Related

Stock Strategies

The first article in this popular series explains what the income statement, balance sheet and cash flow statement are and how they are interconnected.

by Joe Lan | January 2012

Understanding financial statements is key to fundamental stock analysis and overall investment research. Financial statements provide an account of a company’s past performance, a picture of its current financial strength and a glimpse into the future potential of a firm.

This is the first in a new AAII Journal series on financial statement analysis. The goal is to enhance your ability to make a sound judgment about a company’s financial strength and future prospects by showing you the benefits of using financial statements in your personal investment research.

Given the varied financial knowledge of our readers, I will address many topics that some may find very basic. However, to build a strong understanding of advanced topics, you need a solid foundation. As we progress through this series, I expect to touch on more advanced topics when explaining how I personally use financial statements to analyze a firm. In this introductory article, I explain the major components of each financial statement and why they matter in security analysis.

The role of financial reporting for companies is to provide information about their fiscal health and financial performance. As investors, we use financial reports to evaluate the past, current and prospective performance and financial position of a company. These statements allow us to compare one firm to another and form the basis of valuing the worth of a stock.

Several financial statements are reported by companies. The most important three, and the three used most often by investors, are:

The income statement reports how much revenue the company generated during a period of time, the expenses it incurred and the resulting profits or losses. The basic equation underlying the income statement is:

revenue – expenses = income

All companies use a reporting period of one year, which can start and end at the same time as a calendar year, or could start and end at different point in the year (the firm’s fiscal year).

There are several important pieces of information on the income statement that are relevant to stock analysis. Investment analysts use the income statement to monitor revenues, expenses and profits and their trends over time. The direction and rate of change in not only profits but also “top-line” revenue influence the valuation of the firm. The rate of growth, and whether it is accelerating or decelerating, for both revenue and net income, is a critical component in stock valuation. Investors often reward high-growth companies with a higher valuation.

Near the bottom of the income statement is earnings per share. Earnings per share is simply the earnings the company generated per share of outstanding company stock. This is the figure used in the denominator of the price-earnings ratio, a key ratio used frequently in investment analysis.

An example of an income statement can be seen in Figure 1. This is a consolidated statement from cereal maker Kellogg Company (K), meaning that results from the company’s divisions and subsidiaries are included in the results. The statement is also condensed, meaning that some line items have been grouped together for the purpose of brevity.

You can conduct a preliminary analysis by looking the very top and near the bottom of the statement. The first line reports revenue (labeled “net sales” on Kellogg’s statement). Near the bottom you see the net income line and the earnings per share section (labeled “per share amounts” on Kellogg’s statement). You want to see these numbers increasing over time.

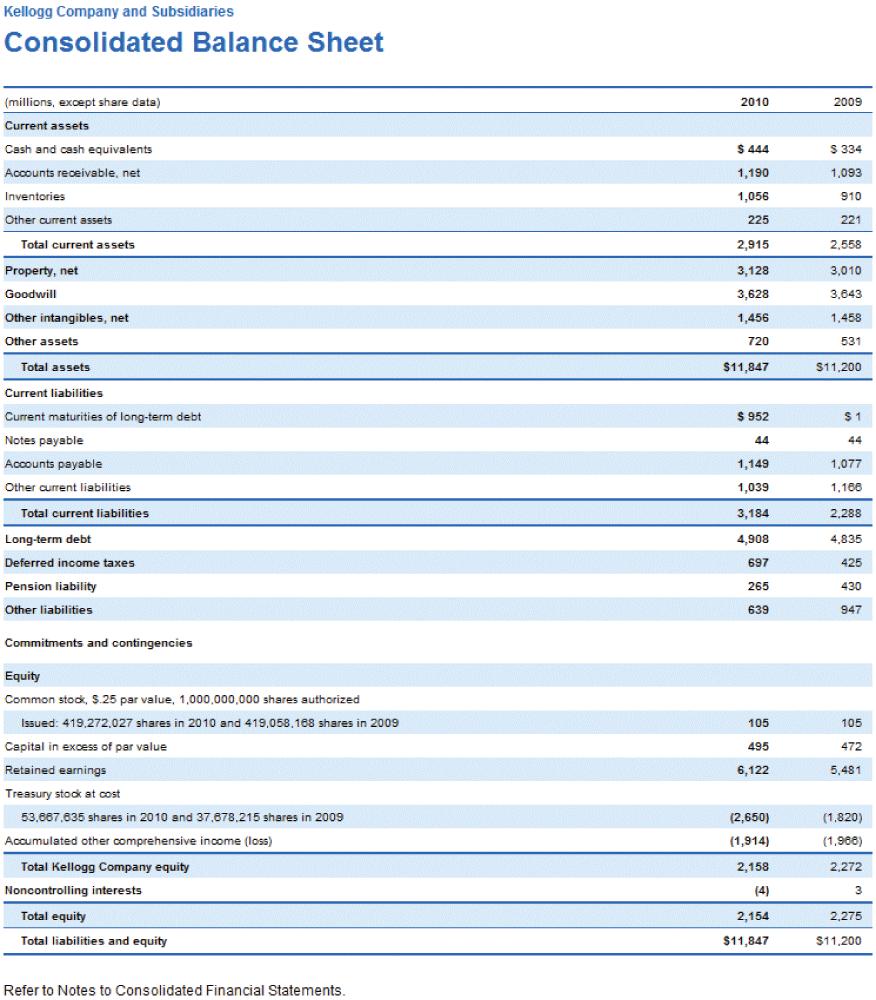

Although the income statement may be the most popular financial statement, the balance sheet provides vital information on a company’s financial position. In contrast to the income statement, which provides revenue and earnings data over a period of time, the data contained in the balance sheet is a snapshot for a specific date.

The balance sheet provides information on what a company owns (assets), what it owes (liabilities), and the shareholder ownership interest (equity). The equation underlying the balance sheet is:

assets = liabilities + equity

Analysts use balance sheets to determine trends in assets and liabilities and to ascertain how adequately the firm is financed. For example, trends in inventory (an asset) and supplier invoices (“accounts payable,” a liability) can provide insight on product demand and the ordering patterns of the firm. An increase in inventory can suggest that a company is gearing up for an expected increase in product demand. However, analysts must be cognizant that holding too much inventory can be problematic.

In addition, the balance sheet shows changes in a firm’s debt and provides clues as to whether the firm is becoming too highly levered. The shareholder’s equity determines the valuation of a firm by providing the book value (which is used as the denominator in the price-to-book ratio), or theoretical value left for the shareholders in event of liquidation.

An example of a balance sheet is presented in Figure 2. (Again, Kellogg is using a consolidated statement.) The top half is always assets, led with the cash balance on the first line. The second half shows liabilities, including long-term debt. At the very bottom is equity. As the company grows, so should equity. Small fluctuations will occur from year to year, however, because the balance sheet tabulates assets and liabilities for a single day.

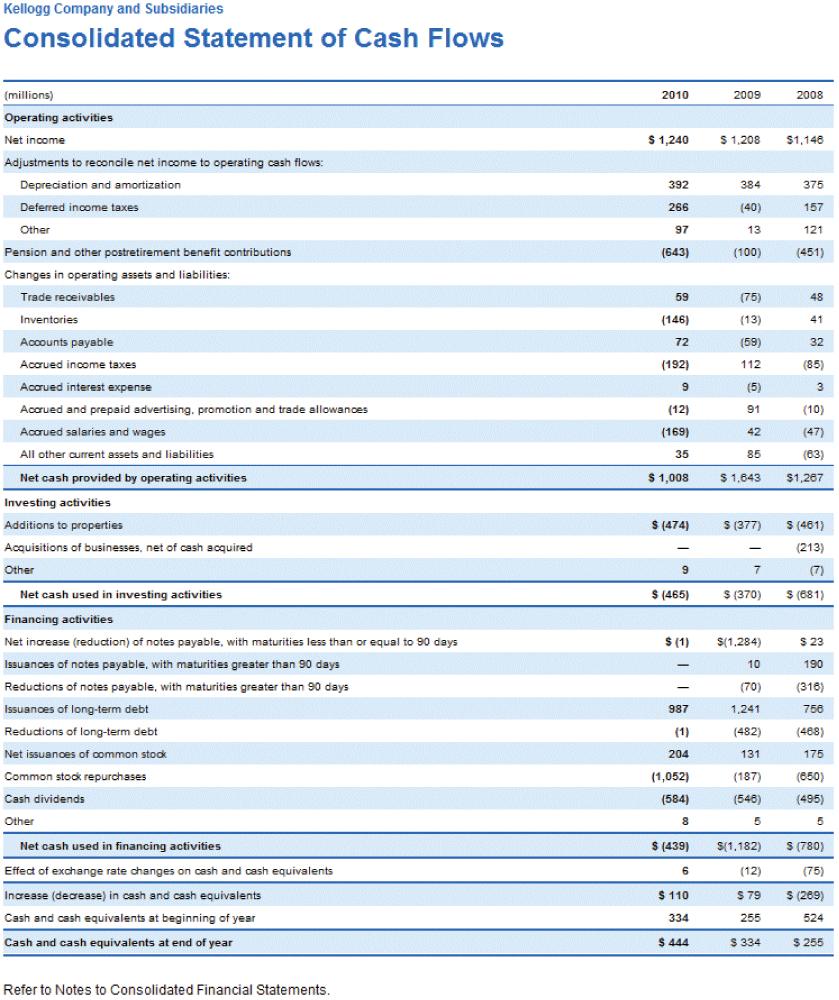

The cash flow statement is the third major financial statement provided by companies. This financial report tabulates how much cash is coming in and going out of the firm. When it comes to financial statements, cash is entirely different from profits. A firm can easily generate healthy profits without generating sufficient cash.

There are three major elements in the cash flow statement:

Cash flow from operating activities encompasses cash generated from a company’s day-to-day operations. The simplest example would be cash inflows resulting from sale of a product for cash, which would represent an increase in cash flow from operating activities. Offsetting this would be money spent to manufacture products, pay suppliers and pay employee salaries, which would mark a decrease in cash from operating activities.

Analysts are very interested in cash flow from operations because it represents the exact amount of cash the firm has been able to generate using its core business operations. Increasing profits while cash flow from operations is shrinking is a potential red flag.

Cash flow from investing activities pertains to the purchasing and selling of investments. Investments include property, plant and equipment and other long-term assets, as well as both long- and short-term investments in equity and debt issued by other companies. Generally, when management feels there is strong demand for products and growth is expected to be robust, cash outflows from investing activities will increase as the firm gears up production.

Finally, cash flow from financing activities covers obtaining or repaying capital. Cash inflows from financing activities include the sale of stock and issuance of debt. Cash outflows include stock repurchases, the issuance of dividends, and the repayment of bonds or other long-term debt.

Analysts keep a watchful eye on cash flow from financing for a variety of reasons. An increase in debt financing can generate additional value for shareholders if profits are successfully generated from the borrowed capital. As always, analysts must be cautious when firms are showing significant increases in debt. Alternatively, a company buying its own shares may indicate management’s willingness to return cash to shareholders, or it may signal management’s belief that the company’s shares are undervalued.

Net cash flow is the total sum of cash flow from operations, cash flow from investing, and cash flow from financing. This figure is the basis of numerous cash flow valuation models; analysts often use cash flow as a basis to develop target prices for the company’s stock.

An example of a cash flow statement, also from Kellogg, is presented in Figure 3. Positive numbers indicate a net inflow of cash and negative numbers (those in parentheses) indicate a net outflow. Positive cash from operating activities is good, though negative cash from investing activities and financing activities can also be good if they are not excessive and represent money spent in the best interests of shareholders.

Perhaps the best way to explain the link between these three financial statements is to consider a simplified example of a firm’s operating activity. Let’s take, for example, a manufacturer of widgets, and detail what happens when a widget is manufactured and sold.

Before a widget can be sold, it must be manufactured. A firm needs to raise and spend money to build a manufacturing plant, buy the raw materials to produce the widget, and then manufacture the widget. This affects two financial statements—the balance sheet and the cash flow statement. On the balance sheet, cash, fixed assets (plant, property and equipment) and inventory increase. On the cash flow statement, all three sections are affected. There is an outflow from cash from operating activities as cash is spent in order to manufacture the widget. There is an outflow from cash from investing activities, as the company builds a plant that will be used for the future manufacture of widgets. Finally, an inflow is recorded in cash flow from financing as the firm raises money by issuing debt.

Next, the widget is sold on account. In this step, the widget leaves the company after it is sold to a customer. However, since the customer is billed for the widget no cash is received. This step affects the income statement and the balance sheet. On the income statement, revenue increases, and so do expenses. The balance sheet is also affected as inventory decreases by the amount of widgets sold and accounts receivable increases by the customer invoice or widgets sold on account.

Finally, cash is collected from the sale and may be used to pay down the debt incurred in the first step and to pay owners through dividends. In this step, the balance sheet and the cash flow statement are affected. On the balance sheet, cash increases and accounts receivable (an accounting of invoices owed by customers) decreases. The cash flow statement shows an increase in cash flow from operations.

If a dividend is then paid to shareholders and some of the cash from the sale is also used to pay down debt, the cash amount listed on the balance sheet decreases. On the cash flow statement, a cash outflow from financing activities occurs from payment on debt and the distribution of dividends. There is no change to the income statement because the revenue and expense from the sale of the widget has already been recognized (the revenue and expenses were recognized when the sale was made and accounts receivable increased).

As you can see, the three financial statements are linked together when a transaction is completed by a firm. The process is admittedly complex, and many of the parts that compose it will be addressed through additional detailed examples in future articles in this series.

Even so, it is vital to look at all three statements when establishing the financial health of a firm. In a very extreme case, a firm can sell its entire inventory on account and never bother to collect the cash. The income statement can look very healthy as sales are being made and revenues and expenses are recognized. However, the balance sheet will provide a hint of trouble as the company’s accounts receivable continues to climb. The problem can be verified from the cash flow statement: It would show continued outflows of cash from operating activities as cash is spent on raw materials and manufacturing, yet no cash is collected from sales on account.

Financial statement data is available at a number of comprehensive financial websites, such as Yahoo! Finance, SmartMoney.com and Morningstar.com, as well at AAII.com. These sites have locations on their home pages where you type in a stock’s ticker symbol or name to access all the data they offer on that company. Be sure to note that most websites provide condensed financial statements and that not all line items for each financial statement are displayed. In addition, due to differences in how certain line items are categorized, some numbers may not correspond exactly with what you see in a company’s annual report.

AAII’s Stock Investor Pro fundamental stock screening and research database program also provides financial statement data (www.aaii.com/stock-investor-pro). It carries income statement, cash flow statement and balance sheet data for the previous eight quarters and for the previous seven years.

When a company announces earnings each quarter, a press release is issued that reports the latest revenue and earnings numbers. Some earnings press releases will also include the income statement, balance sheet and cash flow statement, while others may not have all three statements. These press releases can be found on many financial websites and on the issuing company’s own website.

Company annual reports include financial statements for the most recently completed year; they usually also present financial data for the past few years. Annual reports can be found on a company’s corporate website.

Alternatively, you may find financial statements filed at the U.S. Securities and Exchange Commission (SEC) by using EDGAR (Electronic Data Gathering, Analysis, and Retrieval system). EDGAR is accessed at www.sec.gov/edgar.shtml.

Companies are required by the SEC to file several forms. The Form 10-K is the annual report and gives a comprehensive overview that includes all of the company’s financial statements and financial disclosures. In the interim, companies are required to file Form 10-Q, which is a quarterly financial update. The 10-Q only presents certain financial information, and the financial statements in this report can be unaudited.

Another form that often contains financial information is the proxy statement. A proxy is an authorization from the shareholders giving another party the right to cast its vote. The SEC requires that companies provide shareholders with a proxy statement (Form DEF 14A) prior to a shareholder meeting.

Two sets of accepted standards and governing bodies exist for financial reporting, one for the United States and one international standards.

In the United States, the Financial Accounting Standards Board (FASB) is an organization whose primary purpose is to develop and update the generally accepted accounting principles (GAAP).

U.S. companies are required to follow GAAP; however, many firms report non-GAAP (“pro-forma”) figures in their earnings announcement press releases. Companies report non-GAAP figures because they are believed to be more representative of performance. Firms reporting non-GAAP figures are required to reconcile the figures back to GAAP.

The standard-setting body responsible for developing international financial reporting standards (IFRS) is the International Accounting Standard Board (IASB). The different account standards means that differences exist between how U.S.-listed and foreign-listed companies report their results.

The next article in this series, which will appear in the March AAII Journal, will provide a comprehensive review of the income statement. All the major line items will be discussed, as well as the key income statement figures.

The Income Statement: From Net Revenue to Net Income, March 2012

The Balance Sheet: Assets, Debts and Equity, May 2012

The Cash Flow Statement: Tracing the Sources and Uses of Cash, July 2012

16 Financial Ratios for Analyzing a Company’s Strengths and Weaknesses, September, 2012

Stock Strategies

Financial Planning

Stock Strategies

Steven from IA posted over 14 years ago:

Gerald from GA posted over 14 years ago:

Ray from MT posted over 14 years ago:

Curtis from NC posted over 14 years ago:

Adam from IL posted over 14 years ago:

Robert from TN posted over 14 years ago:

Michael from Illinois posted over 14 years ago:

Steven from IA posted over 14 years ago:

Pranav from NY posted over 14 years ago:

Pavan from MI posted over 14 years ago:

Sue from TX posted over 14 years ago:

Roland from MA posted over 14 years ago:

Roland from MA posted over 14 years ago:

Roland from MA posted over 14 years ago:

Ronald from LA posted over 14 years ago:

John from VT posted over 14 years ago:

Sandra from CA posted over 14 years ago:

Juan Ortega from TX posted over 13 years ago:

J Padulo from NJ posted over 13 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account