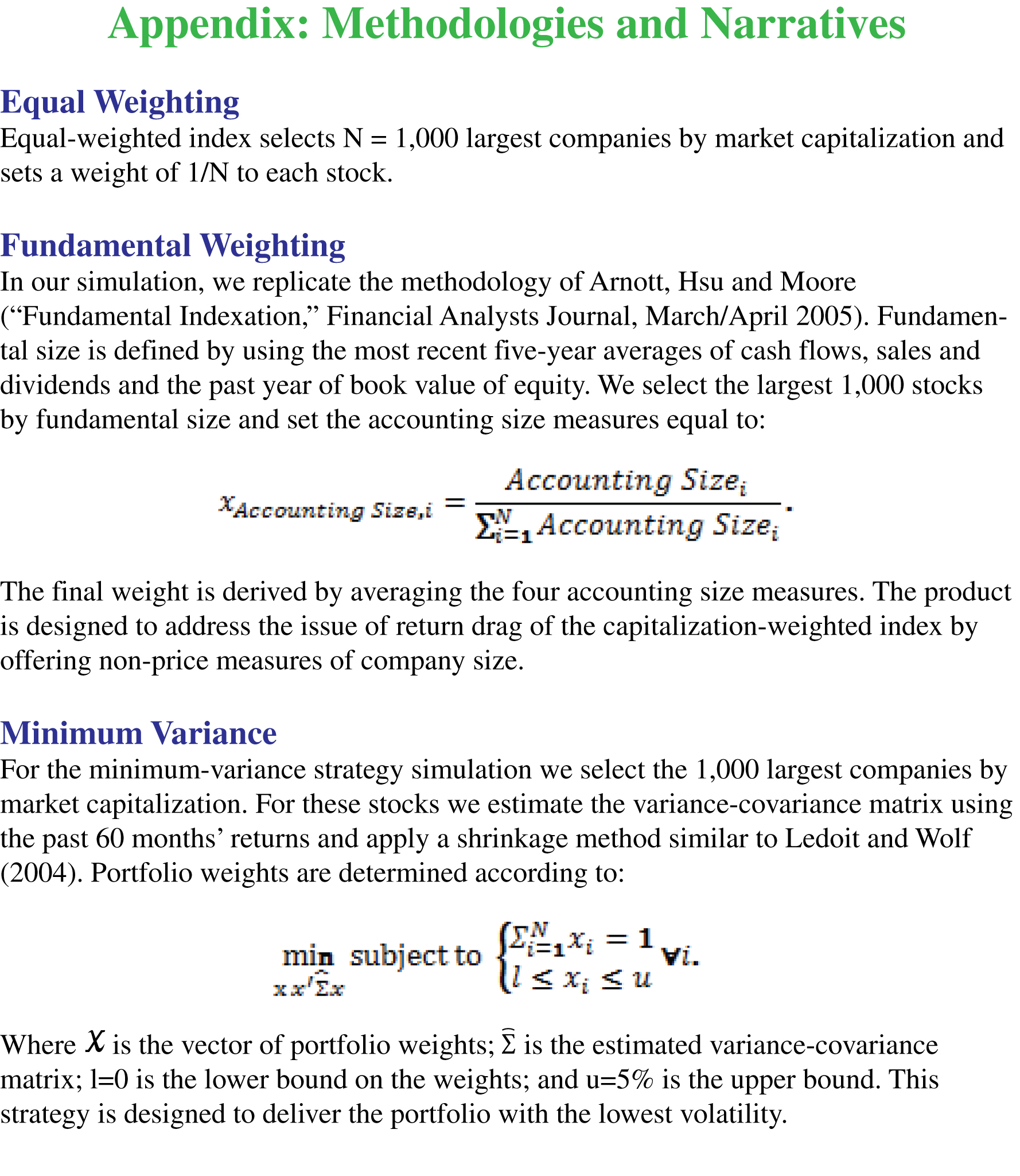

While the smart beta category is a new invention, some of the strategies now included in the category have had a longer history. Though the equal-weighted index goes at least as far back as 2003 with the introduction of the S&P 500 Equal Weighted Index, which is tracked by the Guggenheim exchange-traded fund S&P 500 Equal Weight ![]() (RSP), the concept of equal weighting certainly goes significantly further back in history. The minimum variance strategy has been known since Harry Markowitz’s 1952 paper on mean-variance optimization; the investment rationale for minimum-variance/low-beta strategies has been known since the 1970s. MSCI launched one of the first minimum-variance indexes in 2008 [the MSCI USA Minimum Volatility Index is tracked by the iShares MSCI USA Minimum Volatility Index Fund (USMV)], but other quantitative active managers, like Analytic Investors and Acadian Asset Management have offered active strategies based on low-volatility investing since the early 2000s. Research Affiliates’ Fundamental Index

(RSP), the concept of equal weighting certainly goes significantly further back in history. The minimum variance strategy has been known since Harry Markowitz’s 1952 paper on mean-variance optimization; the investment rationale for minimum-variance/low-beta strategies has been known since the 1970s. MSCI launched one of the first minimum-variance indexes in 2008 [the MSCI USA Minimum Volatility Index is tracked by the iShares MSCI USA Minimum Volatility Index Fund (USMV)], but other quantitative active managers, like Analytic Investors and Acadian Asset Management have offered active strategies based on low-volatility investing since the early 2000s. Research Affiliates’ Fundamental Index ![]() (RAFI) was launched in 2005, and is tracked by the PowerShares FTSE RAFI US 1000 Portfolio (PRF).

(RAFI) was launched in 2005, and is tracked by the PowerShares FTSE RAFI US 1000 Portfolio (PRF).

Empirical Results

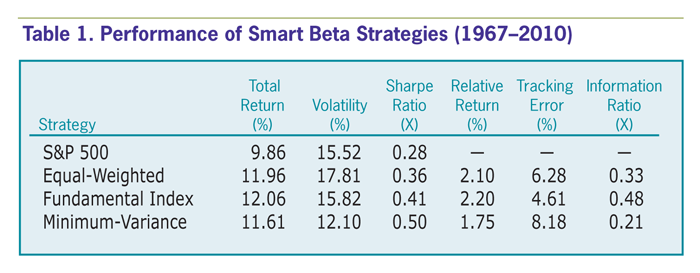

Smart beta strategies are generally based on transparent methodologies. This makes it possible for us to replicate them and examine their risk and return characteristics more deeply. To make strategies comparable, all strategies are rebalanced annually at the beginning of the year. For this study, the index portfolios were based on the 1,000 largest stocks to ensure that the resulting historical performance would not be dominated by illiquid and unusual stocks. For comparison, we compute total index return covering the period 1967–2010 for the U.S. In the appendix, available here, we provide a quick description of the methodology and investment philosophy behind each of the smart betas. Using identical data sources, rebalancing dates and rebalancing frequencies, we carefully compared the different smart betas in a controlled environment.

Performance characteristics

We replicated strategies using parameters that are as close to the commercially available products as possible. We report the standard performance characteristics of the smart beta strategies in Table 1. All summary statistics that we report are annualized using geometric compounding.

Note that all three strategies in our study outperform the cap-weighted benchmark. The subperiod analysis and parameter variations performed by other studies rule out, credibly, that the source of outperformance is due to data mining, short sample bias or other selection biases.

Interestingly, when we examine the level of outperformance for the risk-aware strategy, which attempts to manage the portfolio volatility where the others do not, we do not see any meaningful patterns or differences in its outperformance. When we examine the resulting portfolio volatility, we find that indeed strategies that have elements of risk control do generally succeed in reducing portfolio volatility relative to the cap-weighted benchmark. However, they also tend to ramp up the portfolio tracking error against the benchmark.

Given that the different smart betas are likely to have similar ex ante (expected) outperformance, the minimum-variance strategy, which uses risk control, would generally have a higher Sharpe ratio, owing to its lower portfolio volatility. The other two strategies, which do not incorporate risk control, would generally have higher information ratios, owing to their relatively lower tracking errors.

Four-factor attribution

To better understand the drivers of performance, we performed a four-factor return attribution. We found that the smart beta strategies examined have significant loadings on value and small-size factors, which are well-known sources of excess equity returns. Therefore, it follows that the different smart betas achieve outperformance by explicitly or implicitly accessing value and small-size premiums, which are premiums that hedge funds and quant strategies have relied on traditionally. Why might all of these smart betas exhibit value and small-size characteristics? After all, many, if not most, of the smart beta strategies do not explicitly seek to invest in value stocks or smaller stocks. From the theoretical work of Robert Arnott and Jason Hsu (“Noise, CAPM and the Size and Value Effects,” Journal of Investment Management, 2008) and the empirical work of Arnott, Hsu, Vitali Kalesnik and Phil Tindall (“The Surprising ‘Alpha’ from Malkiel’s Monkey and Upside-Down Strategies,” unpublished manuscript, 2012), we now know that non-cap-weighted portfolios would automatically exhibit value and small-stock tilts when there is mean-reversion tendency in stock prices.

Another natural question is whether the different smart betas can be meaningfully compared given that they do have different exposure to value and size characteristics. We assert that value and size premiums are, to the first order approximation, indeed one in the same in terms of their origins. Based on Jonathan Berk’s argument in the 1997 Financial Analysts Journal article, “Does Size Really Matter?,” it is unnecessary to finely distinguish between excess returns sourced from the value or size characteristics of the portfolio. Surprisingly, as it turns out, these outwardly different smart betas produce nearly similar premiums for similar reasons.

Comparing strategies with and without risk control, we notice an interesting pattern. The strategies with risk control generally have lower market beta loading. In fact, the strategy with the lowest volatility in Table 1, minimum variance, has the lowest market beta (market risk, not shown in Table 1) exposure. This means, regardless of how one chooses to manage risk, ultimately, the risk management will likely result in reducing exposure to the market beta. Unsurprisingly then, this strategy, which hedges off a significant amount of the market beta exposure, would also track the market index poorly, resulting in high tracking error. (Tracking error measures how much a strategy’s return differs from its benchmark’s return.) This results in the pattern of trade-off between the Sharpe ratio and information ratio.

A shrewd reader would immediately ask the question: If the low-risk strategy has a significantly lower market beta, would it not also earn lower returns? The empirical research in the 1970s, which rejects the positive relationship between market beta and expected returns, suggests that reducing exposure to market beta would not adversely affect the portfolio return. In fact, more recent studies seem to suggest that a lower beta exposure could indeed add new sources of equity premium not found in the standard value, size or momentum premiums.

Optimal Smart Beta Selection for Investor Portfolios

In the previous section, we argued that the smart beta strategies rely largely on the same return source—that is, they take advantage of the mean-reversion in stock returns through price-contra trading, which results in a blend of value and size portfolio tilts. In the long run, it is hard to argue that one strategy will perform better than the other. Given that the strategies are largely similar in their long-term return premium, the only differentiator is the degree to which the strategy controls for portfolio volatility risk in favor of tracking error risk. Given these risk objectives, investors should then evaluate strategies based on the cost of implementing a desired portfolio scheme.

Implementation characteristics

When seeing a backtest, it is always wise to ask whether the results are net of all implicit and explicit trading costs. The two biggest concerns for live portfolio implementation are capacity and trading costs. For a long-only strategy, the two simplest measures that help determine investment capacity and trading costs are the weighted average market capitalization and the annual turnover. Table 2 reports weighted average market capitalizations as of year-end 2010 and the average turnover for the period 1967–2010 for the domestic strategies.

The capitalization-weighted index obviously has the lowest turnover— any deviation from it creates excess turnover as the strategies need to rebalance against the intra-year price movements. Generally, smart betas constructed using heuristic approaches (equally weighted and fundamental index) have lower turnovers. Smart beta strategies that rely on optimization (minimum variance) tend to generate high turnovers.

Weighted average market capitalization tends to be higher for the strategies that use some notion of company size in the portfolio weighting. Fundamental index uses company fundamental size as the weighting anchor and therefore naturally inherits a large weighted average market capitalization, which provides portfolio liquidity and capacity.

Note that the actual commercially available index products would likely be evolved to improve their capacity and turnover characteristics, in an attempt to reduce implementation costs.

Portfolio allocation

From a portfolio allocation perspective, it is useful to categorize the different equity smart betas into those with no risk control, which therefore have market-like volatility and track the market portfolio, and those with risk control, which then have below-market volatility and high tracking error to the market portfolio. Equivalently, we can think of the smart betas as either favoring the Sharpe ratio or the information ratio. Obviously, if investors wish to express a tactical view on the market, the low-tracking-error (high information ratio) strategies would be suitable for bull markets and the low-volatility (high Sharpe ratio) strategies would be suitable for low-return markets.

The Sharpe ratio versus information ratio framework is indeed useful for thinking about these smart betas in long-term strategic portfolio allocation. As most of these smart betas would produce comparable outperformance, the pertinent question really becomes the investor’s definition of risk: portfolio volatility or tracking error to the cap-weighted benchmark. If an investor is more sensitive to underperforming the S&P 500 benchmark, then the high Sharpe ratio strategy (minimum variance) might be inappropriate, as it can result in prolonged periods of underperformance. For example, in the period covering 1990–2007, low-volatility strategies underperformed the market benchmark. This potential underperformance may be unacceptable even though the low-volatility strategy generally provides attractive returns and significantly reduced portfolio volatility.

Even though our historical data is computed from long-horizon data, there is still significant noise. Investors would be best served by not over-optimizing their portfolios based on historical results, but to instead diversify across a few appropriate smart betas that show low turnover and high liquidity characteristics.

Conclusion

In this article, we offer evidence that smart beta indexes deliver a robust value-add over traditional cap-weighted indexes. The value-add is driven by the value and size premiums, which are well known sources of equity returns that can be attributed to exploiting mean-reversion in stock prices through contrarian trading against price. We argue that the one commonality among all smart betas is their non-price-weighting scheme, which necessarily generates systematic rebalancing against price fluctuations. Under this framework, the various smart beta strategies are indeed largely similar. The largest differentiating factor among competing smart beta strategies is the degree to which they control for portfolio volatility in favor of tracking error. Strategies that favor lower tracking errors (e.g., fundamental index) have market-like volatility and more attractive information ratios. Strategies that favor lower volatility risk (e.g., minimum variance) generally have more attractive Sharpe ratios.

Given that the strategies are largely similar in the level of outperformance and are also similar in the source of outperformance, we argue that implementation costs and ease should be critical criteria for smart beta investors. Finally, investors who are considering adding smart betas to their current investment portfolio should carefully consider their risk preferences with respect to information ratio and Sharpe ratio. Optimal allocation results in trading off information ratio for Sharpe ratio, and vice versa.

The authors would like to acknowledge help, comments and suggestions from Noah Beck, Tzee-man Chow and Li-lan Kuo.

Discussion

FREE REPORT

Vernon Lewis from CA posted over 13 years ago:

John Portwood from LA posted over 13 years ago:

Paul Stadnik from OR posted over 13 years ago:

Jean Henrich from IL posted over 13 years ago:

D.E. from NY posted over 13 years ago:

JW from NC posted over 13 years ago:

Mike Philbrick from ON posted over 12 years ago:

John Blevens from CA posted over 12 years ago:

William Sanders from WA posted over 11 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account