One of Warren Buffett’s famous quotes that many investors and portfolio managers follow and recite to their followers, “never invest in a business you can’t understand,” can be applied to investing in exchange-traded products (ETPs).

The nomenclature ETP is rarely used in the popular press or by investors; even Ned Davis Research has an ETF Service. All ETPs are not created equal. There are exchange-traded funds (ETFs), exchange-traded notes (ETNs) and unit investment trusts (UITs). Many will add open- and closed-end mutual funds to the ETP basket as well. To confuse matters more, many of these vehicles have different structures: grantor trusts, limited partnerships and open-ended 1940 Investment Company Act funds. These are all important considerations when determining the tax implications, tracking error, asset allocation and distribution differences in owning a fund.

To delve into the differences of structures would take much more space than allotted for this article, but I will cover the three main investment companies. Nearly every ETP provider has literature on their website explaining the differences and similarities among products. In addition, there has been a plethora of books, articles and academic literature published on the subject. For the purpose of this article I want to focus on ETFs and ETNs, explaining the basic mechanics of how they trade, and why it is important to know what you own.

Mutual Funds, Closed-End Funds and Exchange-Traded Funds

The Investment Company Institute (ICI) tracks flows into and out of three investment companies: mutual funds, closed-end funds and exchange-traded funds. In total, there is over $13 trillion in the U.S. held in these vehicles.

At nearly $12 trillion in total assets, mutual funds hold the lion’s share of investment company assets. Mutual funds can be either actively managed or they can track a passive index. In 1924, the Massachusetts Investors Trust was launched as the first actively managed open-end mutual fund. The first passive mutual fund was launched in 1976 by Vanguard to track the S&P 500 index. Both the passive and the active funds are considered open-end because they can buy back existing shares or issue new shares of the fund on a daily basis, typically at the fund’s daily closing net asset value (NAV).

Closed-end funds (CEFs) have a relatively small piece of the investment company pie, with only $300 billion in total assets. As the name suggests, they issue a fixed number of shares during their initial offering process, which typically remains constant throughout the life of the fund. Unlike open-end mutual funds, closed-end funds trade on the exchanges during the day based on their bid and offer prices. Because of the closed structure, CEFs will often trade at a premium, or discount, to net asset value.

ETFs are one of the fastest-growing investment vehicles, with total assets reaching $1.4 trillion in 2012 (Figure 1). Like open-end mutual funds, exchange-traded funds typically hold a basket of underlying securities. The basket can consist of stocks, bonds, futures, options, forwards (a non-publicly traded contract to deliver a cash commodity at a specified date in the future), the rights to physical commodities, or any combination thereof.

ETNs are senior, unsecured, unsubordinated debt securities issued by an underwriting bank, and their assets are typically lumped together with ETF assets. Similar to other debt securities, ETNs have a maturity date and are backed only by the credit of the issuer. ETNs typically do not guarantee any return of principal at maturity and do not pay interest during their term. Instead, you receive a cash payment at maturity less fees based on the performance of the underlying index. Since both ETFs and ETNs typically track an index, the main difference is that exchange-traded funds hold some percentage (full or partial replication) of the underlying securities in the index, whereas exchange-traded notes do not; their objective is merely to meet the total return at maturity of the underlying index, less any fees or expenses.

The Important Role of the Creation and Redemption Process

The primary market for ETFs is where the new shares are created for an ETF/ETN through the in-kind redemption and creation processes. This is typically done in blocks of 50,000 shares (a “creation unit”). At the most basic level, an authorized participant will deliver the underlying stock constituents (for an equity ETF), and any needed cash (ETNs are cash transactions only), to the fund sponsor for a new creation unit. In exchange, the sponsor delivers shares of the fund. For redemption, the process is reversed: the authorized participant delivers shares of the ETF to a sponsor, and the basket of securities is removed from the ETF holdings and delivered to the authorized participant. This process occurs away from the secondary market and, for tax purposes, is not considered a taxable event. This is one of the main reasons why ETFs are more tax-efficient than many mutual funds. Each day, ETF sponsors provide both creation and redemption basket constituents to data vendors, so all parties know the size and weights of all deliverables. The baskets will trade close to intraday net asset value throughout the day.

Investors, typically larger firms, will use this process to execute their ETF trades. Because new shares of a fund can be either created or redeemed in very short order, the actual liquidity of the fund is really based on the least liquid security in the basket delivered or received by the sponsor. Many investors will see a large bid/ask spread, or light trading volume in a fund, and assume that the fund does not have any liquidity. There are several liquidity-providing firms out there that will work with the authorized participant to get better prices than individual investors see on the secondary market quote screens.

Because of this unique in-kind redemption process, it is possible to have more short interest [number of shares sold short and not yet repurchased] than shares outstanding in a fund. Just like U.S. equities, shares of an ETF/ETN can be shorted, and in some cases the number of shares short can exceed the actual number of shares outstanding in an ETF. I think the key here is that before a short position is established, an investor must post cash collateral for the trade. For example, an ETF has 1,000 shares outstanding held by Investor A. Investor B is interested in shorting 1,000 shares, so he posts cash collateral to Investor A, borrows the 1,000 shares and sells them to Investor C, who is now long 1,000 shares. Investor D also wants to short 1,000 shares and posts cash, gets Investors C’s shares and sells them to Investor E, (short position for Investor D and a long position for Investor E). In this scenario, there are effectively 1,000 shares outstanding and 2,000 shares of open short interest, which equals 3,000 shares of long interest (1,000 actual shares and 2,000 in cash collateral).

Typically, ETFs with a very high ratio of short interest to shares outstanding have very liquid underlying baskets. Because of the creation/redemption process, you can’t really get a short squeeze in ETFs like you can stocks; stocks don’t have a continuous issuance process (shares outstanding are fixed). Instead of a short squeeze (when an ETF rises against the shorts), the borrow rates for holding a short position on an ETF basket will become more expensive and is typically an impetus for short covering.

Tracking Error and Realized Performance

One major component of knowing what you own is understanding the vehicle or index that the fund is tracking. Because ETNs are notes, the return of the note should be equal to that of the index less fees, so there should be minimal tracking error [the average amount by which the ETN return deviates from the return of its target index]. For ETFs, there can be considerable tracking error between the fund’s performance and the underlying index.

There is no one standard definition or calculation for tracking error. The most-followed method is the difference in the NAV return of the fund versus the underlying index total return. Because there isn’t an industry standard for this measure, estimates of tracking error for a specific fund can differ significantly, depending on the time frame and calculation. Typically, the longer the time frame, the better the tracking error looks. Fund companies will usually provide the full tracking error history.

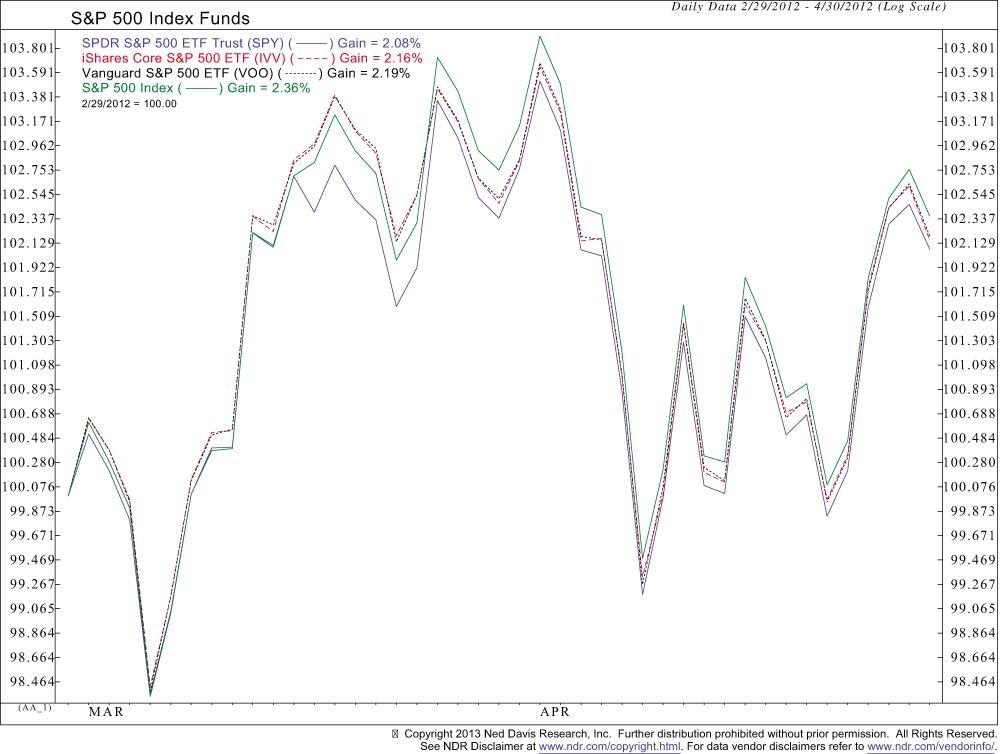

Tracking error should really be based on the individual’s holding period: Did the fund return what I expected based on the performance of the underlying index? I typically suggest that investors should be more worried about what the fund owns and how that fits into your portfolio, rather than the tracking error. Figure 2 shows tracking error over a three-month period based on the closing values of one of the most widely followed indexes in the world, the Standard and Poor’s 500 index (S&P 500), and the closing prices of three funds that aim to track the index.

As shown in Figure 2, there is a 28-basis-point return difference between SPDR S&P 500 ETF ![]() (SPY), which is organized as a unit investment trust, and the index [2.08% versus 2.36%]. If you look at the NAV returns for these three funds, they are identical over this time frame. However, if you compare the total return (add distributions back in) of the three funds and the index, the returns differ.

(SPY), which is organized as a unit investment trust, and the index [2.08% versus 2.36%]. If you look at the NAV returns for these three funds, they are identical over this time frame. However, if you compare the total return (add distributions back in) of the three funds and the index, the returns differ.

A recent study on ETF tracking error done by Morgan Stanley Smith Barney found that the Guggenheim S&P Equal Weight Utilities ETF (RYU) had the second-largest tracking error of all funds traded in the U.S. For 2012, RYU had a tracking error, minus fees, of 449 basis points versus the index. How could this be? The fund should easily be able to track a basket of domestic utility stocks and equally weight them. The analysis done for the study exploits another issue with the standardization of ETF information. Like tracking error, there is no industry standard for style (growth or value), capitalization (small, mid, large) or sector and industry exposure. This utility fund also holds telecommunications stocks from the S&P 500. With a 13% weight in this fund, as is shown in Table 1, the action of telecommunication stocks is where the tracking error lies for RYU.

|

Allocation

|

|

|

Weight**

|

|

|

Sub-Industry*

|

(%)

|

| Multi-Utilities |

37.15

|

| Electric Utilities |

34.34

|

| Integrated Telecommunication Services |

13.00

|

| Independent Power Producers & Energy Traders |

5.20

|

| Gas Utilities |

5.16

|

| Wireless Telecommunication Services |

5.15

|

| *Uses Standard and Poor’s GICS Equity Classification System. | |

| **Based on long position creation unit weights. | |

Comparing funds on a standardized basis is crucial for complete evaluation of how a fund will contribute in a portfolio. If you own RYU and another telecommunications fund, you may have too high of an exposure to telecommunications that you hadn’t accounted for. Investors cannot simply take the name for granted when making investable decisions. There are many cases of ETFs that call themselves growth funds, or small-cap funds that have a great deal of exposure to value or mid-cap stocks.

Additionally, many funds do not fully replicate the underlying index they are tracking. This is especially true for international funds, and this is why, on average, international equity and fixed-income funds will have some of the highest tracking errors. Many international funds will state in their prospectus that they follow a replication strategy and may only completely replicate 80% of the index’s underlying holdings. The other 20% could be allocated to other highly correlated assets, or even derivatives of the underlying index. This occurs because of the illiquidity of the underlying assets in the index. It is one thing for an asset to be included in an index; it is another to actually purchase that asset in enough quantity, at good prices, so that it can be included in the ETF basket.

Many fund providers have started to remedy this issue by selecting so-called investable, capped, pure float or liquid indexes to benchmark their ETF. Historically, the index was created first and an ETF would follow. That is no longer the case in many new offerings; the ETF idea is created first, and then an index is created to match that idea. This approach will significantly reduce tracking error and any issues with full replication.

Consider Fees and Other Factors

Investors should also have an understanding of the fund’s fees, distribution schedule, taxation and rebalancing periods.

Fees are often referred to as the expense ratio, which is the total annual cost of owning the fund. Expense ratios differ by fund and can be found in a fund’s prospectus. Fees for ETFs may or may not include all of the following: management fee, distribution and service (12b-1) fee, acquired fund fees and expenses, and possibly a “fee waiver.” The fee waiver is something investors should pay particular attention to. This figure will show up as a subtracted percent from a fund’s total operating expenses and fees (expense ratio). Many fund companies will waive part of the fees for a fund for a set period following the launch of the fund to attract assets. In some cases, the waived amount can be substantial, and if you aren’t aware of the increase, you could get caught in a fund that is underperforming just because of a fee increase. Per share fees are taken out of an ETF each day.

Many ETFs are very efficient and have zero capital gains or dividend distributions, and in many cases a dividend distribution from the underlying stock components is put back into the fund. How a fund handles distributions can be a contributing factor in tracking error. Some funds are structured as a unit investment trust, like the SPDR S&P 500 ETF ![]() (SPY). They accumulate dividend distributions and pay them out approximately six to eight weeks after receiving the payouts. This means that an investor, if reinvesting dividends, could have missed opportunity costs. Fund providers will often outline their distribution schedule in the fund’s prospectus. Fund providers will also announce year-end distributions well in advance so investors can plan ahead.

(SPY). They accumulate dividend distributions and pay them out approximately six to eight weeks after receiving the payouts. This means that an investor, if reinvesting dividends, could have missed opportunity costs. Fund providers will often outline their distribution schedule in the fund’s prospectus. Fund providers will also announce year-end distributions well in advance so investors can plan ahead.

I am not a tax professional, so please consult an appropriate professional for more information on the tax treatment of different ETF structures. In general, stock and bond ETFs and ETNs are taxed at short- and long-term capital gain rates like stocks. However, currency funds are not considered investable vehicles and are taxed as ordinary income. Many of the commodity- and futures-based funds are taxed similarly to futures, as 60% short-term gains and 40% long-term gains. The real standout on taxation for me is physical precious metal funds, like the SPDR Gold Shares ETF ![]() (GLD). These funds are taxed the same as collectibles, which is typically at a much higher rate than capital gains. Additionally, a fund like GLD will have multiple taxable events throughout the year. Some funds, like master limited partnerships, are better structured as ETNs rather than ETFs, from a tax perspective.

(GLD). These funds are taxed the same as collectibles, which is typically at a much higher rate than capital gains. Additionally, a fund like GLD will have multiple taxable events throughout the year. Some funds, like master limited partnerships, are better structured as ETNs rather than ETFs, from a tax perspective.

Rebalancing is the buying and selling of underlying securities to get in line with the ETF or index. In general, the more often a fund rebalances, the closer it will track an index. Less frequent rebalancing increases the potential for drift from the benchmark. For example, if a small-cap fund has done really well from January to November, and the scheduled rebalancing is for December, it is likely that the fund in November will be holding more mid-cap and even large-cap stocks than when it started the year. This can happen with sector and style exposure as well. A sector may start out the year as 20% of the fund, and end the year at 30% of the fund because the sector has done well. If the fund was rebalanced on a monthly basis, the sector weight would be much closer to the 20% benchmark.

Conclusion

Knowing what you own should be one of your top priorities when selecting an investment vehicle. Many fund companies will provide all the information you need to evaluate a fund and determine if it is right for your portfolio.

For individual investors in a taxable account, expenses and taxation may seem like the most important factors. But while they should be considered, they shouldn’t be the only input. Knowing what the fund owns and how those components will meet your investment needs and affect the other holdings in a balanced portfolio is equally, if not more, important.

Related

Hot Links

Arnie Zimmer from VA posted over 13 years ago:

Earl Lash from CO posted over 13 years ago:

Earl Lash from CO posted over 13 years ago:

Robert Brown from MD posted over 13 years ago:

Tom O'Brien from IL posted over 12 years ago:

Charles Rotblut from IL posted over 12 years ago:

Warren Laird from KY posted over 12 years ago:

Chintan Bhatt from PA posted over 12 years ago:

Charles Rotblut from IL posted over 12 years ago:

Chintan Bhatt from PA posted over 12 years ago:

Cliff Rafter from FL posted over 12 years ago:

Charles Waldrop from TX posted over 12 years ago:

Ed Blansten from New York posted over 11 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account