Featured Tickers:

For value investors, the sweet spot in investing is being able to buy an undervalued stock right before its value is recognized by the market and just before its stock price begins to take off.

But how can a value investor tell when a stock is in the sweet spot? The answer, according to Brian Nelson, president of investment research company Valuentum Securities, is to identify stocks with good value that are just starting to exhibit good technical/momentum characteristics.

Doing so helps an investor avoid:

- value traps: stocks whose prices continue to fall—so-called “falling knives”—or stocks whose value will never be recognized by the market,

- underperformance due to the opportunity cost associated with holding a stock with great potential, but whose value takes an inordinate amount of time to be recognized by the market and

- speculative momentum or irrational high-yielding stocks whose technicals are unsupported by their fundamental valuation (“greater fool” stocks).

Many investors often base their investment decision on whether a stock is undervalued or overvalued or whether it has excellent competitive advantages or other qualitative measures. Nelson believes this a great start but it’s an incomplete assessment, as stocks can stay undervalued or overvalued for decades (and some stocks may never converge to an estimated intrinsic value). Only when there is buying or selling in the stock based on its overvalued or undervalued state does a stock actually converge to its intrinsic value. Investors are highly dependent on other investors’ actions (buying a stock drives its price higher, all else equal).

This core market dynamic is why Nelson looks for undervalued stocks that are just starting to be bought by other investors, the latter evidenced by a stock’s positive technical/momentum considerations. He does not believe it is enough for a stock just to be undervalued. When it takes too long for a stock’s value to be recognized by the market, both the power of compounding and the stock’s annualized rate of return are adversely affected. A 30% return in nine months, for example, is far better than a 30% return over five years. Investors who focus only on value, growth or competitive-advantage analysis may not be using everything in their tool kit to maximize returns.

The value school of investing has seen this happen before. For a long time, “value investing” and “growth investing” were mistakenly viewed as separate and incompatible styles of investing. Legendary investor Warren Buffett debunked this myth when he said, “Growth and value investing are joined at the hip. Value is the discounted present value of an investment’s future cash flow; growth is simply a calculation used to determine value.” Similarly, some value investors have viewed value and momentum as being likewise incompatible investment strategies, even though there is a benefit to combining them.

As a common example, value investors have traditionally been conditioned not to accept technical/momentum analysis. Price movement strategies have often been dismissed as a self-fulfilling prophecy, the belief that they only work because other investors are buying and selling based on technical/momentum indicators. Nelson argues that this isn’t a balanced view of the markets. Value investing works sometimes because people buy or sell based on value principles, driving a stock higher or lower, respectively. An understanding of these market dynamics helps investors relate to the theory behind why stocks admired by both value (inclusive of growth) and technical/momentum investors can be attractive. The possibility of price-to-fair-value convergence for this cohort of stocks is enhanced.

Research Says Combine Value With Momentum

Several research studies—most notably a study done by Cliff Asness of AQR Capital, Tobias Moskowitz of the University of Chicago and Lasse H. Pedersen at the New York University in their paper “Value and Momentum Everywhere”—make the argument that value and momentum strategies work well together. In their research, Asness, et al. show that over time combining value and momentum strategies across diverse markets and asset classes results in significantly higher risk-adjusted rates of returns.

Modern portfolio theory indicates that when you combine assets that are not perfectly correlated, or move in opposite directions, both portfolio volatility and overall risk are reduced. By applying this same sort of thinking to combining the best elements of two seemingly incompatible investment strategies—value and momentum—Asness, Moskowitz and Pedersen found that an investor can garner significant benefits of diversification by combining the best elements of value and momentum strategies. In their research, Asness, et al. found “that value (momentum) in one asset class is positively correlated with value (momentum) in other asset classes, and value and momentum are negatively correlated within and across asset classes.”

Source: Research paper by Clifford S. Asness, Tobias J. Moskowitz and Lasse H. Pedersen, “Value and Momentum Everywhere,” February 2009.

Moskowitz in his October 2012 article “A Better Bet,” published by the University of Chicago, makes the point that generally a value investor can expect to outperform the market by about 3% to 4% a year, while a momentum investor is likely to outperform the market by about 4% to 5% per year. He goes on to point out that combining value and momentum strategies outperforms on average by 5% per year. This may not look like much of an advantage over using either value or momentum alone, but portfolio volatility is reduced by about 50%.

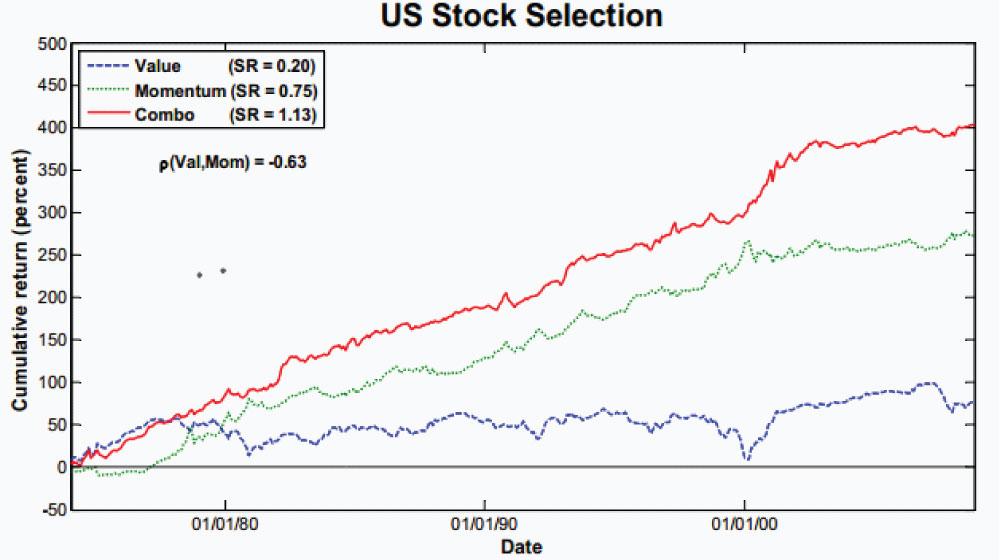

Figure 1 is from the Asness, et al. study and shows the cumulative returns and Sharpe ratios for the period from January 1975 through July 2, 2007, for each of the three strategies. The blue Value line represents the returns of a long-short portfolio. This portfolio was long stocks with good value characteristics (a high ratio of book value to market value, or the inverse of the price-to-book ratio) and shorted stocks with poor value characteristics (a low ratio of book value to market value). The Momentum green line is a long-short portfolio that is long stocks that have performed well recently and short those stocks with poor momentum characteristics. The red Combo line shows cumulative return over this period for a portfolio that is a 50/50 combination of value and momentum.

Why These Styles Complement Each Other

Figure 1 shows that the 50/50 combination portfolio of value and momentum produces better cumulative long-term returns and better risk-adjusted long-term performance. The logical question though is, why? The answer that Moskowitz offers in his article “A Better Bet” is that while value and momentum appear to be at odds with one another, it is this very opposition to one another that accounts for the reason they seemingly work so well together. He explains that momentum investing works well in the short term—a year or less—while value investing focuses on the long term. Combining value and technical/momentum characteristics is also a long-term proposition, as it is conditioned on price-to-fair value convergence (the value premise).

The example Moskowitz gives is that during the technology boom of the mid-1990s momentum investors produced much better returns than value investors, who stayed away from technology stocks. But when the technology stocks crashed and burned, value investors generated better returns because they were invested in a completely different group of stocks. He suggests that a strategy that combined value and momentum in a situation like this would have allowed an investor to profit from these market extremes without being exposed to the probability of a major loss.

The conclusion of the Asness, et al. study is that the negative correlation between value and momentum strategies coupled with their high expected returns make a simple strategy of equally weighting a portfolio with value and momentum stocks a powerful strategy that produces higher cumulative long-term rates of return than either value or momentum alone (across every asset class). The Asness study also points out that combining value and momentum results in a significantly higher Sharpe ratio than either a value or momentum strategy alone and makes the portfolio less volatile across markets and time periods. [The Sharpe ratio measures how much return a strategy generates relative to the level of risk it incurs. Higher Sharpe ratios imply a strategy produces more return for each unit of risk. To learn more about the Sharpe ratio, see “Interpreting the Sharpe Ratio” in the May 2013 AAII Journal.]

How Investors Can Combine the Strategies

Though Asness, et al. used a 50/50 combined long-short value and momentum strategy and recommended applying it to a large number of stocks, such a strategy is not practical for the individual investor. Nelson, however, has an idea for a similar strategy that individual investors could follow.

In much the same way that Hall of Fame baseball player Ted Williams wrote about pitches being in his strike zone, Nelson believes it is the cohort of good value and good momentum stocks on the long side and poor value and poor momentum stocks on the short side that are the major drivers of the outperformance when value and momentum strategies are combined. To ferret out those stocks that are likely to be in the investor’s strike zone, his methodology utilizes certain value and momentum signals.

Value Signals

To identify stocks that appear to be undervalued, Nelson primarily utilizes a three-stage discounted cash flow (DCF) model. This model is used to estimate a company’s intrinsic value by calculating the present value of future expected cash flows. He also utilizes a relative value approach. A stock is considered to be undervalued if it has a low price-to-earnings ratio and a low price-earnings-to-growth (PEG) ratio compared to the median for industry peers. Though an individual investor could simply use a low relative price-earnings ratio and a low PEG ratio to identify stocks with good value characteristics, including a DCF model will provide a more comprehensive valuation analysis.

Academic research and Nelson’s research also suggest that value metrics such as a high book-to-market-value ratio (the inverse of the price-to-book ratio) or a low EV/EBITDA ratio are useful indicators for an investor to focus on. Enterprise value (EV) is the cumulative value of market capitalization, short-term debt, long-term debt, minority interest and preferred equity less cash. Earnings before interest, taxes, depreciation and amortization (EBITDA) is often used as a proxy for cash flow. The EV/EBITDA ratio is the valuation ratio a would-be buyer might assign to the entire company.

Nelson’s methodology also utilizes a relative value approach and considers a stock to be undervalued if it has a price-earnings ratio and price-earnings-to-growth (PEG) ratio below average for its industry peers. This relative value approach is coupled with the low price-to-book ratio or low PEG ratio metrics to provide a more comprehensive valuation analysis. Based on his research, it appears that a high book-to-market value ratio (a low price-to-book ratio), a low EV/EBITDA multiple, a low relative price-earnings ratio and a low PEG ratio are useful value signals that an individual investor can use to identify stocks with good value characteristics.

Momentum Signals

There is a considerable amount of academic research suggesting that relative returns can signal whether future price performance will be above or below the market’s return, particularly over the next six to 12 months. (Examples include “Momentum” by Narasimhan Jegadeesh and Sheridan Titman, 2001, and “Momentum Strategies” by Louis K. C. Chan, et al, 1996). Eugene Fama at the University of Chicago, was quoted in the Financial Analyst Journal last year as saying, “Of all the potential embarrassments to market efficiency, momentum is the primary one.”

In trying to identify stocks with good momentum characteristics, Nelson generally uses four factors. The first are moving averages, with an emphasis on situations where the shorter-term moving average crosses a medium- or longer-term moving average from below (a bullish signal). The second is the money flow index (MFI), which is an oscillator that uses price and volume to measure buying and selling pressure. Chartists often look for an overbought signal, above 80, and an oversold signal, below 20, to indicate unsustainable near-term price extremes. The third is the accumulation/distribution ratio. A heavy accumulation (buying) or distribution (selling) week can signal the future near-term direction of the firm’s share price as investment dollars continue to move in or out of the stock in the days and weeks ahead and drives the stock price up or down, respectively. The final indicator is upside/downside volume. The level and trend of the upside/downside (U/D) volume ratio indicates whether institutional participation has been bullish or bearish recently.

Low, Not High, Turnover

The biggest benefit of a combined value-momentum strategy is that the approach allows an investor to improve his or her entry and exit points on the most undervalued stocks. A combination of the two strategies can be used to help weed out the value traps and “dead-money” ideas to bolster overall returns. Such a strategy doesn’t require value investors to abandon what they’re currently doing, but rather simply overlays a timeliness assessment to augment performance. Focusing on the very best (timely) opportunities in the traditional value portfolio can result in an even more concentrated, low turnover portfolio, which can result in less tax and less transaction costs and better long-term performance. For Nelson, most turnover occurs as a result of a value trigger, meaning the stock is no longer undervalued, as opposed to a momentum trigger, such as a negative assessment of a stock’s moving averages.

Testing the Strategy

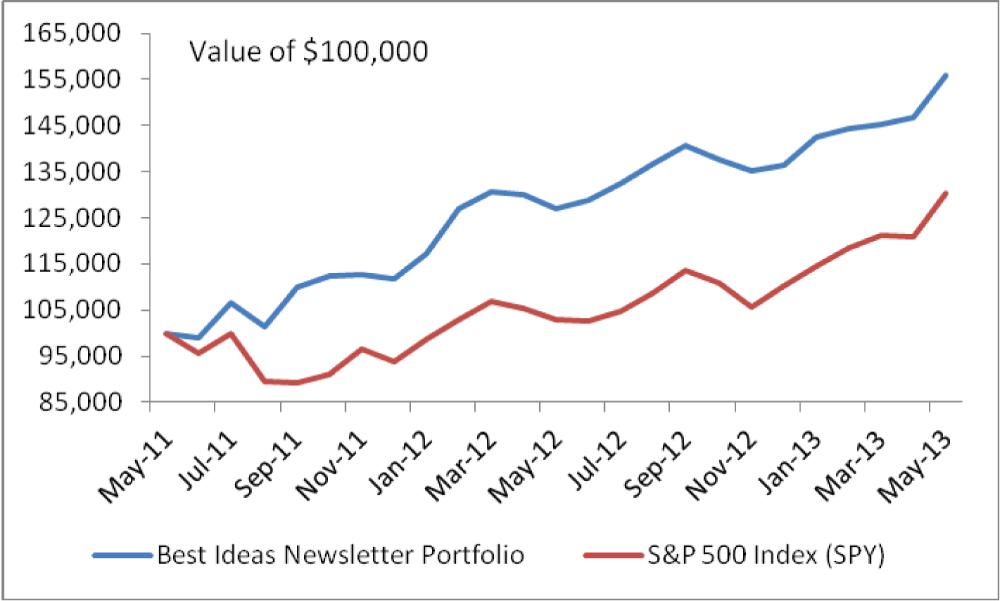

The efficacy and usefulness of any investment strategy are the returns it produces in the real world. Figure 2 shows the results that were achieved with a model portfolio constructed by Nelson. The cumulative return for the model portfolio from May 2011 to May 2013 was 55.9% versus 30.2% for the exchange-traded fund S&P 500 Index ![]() (SPY). Valuentum’s stock strategy outperformed the S&P 500 Index

(SPY). Valuentum’s stock strategy outperformed the S&P 500 Index ![]() (SPY) by close to 26 percentage points during this 24-month period.

(SPY) by close to 26 percentage points during this 24-month period.

Conclusion

The research studies by Asness and others provide evidence that combining value and momentum strategies offer investors the opportunity to achieve higher rates of return with lower risk than would be achieved with either strategy individually. Nelson’s research adds to these studies by highlighting the fact that the results of combining value and momentum strategies are very likely driven by focusing on a subset or cohort of stocks that possess good value and good momentum characteristics. Nelson believes individual investors can profit from this research by focusing on such stocks.

Currently it does not appear that the strategy of combining good value and good momentum has gained enough popularity to reduce its benefits. (Too much focus on any single anomaly tends to reduce or eliminate the excess returns.) One reason why is that value investors have been conditioned to ignore technical/momentum analysis, while many chartists do not pay significant attention, if any, to valuation multiples. Until combining value and momentum becomes more widely used, it is possible that combining low valuation and upward price momentum will be a useful strategy for individual investors.

Key Characteristics for Finding Good Value and Momentum

- Price-earnings ratio below the industry or sector median

- Price-earnings-to-growth (PEG) ratio below 1.0 and below the industry median

- EV/EBITDA* ratio below or equal to 10.0

- Increasing relative strength over past 52 weeks, 26 weeks, 13 weeks and 4 weeks

- The shorter-term moving averages (5-day, 20-day, or 50-day) are above the longer-term 200-day moving average

- The current price is at least 75% of the stock’s 52-week high

*EV/EBITDA is enterprise value (total market capitalization plus total debt) divided by earnings before interest, taxes, depreciation and amortization.

Related

Value Investing

Fernando Robles from FL posted over 13 years ago:

Jon Silverberg from NY posted over 13 years ago:

Terrence Kulasa from AB posted over 13 years ago:

Frank Klamik from WI posted over 13 years ago:

Gerald Scott from MI posted over 13 years ago:

Jean from AAII posted over 13 years ago:

Lee Martin from CA posted over 12 years ago:

Joost Tanis from IL posted over 12 years ago:

Wayne Thorp from IL posted over 10 years ago:

VAIDY B from CAN posted over 5 years ago:

VAIDY B from CAN posted over 5 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account