Related

Portfolio Strategies

Individual investors underperform the mutual funds they invest in, but they can take advantage of psychological behaviors to improve their returns.

by Louis Harvey | October 2012

Back in 1993, a curious thought crossed my mind while analyzing the federal regulations that were new at the time.

Mutual funds were permitted to report investment returns for one, three, five and 10 years (“alpha”), but how many investors actually kept their investments unchanged for those specific periods? If all investors did not hold on to their investments for those precise periods, then they had to be doing better or worse than was being reported.

Alpha is a measure of performance on a risk-adjusted basis. Alpha takes the volatility (price risk) of a mutual fund and compares its risk-adjusted performance to a benchmark index. The excess return of the fund relative to the return of the benchmark index is a fund’s alpha. Simply stated, alpha represents the value that a portfolio manager adds to or subtracts from a fund’s return. Investors’ alpha is the value a retail investor adds to or subtracts from the alpha delivered by the portfolio manager. The return of the respective index is considered to be zero alpha, so any excess over the index is considered positive investor alpha.

I developed a calculation that would measure whether mutual fund investors were actually earning more or less than the reported alpha. In 1994, DALBAR issued the first Quantitative Analysis of Investor Behavior (QAIB), showing that investors had severely underperformed the average mutual fund alpha! This underperformance continues to this day.

Investors were actually missing much of the alpha that mutual funds had earned. Using the S&P 500 index to approximate the returns that equity mutual funds produced, investors were leaving between 10.97% and 4.32% on the table, as Table 1 shows.

This shocking finding of underperformance led to research to understand how and why millions of investors were missing so much of the alpha and, ultimately, what they could do to capture more of the profits that funds were earning.

The first breakthrough came when we discovered how long investors kept their money in equity mutual funds. If the money was not invested, then the profits would be lost. We found that instead of holding investments for 20 years or more, investors were in and out in as little as two to three years. It was clear that investors had to remain invested for a longer time period if they were to capture more of the alpha of mutual fund managers.

We then discovered the pattern of behavior that led to the short time horizon. It was simple enough. We found that investors withdrew funds in greater volume following a market decline, thus losing much of the profits they had earned. This meant that mutual fund investors were selling investments long after the large institutions had taken their profits!

Almost as destructive as withdrawing in a down market was waiting for the market to recover to start investing again. Yes, we proved by our investigations that investors were adding to their investments when the prices were highest and withdrawing when prices were low.

This pattern was repeated month after month since 1984, which was as far back as the data we had allowed us to analyze. Months of down markets were followed by outflows and after months of up markets, the inflows accelerated.

Table 1. Investors Underperform the Market by Big Margins

|

20-Year Period Ending |

S&P 500 (%) |

Average Equity Fund Investor (%) |

Difference (%) |

|---|---|---|---|

| 1998* | 17.18 | 6.71 | (10.47) |

| 1998* | 17.9 | 7.25 | (10.65) |

| 1999* | 18.01 | 7.23 | (10.78) |

| 2000* | 16.29 | 5.32 | (10.97) |

| 2001* | 14.51 | 4.17 | (10.34 |

| 2002* | 12.22 | 2.57 | (9.65) |

| 2003 | 12.98 | 3.51 | (9.47) |

| 2004 | 13.2 | 3.7 | (9.50) |

| 2005 | 11.9 | 3.9 | (8.00) |

| 2006 | 11.8 | 4.3 | (7.50) |

| 2007 | 11.81 | 4.48 | (7.33) |

| 2008 | 8.35 | 1.87 | (6.48) |

| 2009 | 8.2 | 3.17 | (5.03) |

| 2010 | 9.14 | 3.83 | (5.31) |

| 2011 | 7.81 | 3.49 | (4.32) |

| *The analysis begins in 1984 so that from 1997–2002, the period covered is less than 20 years. Since 2003, the long-term analysis has covered a 20-year time frame. | |||

But why would mutual fund investors act so irrationally? Were they being advised to do this? After interviewing several hundred investors after market downturns, the finding was clear. Investors decided to get out of their investments to avoid further losses. They lacked the confidence that the market would rise again and restore the value that once was theirs. This phenomenon was later described as the psychological behavior of “loss aversion.”

On the other hand, confidence was restored after months of rising markets and at that point the inflows resumed. This phenomenon was later attributed to the psychological behaviors of “herding” and “media response.”

Table 2. Psychological Behaviors Affecting Investor Returns

|

1 |

Loss Aversion |

Expecting to find high returns with low risk. Loss aversion causes the investor to search for investments that don’t exist and results in either taking no action or later discovering that the selected investment fails to meet the expectation. The effect is often selling the investment at an imprudent time, which adversely affects the alpha that professional investment managers create. |

|

2 |

Narrow Framing |

Making decisions without considering all implications. The result is quick decision-making with the consequence that facts are uncovered after inappropriate investments are made. Investors make precipitous investment changes, which can lose alpha. |

|

3 |

Anchoring |

Relating to the familiar experiences, even when inappropriate. Anchoring is a very powerful communication method but can mislead investors unless it is used with caution. For example, investors can be misled about the stability of an investment if analogies are used to represent stability. Analogies of growth can also lead to unrealistic beliefs and expectations. Alpha can be lost by selecting investments that cannot reasonably be expected to produce the expected alpha. |

|

4 |

Mental Accounting |

Taking undue risk in one area and avoiding rational risk in others. Used wisely, mental accounting can permit an investor to achieve high alphas in one area, while protecting assets for other purposes. Imprudent use of mental accounting can be as damaging to alpha as any other psychological factor since investors can be misled into inappropriate investments. |

|

5 |

Diversification |

Seeking to reduce risk, but simply using different sources. This extremely valuable investment strategy can also be misused to create a false sense of protection that results in alpha-killing actions. |

|

6 |

Herding |

Copying the behavior of others even in the face of unfavorable outcomes. Investors who go along with the crowd simply because there is a crowd tend to avoid catastrophic errors, but seldom achieve above-average results. Alpha is not achieved by herding. |

|

7 |

Regret |

Treating errors of commission more seriously than errors of omission. Investors who fear decision-making lose alpha through inaction or reversals. Inaction can prevent losses caused by poor decisions, but is unlikely to produce alpha for the investor. |

|

8 |

Media Response |

Tendency to react to news without reasonable examination. Familiar media sources have become less reliable as they compete with newer, faster and lower-cost outlets. At the same time, new media outlets seldom have very thorough authentication. This question of reliability raises the concern about reacting to news. |

|

9 |

Optimism |

Belief that good things happen to me and bad things happen to others. Optimistic investors hold on to investments after it becomes evident that losses are not likely to be recovered. Holding on to poor investments is yet another way psychological factors can reduce alpha. |

Further research showed that loss aversion, herding and media response were not the only forces that caused the loss of profits. In all, we found that there were nine psychological behaviors that were to blame for the underperformance in one way or another. Table 2 defines the nine psychological behaviors that affect investor returns.

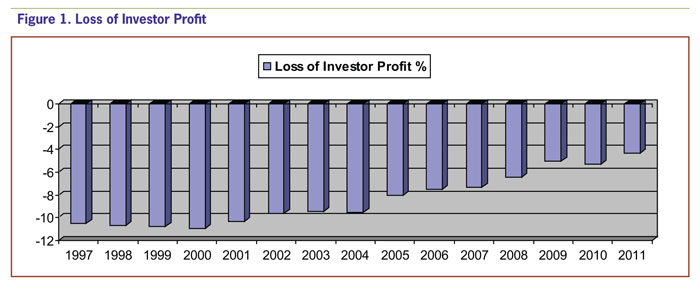

With the problem clearly identified, the solution seemed simple, at first. If investors were taught to make rational decisions, they could avoid the psychological traps. After years of investor education, there was some improvement, as can be seen in Figure 1, but the basic problem remained. The market meltdown of 2008 was solid evidence that investors still reacted to their psychological instincts.

Figure 1. Loss of Investor Profit

Further research was clearly necessary. This research led to another way of making better investment decisions. Instead of trying to change psychological behaviors, this new approach takes advantage of them. Specifically loss aversion, narrow framing and mental accounting are deployed. The psychological strategy is to protect the portions of investments that are most critical to the investor, while permitting risks with portions where time will permit losses to be recovered.

The term for this strategy is purpose-based asset management (PBAM), in which investors subdivide investments and associate each subdivision with a specific purpose. In this way, each subdivision can be assigned a different risk tolerance and invested accordingly. For example, one subdivision might be “minimum acceptable retirement income,” which would be very conservatively invested. The subdivision for the purpose of “inheritance” could be more aggressively invested.

The result of this purpose-based system is that the loss aversion is avoided for the minimum retirement income, while the short-term ups and downs of the inheritance portfolio are tolerated without the temptation to sell at the worst-possible times.

Implementing PBAM is actually quite simple, but it does require some discipline to start. Here are the steps:

Define each major purpose of funds and for each determine:

Approximate time frame when funds will be needed;

Minimum needs:

Lump sum that will be needed,

Monthly payments that will be needed and

Duration of monthly payments that will be needed; and

Arrange purposes in order of importance, taking each minimum and maximum separately—for example, minimum retirement income may be more important than minimum education, but optimum retirement income may not be.

Identify the available sources of funds:

Using the prioritized list, assign funds to each purpose in order of priority from available sources. Stop when funds are exhausted. Only those purposes that are funded can be considered.

Develop an investment plan that includes:

Investors using PBAM have selected a variety of purposes to allocate investments, including:

Adopting PBAM assures that investments are properly deployed and the panic of market volatility can be weathered with the confidence of knowing that you are not losing alpha and that the essential funds are protected.

It is hoped that over the next decade, investors will use prudent investment strategies, such as purpose-based asset management, to avoid the tragic loss of reacting emotionally without the safety net of a program that incorporates investor psychology.

Portfolio Strategies

Owen Newcomer from CA posted over 13 years ago:

Bob Stein from OH posted over 13 years ago:

Edward Spitzer from PA posted over 13 years ago:

William Orlowski from WI posted over 13 years ago:

Kim Bedell from NC posted over 13 years ago:

Richard Ballew from CA posted over 13 years ago:

Maureen Gill from NJ posted over 13 years ago:

Thomas Keon from PA posted over 13 years ago:

Robert Carr from NY posted over 13 years ago:

Robert Anderson from CA posted over 13 years ago:

Stephen from FL posted over 13 years ago:

Douglas Johnson from TX posted over 13 years ago:

Charles Comereski from NY posted over 13 years ago:

Richard Vroman from CA posted over 9 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account