Related

Financial Planning

by Carl Richards | March 2013

We just don’t know what will happen next. It’s a reality that can be hard to handle as an investor.

From fiscal cliffs and debt ceilings to unemployment rates and quarterly earnings, it can feel like we’re just along for the ride. And this feeling that we lack control, combined with uncertainty about the future, can make it very difficult to behave when it comes to investing.

Your goal for 2013 needn’t be finding the “best” investment or even the next Apple Inc. (AAPL). Instead, you (and your portfolio) should be better off if you focus on the things you can control and implement strategies that help you avoid classic investing mistakes.

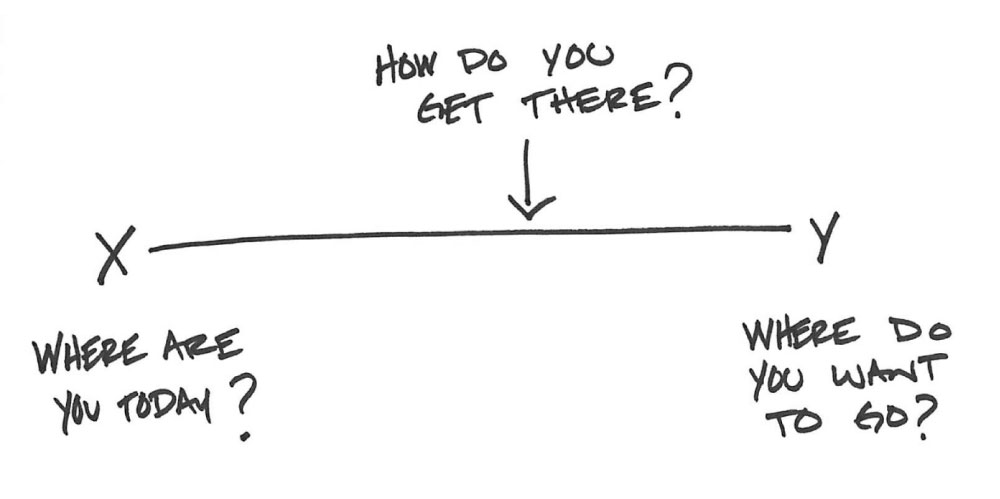

Does it really matter what the market did today if you don’t understand your current financial reality? Too often we get caught up in the news around investing and forget that the primary source of investing success comes from having a solid financial foundation.

But if getting clear about our current reality is so helpful, why haven’t we done it?

The best place to start is at the beginning by creating a personal balance sheet. Your goal is to discover where you stand financially right now. You don’t need a fancy spreadsheet or even a computer for this exercise. Just grab a blank piece of paper and a pen. Then draw a line down the middle.

On the left side, list all your assets in detail: bank accounts, the fair market value of your home, investment portfolio, etc. For every asset, list it and its value.

On the right side, list all your liabilities: credit card debt, mortgage, school loans, etc. Again, get specific and list the actual amounts of each liability (Figure 1).

If you don’t know the amount, call your bank, credit card company or your adviser. In this exercise, guessing isn’t allowed, so ask the questions and get the real numbers on paper.

Then, add up all your assets and subtract all your liabilities. You now have your net worth.

What does it look like? If you’re not happy with the number you see, you have two choices that will probably involve some hard work:

If you’re wondering why I suggest starting with something so simple, it’s because I keep crossing paths with people who don’t know how their assets compare to their liabilities. And the reality is that if you don’t know where you stand today, then how will you ever figure out where you want to be tomorrow?

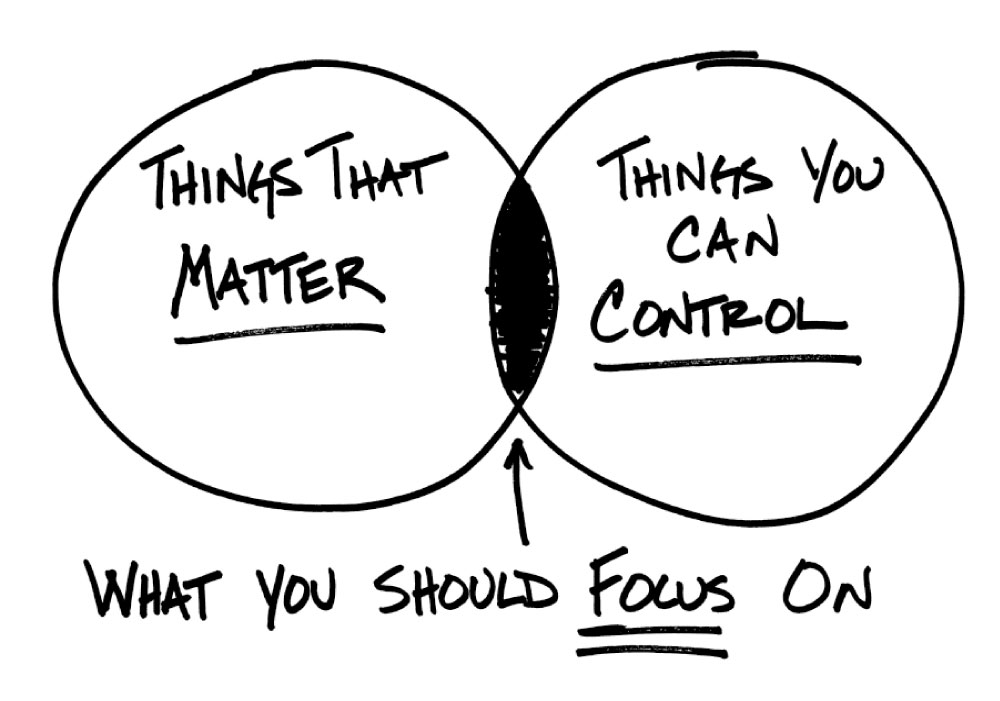

When you invest, all that matters is your financial goals. Not your neighbor’s goals, or those of the guy at work or your brother-in-law. But I often see one of two things happen:

When you invest, you need to do it with your financial future in mind and not anyone else’s (Figure 2). However, if you fall in the group where you’re feeling overwhelmed, here are some things to keep in mind to help you set goals that matter to you.

These goals are guesses.

While it is important to admit these are guesses, you should still make them the best guesses you can. Be specific. Just saying, “I want to save for college for my kids,” isn’t enough. How about, “I’ll find $100 to add to a specific 529 account on the 15th of each month”?

Even though you need to be specific, give yourself permission to be flexible. An attitude of flexibility goes a long way toward dealing with uncertainty. There is something very powerful about having specific goals but not obsessing about them.

These goals will change.

It’s a continuing process, and it will change because life changes. But don’t let this knowledge stop you from setting financial goals. You need to start somewhere.

Think of these goals as the destination on a trip.

You would never spend a bunch of time and energy worrying about whether you should take a car, train or plane without first deciding where you are going. Yet we spend countless hours researching the merits of one investment over another before we even decide on our goals. Why are you stressing about what stocks to pick if you don’t have goals in mind?

Prioritize these goals.

Once you have them all written down, rank each goal in terms of importance and urgency. Sometimes you will have to deal with something that is urgent, like paying off a credit card bill, so that you can move on to something really important, like saving money for retirement.

This is a process.

If you set goals and then forget about them forever, that is a worthless event. This is a process. Since we’ve given ourselves permission to change our assumptions about the future as more information becomes available, we need to do it. Part of the process of planning involves revisiting your goals periodically to see how you are doing and making course corrections when needed.

Let go!

As important as it is to regularly review your progress, it’s also very important to let go of the need to obsess over your goals. Define where you want to go, review your goals at set times and in between let go of them! Goals for the future are important, but so is living today. Find that balance.

Obviously, it’s easy to get distracted. And based on the questions I get, people are really distracted when it comes to money.

By asking just these questions we switch our focus to things we have at least some control over. We start to focus on our personal economy, instead of the global economy. Our personal economy becomes the filter for all the noise. Things like Europe, the market and individual stocks drop off our radar. Instead, we focus on information that helps us with the one thing we can control: ourselves (Figure 3).

Obviously with so much noise, it can be incredibly hard to get this focused. But the sooner you figure out the value of this filter, the faster you’ll be able to make sense of the noise.

We know the market will likely go up and down in the short term, yet people sometimes worry anyway about that fluctuation even if they don’t need the money for 20 years. Here are a few reasons why you may succumb to this behavior.

You’re not confident in your investment process.

If your portfolio is based on a thoughtful approach that relies on the best academic evidence we have, then it can be easier to stick with the long-term plan when things get scary in the short term. On the other hand, if what you own is a collection of random mutual funds instead of a well-designed, broadly diversified portfolio, it’s easy to get spooked. You start to wonder if the reason you’re losing money has something to do with the investment instead of just the normal ups and downs of the market.

You’re watching too much news.

Counteracting this one is simple, but not easy. Turn it off! Go on a media fast. If you’re confident in your investment process, what does the daily news about the markets do for you? Either ignore it, or get really clear about why you’re tuning in. Is it to be informed so you can have an intelligent conversation at dinner parties? Is it because you find it funny? I have a friend who refers to the Money section of USA Today as the “Funny” section. Whatever your reason for watching or following the news, just make sure you’re clear about it. If you’re watching out of habit and it makes you anxious, just stop it!

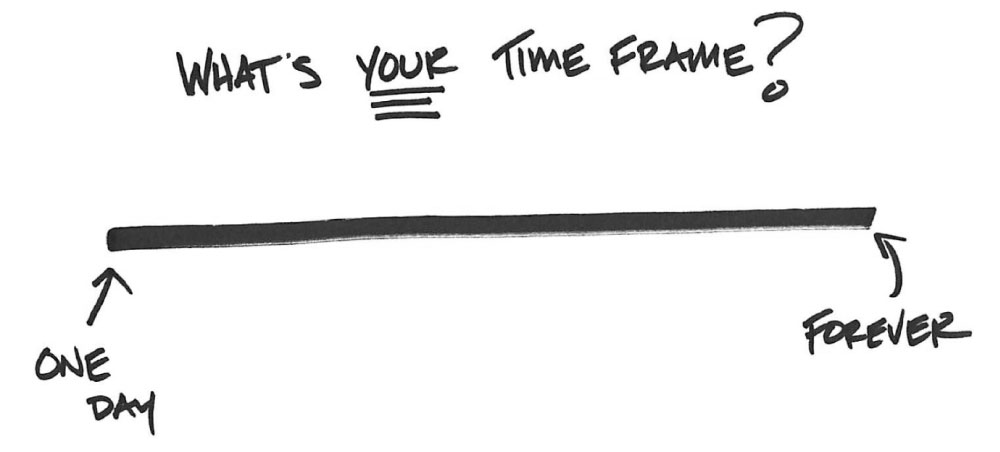

You’re listening to people with different time frames than yours.

Josh Brown has written about this issue on his blog, The Reformed Broker:

“Everyone has an opinion and there is a lot of smart stuff being said for long-term investors, short-term swing traders and day traders out in the Wide World of Market Punditry—but the trick is not just figuring out who’s right, it’s determining whether or not something is relevant to your time frame.”

If you’re an actual investor, and not a short-term trader, make sure the information you’re worrying about matches your time horizon. If you’re investing to pay for your kids’ educations 12 years from now, why do you care (at all!) about the latest apocalypse du jour?

You’re projecting the recent past into the future…forever.

This is a classic mistake, and one that is really easy to make. We are pattern-seeking animals and are notorious for looking at the recent past and thinking that it will last forever. We did it with tech stocks in the late 1990s, real estate in 2005 and now we’re just positive the European debt crisis will never, ever end. But remember, things change.

You think we’re all moving to the hills to grow our own vegetables no matter what we do.

I can’t help with this one. Until I learn differently, I still believe it’s in our best interest to be invested in a broadly diversified portfolio, since capitalism as we know it will not fall apart anytime soon.

Your timeline is your own. Not your neighbors’, your co-workers’ or your brother-in-law’s. So do yourself a favor and make investing decisions based on what your time frame requires and not what the talking heads on TV are saying to fill a 24-hour news cycle. You’ll sleep better and will hopefully feel a bit less like running to the hills (Figure 4).

At some point in our lives, most of us have done something that we knew ahead of time made no sense. (Just think back to your teenage years.)

After the fact, we’d shake our heads and wonder what we were thinking. Maybe it wasn’t our fault. Maybe the science shows that there are times when biology works against us and makes it difficult to act rationally.

In the case of investing, both the science and the anecdotes seem to back up the idea that sometimes our biology gets in the way of our ability to assess risk. That matters a lot when you’re investing, according to John Coates, who wrote about it at Time.com:

“…when we take risk, including financial risk, we do a lot more than think about it—we prepare for it physically. Body and brain fuse as a single functioning unit…[However] (e)ffective risk-taking morphs into over-confidence and dangerous behavior and traders on a winning streak may take on positions of ever-increasing size, with ever-worsening risk-reward trade-offs.”

Even Warren Buffett, known to encourage investors to be fearful when others are greedy, and to be greedy when others are fearful, isn’t immune to biology, according to Dan Ariely, a behavioral science expert:

“He is what behavioral economists call a sophisticate: someone who understands his irrationality and builds systems to cope with it.”

Since irrational behavior appears to come naturally to us, we need to be like Buffett and build our own coping systems:

Remember: there is rarely a time when investing skill matters more than investor behavior. So make your behavior count.

Financial Planning

Financial Planning

Financial Planning

Jeff Carlson from MN posted over 13 years ago:

James Joslin from NC posted over 13 years ago:

Peter Jochems from CO posted over 13 years ago:

Larry Taylor from SC posted over 13 years ago:

Durai Raghavan from TX posted over 13 years ago:

Ramesh Patel from OH posted over 13 years ago:

S Jones-Hendrickson from VI posted over 13 years ago:

Robert Lyon from NC posted over 13 years ago:

Winthrop Harewood from IL posted over 13 years ago:

Marvin Glenn from AR posted over 13 years ago:

Rudolph Heider from MO posted over 13 years ago:

Walter Curtis from WA posted over 13 years ago:

Floyd Wright from TX posted over 13 years ago:

Muriel Chandler from IL posted over 13 years ago:

Dennis Roubal from MI posted over 13 years ago:

John Flynn from FL posted over 13 years ago:

Leslie Sublett from KS posted over 12 years ago:

Hildy Richelson from PA posted over 12 years ago:

Richard Abbott from FL posted over 12 years ago:

Richard Abbott from FL posted over 12 years ago:

John Knox from AL posted over 10 years ago:

John Landry from TX posted over 10 years ago:

BARRY J from TX posted over 4 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account