While many academic studies highlight value measures that investors can use to construct market-beating portfolios, researchers have not been able identify quantitative growth factors that help investors build portfolios that outperform the market on a risk-adjusted basis. New research by Robert Novy-Marx, an assistant professor of finance at the Simon Graduate School of Business at the University of Rochester, looks to change that.

Novy-Marx reminds us that Benjamin Graham did not just focus on buying cheap stocks. Rather, Graham looked for undervalued companies—high-quality firms selling at attractive prices. Graham argued that it is best to build a portfolio of undervalued stocks that are being ignored or discriminated against by the market. Graham’s approach focused on the concept of an intrinsic value that is justified by a firm’s assets, earnings, dividends and financial strength.

Unfortunately, tests of many of the most popular measures of company growth and financial strength, such as past or expected earnings growth or return on equity, do not reveal strategies that could be used to select stocks poised to outperform the market as well as value measures such as low price-to-book-value ratios or low price-earnings ratios.

Most investors focus on the bottom line of the financial statement to measure company success and growth. Novy-Marx discovered that the firm’s gross profit is a much better predictor of future success and stock market performance than bottom-line earnings or even cash flow. Furthermore, since this test for quality growth is not highly correlated with value measures, investors can combine growth and value tests to build more diverse portfolios.

Gross Profit to Assets

Novy-Marx’s test for quality growth revolves around gross income (gross profit). Gross income, which is calculated by taking revenue (sales) and subtracting the cost of goods sold, represents the amount of profit a company earns by selling its products or services. Cost of goods sold is the cost a firm incurs by manufacturing or producing an item, such as material and direct labor costs. Gross profit reflects a firm’s basic pricing decisions and its material costs. The greater the gross profit and the more stable it is over time, the greater the company’s expected profitability. Trends are closely followed because they generally signal changes in market competition. If product costs are increasing, they will have to be either absorbed by the company, hurting profits, or passed on to the consumer, potentially hurting revenue.

Investors normally scale or compute a ratio from gross income so that it can be tracked over time and compared against other firms that are different in size. Typically, a gross margin figure is computed by dividing gross income by total revenue. The percentage reflects the proportion of gross profits earned from each dollar of revenue.

Novy-Marx scaled gross income to total assets rather than total revenue. Gross profit to assets is revenue minus cost of goods sold divided by total assets. By comparing gross profit to assets, investors are getting a snapshot as to whether or not the firm’s assets are profitable. Since the profitability test is measured so near the top line, it is considered a very clean measure of economic profitability. Novy-Marx feels that profitability measures get more “polluted” as one goes further down the income statement. He argues that a firm that has lower production costs (higher gross margins) and higher sales than its competitors is more profitable. However, it can have lower earnings than its competitors if it is expanding sales with an advertising campaign and establishing a larger sales force. These types of expenditures will not impact gross profits but may hurt operating profits as well as net income in the short term. Research and development outlays will also hurt bottom-line profitability until the research benefits result in higher sales or margins. Simple screens for earnings growth or earnings profitability have a difficult time distinguishing firms that have reduced earnings because they are investing for future growth from firms with lower overall product sales and profitability.

Testing Profitability Measures

Novy-Marx examined other profitability measures such as earnings before interest, taxes, depreciation and amortization (EBITDA). EBITDA considers cost of goods sold as well as selling expenses (marketing and advertising), general and administrative expenses (employee salaries, rent, insurance, electricity, etc.) and research and development expenses. While he found that profitability measures such as EBITDA-based ratios were useful and had predictive powers, gross profit to assets took their contribution into account and did a better job overall of predicting future performance.

Gross profit to assets also outperformed the use of free cash flow to equity as a means of building profitable portfolios. Free cash flow represents cash that management is able to use at its discretion. Free cash flow is cash flow from operating activities less capital expenditures and dividends paid. Free cash flow is reduced when a company is investing resources on items such as research and development, additional product inventory or even expanding its factories. While these investments may hurt current bottom-line profitability and free cash flow, they should help sales and profitability down the line. Free cash flow to equity penalizes firms for investing in their future, while gross profit to assets does not. Free cash flow did a better job than earnings in predicting future stock price performance, but gross profit trumped all the growth measures Novy-Marx tested.

Novy-Marx presents his results in two related research papers—“The Quality Dimension of Value Investing” and “The Other Side of Value: The Gross Profitability Premium.” Novy-Marx’s findings highlighted that the gross-profit-to-assets ratio worked well in predicting future performance of companies. “The Quality Dimension of Value Investing” paper describes the results of growth, value and momentum tests using a universe of the 500 largest non-financial firms traded on the New York, American and NASDAQ stock exchanges. Financial firms were excluded from the tests because the assets of these firms are primarily financial securities, not operating assets. This makes it difficult to compare gross profits to assets across financial and non-financial companies.

The tests created portfolios by sorting the large-cap universe to create 150-stock portfolios with the highest- and lowest-ranked stocks for a given tested parameter (top and bottom 30%). The portfolios were held for one year and rebalanced each year at the end of June. Novy-Marx built the portfolios mid-year to be certain that the annual income statement and balance sheet from the prior year-end were available for the analysis. The tests covered the period July 1963 to December 2011. Quarterly financial data was not available for testing until 1972, which is why the test was constructed in this fashion using annual data. Fortunately, the use of quarterly data to construct gross profit portfolios proved to be even more profitable.

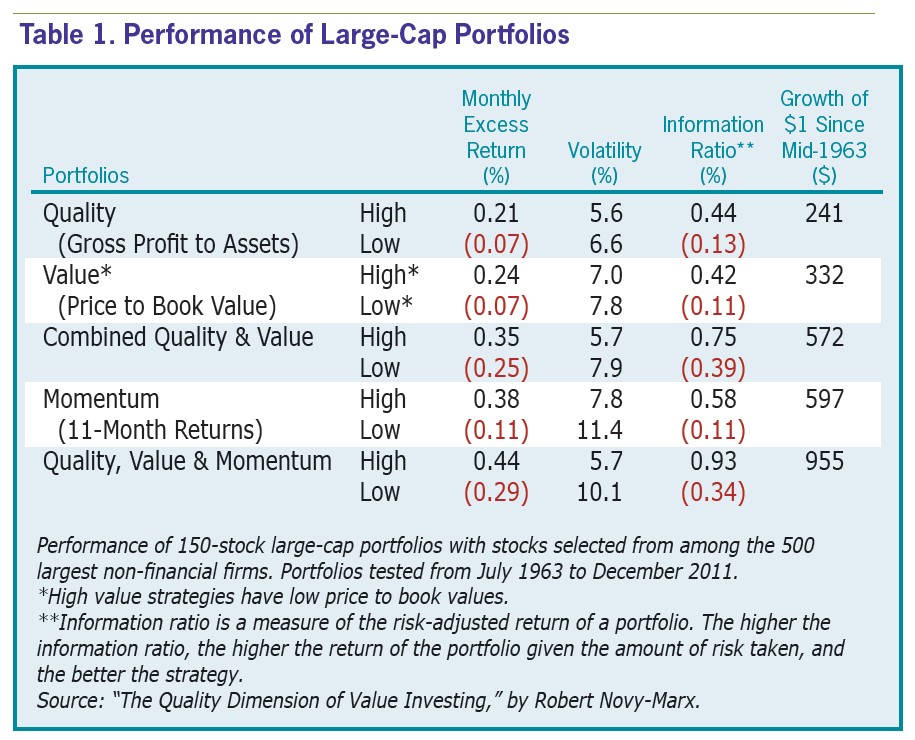

Table 1 summarizes the performance of the strategies. Gross profit to assets turns out to be a powerful predictor of future growth in gross profitability, earnings, free cash flow and payouts (dividends plus share buybacks). The portfolio formed from high gross profit stocks also tended to have relatively high price-to-book-value ratios. Novy-Marx calls them “good growth” stocks because they were able to outperform the market even though they had high price-to-book-value ratios. The turnover was low for this strategy, taking around four years to turn over. The portfolio of stocks with the highest gross-profit-to-asset ratios had an excess return of 0.21% per month, while the portfolio of stocks with the lowest gross-profit-to-asset ratios underperformed the market by 0.07% per month. The volatility of the portfolio with low gross-profit-to-asset stocks was also higher, hurting its risk-adjusted return even more.

Quality Growth

Novy-Marx called stocks with high gross profits to assets “quality” growth stocks. Even though these stocks trade with high price-to-book-value ratios, they have strong future performance. Portfolios of quality growth stocks hold very different stocks than portfolios using pure value strategies, so they offer the potential for a value investor to diversify their holdings yet maintain the potential for a high return on a total and risk-adjusted basis.

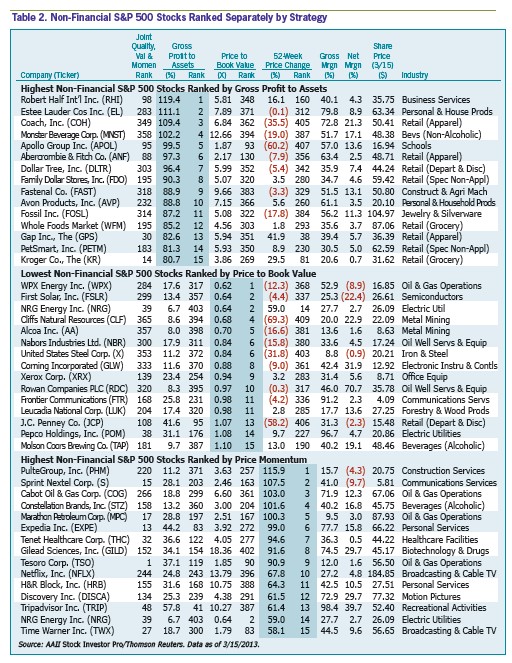

We used Stock Investor Pro, AAII’s stock screening and analysis program, to build a number of portfolios that represent the types of stocks described by Novy-Marx. We focused on large-cap stocks and first specified that a stock be a member of the S&P 500 index. We then excluded financial firms as well as foreign stocks marked as ADRs (American depositary receipts—that is, foreign stocks traded on American exchanges). We also screened out firms with negative equity (book value). We were left with a universe of 409 non-financial large-cap stocks. We created a custom field for gross profit to assets that divided gross profit over the trailing 12 months by total assets at the end of the last fiscal quarter. We wanted to create scores that combined the ranks of multiple strategies, so we exported the data of our large-cap universe into Excel and used the program’s Rank function and sorting features to create tables of passing companies. The top panel of Table 2 lists the 15 stocks with the highest gross profits to assets. We thought it might be interesting to also display the top-line profit margin (gross margin, or gross profits dividend by revenue) and bottom-line net margin (net margin, or net income divided by revenue). We were surprised to see so many retail stocks at the top of the quality growth list. The high asset turnover of these stocks must have helped to propel them to the top of the list. Most of these stocks had high price-to-book-value ratios and low 52-week price performance.

High Value

Prominent academic studies point to the price-to-book-value ratio as the best value predictor of stock price performance. Novy-Marx created 150-stock portfolios consisting of the high value (low price to book value) and low value (high price to book value) groups in the universe of 500 non-financial large-cap stocks. The portfolio with low price-to-book-value stocks (high value) had a monthly excess return of 0.24%. This was higher than the 0.21% return for the high-quality portfolio, but the volatility was also higher, resulting in a lower risk-adjusted performance figure of 0.42%. The portfolio with low price-to-book-value ratios easily outperformed the high price-to-book-value (low value) portfolio, which had a monthly excess return of –0.07%.

We followed Novy-Marx’s example, and the middle panel of Table 2 highlights the 15 non-financial S&P 500 stocks with the lowest price to book values. These stocks are much different than the quality growth stocks in the top panel of the table. This group has a high concentration of industrial and natural resource stocks. These stocks tend to have low gross profits to assets and their 52-week price performance is generally weak.

Novy-Marx notes that industries such as software developers and pharmaceuticals that do not employ much tangible capital in the production process tend to have high price-to-book ratios as well as high gross profitability because they do not carry high tangible book value on their balance sheet. The opposite tends to be true with stocks with low price-to-book ratios and the rankings in Table 2 bear that out.

Combining Quality and Value

It is possible to combine the gross profitability strategy with the low-price-to-book-value strategy and keep the return high and reduce portfolio risk. Novy-Marx measured the drawdown of the large-cap strategies. Drawdown is the peak-to-trough decline during a market downturn. These drawdowns are usually quoted as the percentage between the peak and the trough.

The drawdowns during bear markets for the joint strategy were better than the drawdowns for the individual strategies. The joint quality growth and value strategy worked in a wide range of market environments. Value stocks underperformed the market by 44% during the tech-stock run of the second half of the 1990s, while quality growth stocks lagged the market through much of the 1970s, underperforming the market by 28.1% by the end of the decade. However, Novy-Marx indicates that the joint quality growth and value strategy never lagged the market by more than 15.8%. The cheap, profitable stocks strategy usually bounced back quickly and strongly when it fell behind the market, creating short drawdown periods that sharply reversed.

The easiest way to combine the gross profitability strategy with the low-price-to-book-value approach is to create a single variable that combines both measures. Novy-Marx indicates that investors could first establish a set of firms to consider for investment. The stocks can then be ranked by growth—best (highest gross profit to assets) to worst (lowest gross profit to assets)—and separately by value—best (lowest price-to-book-value ratio) to worst (highest price-to-book-value ratio). The joint measure combining quality and value is simply the sum of the ranks of the two individual measures. If a stock has the 23rd highest gross-profit-to-asset rank and the 41st lowest price-to-book-value rank, its combined score is 64.

This process is similar to the technique used by Joel Greenblatt in his book “The Little Book That Still Beats the Market” (John Wiley & Sons, 2010) to calculate his magic formula. Greenblatt’s Magic Formula was covered in a First Cut article in the December 2011 AAII Journal (www.aaii.com/journal/article/greenblatts-magic-formula).

The performance of the combined quality and value portfolio was 0.35% and the volatility was low at 5.7%. The combined quality and value group’s higher excess return and low volatility boosted the risk-adjusted performance to 0.75%. In contrast, the 150-stock portfolio that had the lowest gross profit to assets and highest price to book had negative excess monthly return of 0.25% and higher volatility of 7.9%, resulting in a risk-adjusted performance of -0.39%.

Price Momentum

Novy-Marx does not stop by combining growth with value. He notes that price momentum is another “robust capital market anomaly” that has been shown to work profitably when used by itself as well as when it is combined with value strategies.

Price momentum strategies seek out stocks with strong recent price performance with the hope that the price momentum will continue into the future. Price momentum is normally measured by comparing the stock price change against that of a market index or a segment of stocks. Price momentum has connections to company performance and human behavior. Price momentum can highlight stocks that are reacting to strong or improving company performance and future prospects. Investors look for stock price performance better than that of other stocks with the belief that the rising price will attract other investors, who will drive up the price even more.

To construct high price momentum portfolios, Novy-Marx ranked stocks by their performance in the first 11 months of the year preceding the annual portfolio formation. As shown in Table 1, stocks with high price momentum had high excess returns of 0.38%. This was higher than the combined quality growth and value excess return of 0.35%, but the volatility of the high-momentum portfolio was greater, resulting in a lower risk-adjusted information ratio of 0.58%. In contrast, low price momentum had a negative excess return of 0.11% with even greater volatility.

We ranked the non-financial S&P 500 stocks by their 52-week price change and present these stocks in the bottom panel of Table 2. Homebuilder PulteGroup (PHMl) eads the list as the housing market is rebounding. Other winners include oil refiners, Internet travel sites and entertainment stocks.

Combining Quality, Value and Momentum

Using the same method for calculating the joint quality growth and value score, Novy-Marx constructed portfolios that also take price momentum into account. He ranked his stock universe by the price performance for the first 11 months of the year preceding portfolio formation of the test portfolios. The price performance ranking was combined with the gross-profit-to-assets ranking and the price-to-book-value ranking to form a single composite rank or score. The study paper indicates that all three rankings were given equal weighting for the sake of simplicity, although you might be able to improve performance by changing the weights.

The average monthly excess return for these stocks came out to 0.44% and volatility stayed low at 5.7%, resulting in a very high risk-adjusted information ratio of 0.93%—higher than that observed for any other strategy. A dollar invested in July of 1963 in the strategy that combines quality, value and momentum would have grown to $955 dollars by the end of 2011. Over the same time frame, $1 invested in T-bills would have grown to $12.31, while $1 invested in the market would have grown to $84.77. All of the individual strategies were able to improve upon market performance, but since they all offer different dimensions to selecting stocks, Novy-Marx shows how investors can benefit from combining these distinct strategies.

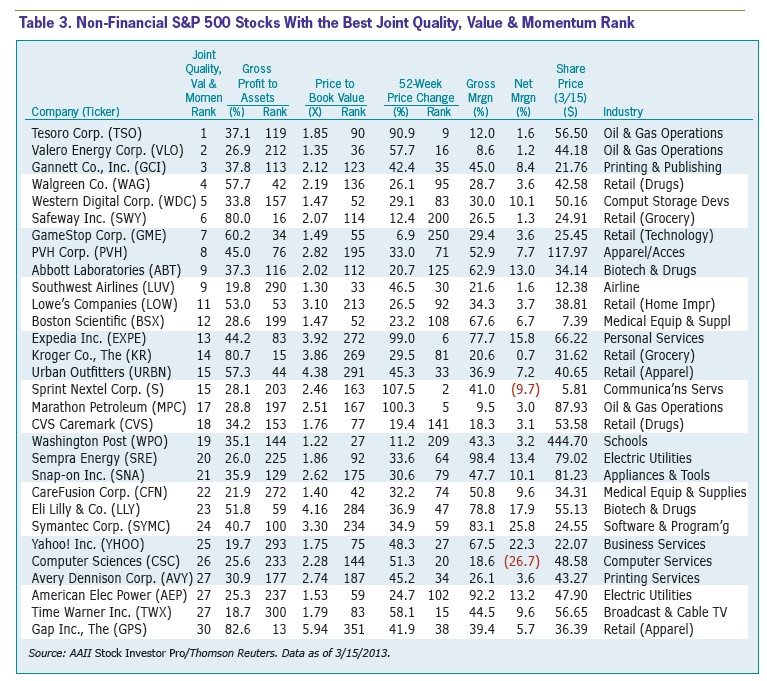

Table 3 displays the 30 non-financial S&P 500 stocks with the best combined quality, value and momentum ranking. It is an interesting and diverse group of companies that look worthy of further analysis.

Conclusion

Novy-Marx offers new dimension to building stock portfolios.

Value measures such as price to book value attempt to identify undervalued stocks, but investors need to use secondary screens to avoid stocks that are cheap for a good reason. Novy-Marks shows how value investors can use gross profit to assets as a quality signal to separate true bargains from value traps. He uses one of Warren Buffett’s favorite sayings to illustrate this value-growth trade-off, “It is far better to buy a wonderful business at a fair price than to buy a fair business at a wonderful price.”

Growth investors can benefit from using value screens to avoid good companies that are already fully priced. Patience is often required while waiting for the market to recognize the value of a given stock. Combining value with quality growth and price momentum should help to identify attractively priced growth stocks on the move.

Keep in mind that the purpose of these screens is to illustrate with real firms a useful combination of value, growth and momentum analysis. The screens are a mere first step in the stock selection process.

See AAII’s VMQ Stocks for a portfolio dedicated to value, momentum and quality and a list of stock ideas based on the VMQ criteria.

Discussion

FREE REPORT

Kurt Roggendorf from CT posted over 13 years ago:

Charles Rotblut from IL posted over 13 years ago:

Vernon Roberts from FL posted over 13 years ago:

Jim Gravitt from KY posted over 13 years ago:

R Frey from TX posted over 13 years ago:

Charles Rotblut from IL posted over 13 years ago:

Werner Emmerich from PA posted over 13 years ago:

John Wiley from AZ posted over 12 years ago:

A Singer from California posted over 12 years ago:

VAIDY B from CAN posted over 5 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account