Related

Financial Planning

Magic numbers are used in shortcuts that help you calculate portfolio growth, how long your savings will last and how much you can withdraw.

Individuals planning for or approaching retirement commonly have questions about how long their savings will last, how much money they will be able to withdraw or how long it will take to save a certain amount.

In all these situations, the stream of money being withdrawn from savings is an annuity. In any final analysis, exact annuity formulas must be used to determine exact values. The appropriate formulas for answering questions about “how long” and “how much” require the use of logarithms. However, in a preliminary analysis or for long-range planning, reasonable approximations may be sufficient, because the future is not a certainty. The “magic numbers” 72, 114 and 167 may be used to obtain these approximations with simple arithmetic.

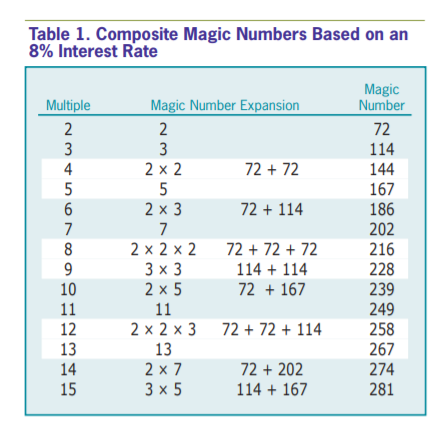

You may already be familiar with the Rule of 72, where the approximate number of years it takes for money to double is given by dividing 72 by the interest rate. Derived in the same manner are other, less-known rules: 114 divided by the interest rate for tripling money and 167 divided by the interest rate for quintupling money. With these three rules, magic numbers for multiples up to 15 are readily determined; they are displayed in Table 1. The “mavericks” are multiples of 7, 11 and 13, which are prime numbers and must stand alone.

These rules may also be used to determine the approximate number of years it will take to deplete savings based on the present value of a fund (e.g., retirement savings) or to determine the number of years it will take to accumulate a future amount (an accumulation), given specified annual withdrawals or savings, respectively. Further, given a specified numbers of years, you can determine what the approximate annual withdrawal or savings should be. All of these numbers can be determined using a simple hand-held calculator. If a fractional multiple is suggested, the average of the magic numbers of the two surrounding multiples may be used. Further, the magic numbers in Table 1 were derived using an 8% interest rate, or rate of return. For rates other than 8%, there is a 1% error for every 2% difference between the interest rate and 8%. However, the error in the magic numbers is less than 3.5% for interest rates between 2% and 15% and would have a negligible effect on approximations.

Determining the length and value of a level annuity (an annuity that pays out the same amount each year) depends on the amount invested (the present value), the number of years over which withdrawals can be made and the expected interest rate.

The most common question investors have is how long their retirement, or total, savings will last. Formula 1 determines this number in years.

Formula 1: n = M ÷ i

where,

n is the total number of years

M is the magic number

i is the interest rate multiplied by 100

As an example, let’s assume an investor has a $1 million fund that pays an 8% interest rate. The investor wants to withdraw $100,000 each year starting 12 months from now. How long will the $1 million fund last? We know the current value of the savings ($1 million), the withdrawal percentage (10%, or $100,000 ÷ $1 million) and the interest rate (8%). We just need to figure out which magic number to use. Fortunately, we have the information we need.

The first step is to determine which magic number multiple to use. You find the closest multiple by dividing the withdrawal percentage (10%) by the difference between it and the interest rate.

Formula 2: m = w% ÷ (w% – i%)

where,

m is the magic number multiple

w% is the withdrawal percentage

i% is the interest rate

Plugging in the numbers from our example, the math is 0.10 ÷ (0.10 – 0.08), which gives a multiple of 5.

Looking at the list of magic numbers in Table 1, we can see that magic number for a multiple of 5 is 167.

Returning to Formula 1, now that we know the magic number, we simply need to divide it by the interest rate in order to find out how many years the $1 million fund will last: 167 divided by (0.08 × 100), or 20.9 years. This should be thought of as 20 withdrawals of the same amount (a level withdrawal) and a 21st withdrawal of approximately 90% of the level amount. With a fund of $1 million, assuming an 8% interest rate, there can be 20 withdrawals of $100,000, with a 21st withdrawal of approximately $90,000.

When the time for withdrawals nears, the annuity provider or financial advisor might state what the duration of the annuity will be. This addresses the question of “how long will my savings last” if the withdrawals begin “now.” You could calculate the answer by simply multiplying the withdrawal rate (10%) by one plus the expected interest rate (8%). The math is 0.10 × (1 + 0.08) = 10.8%. You then use Formula 2 to find the closest multiple by dividing 10.8% by the difference between the withdrawal and interest rates: 0.108 ÷ (0.108 – 0.08) = 3.86. This value is sufficiently close to 4 to approximate the term using the magic number for 4 (144).

Now that we know the magic number, we divide it by the interest rate to get the number of years our savings will last: 144 ÷ (0.08 × 100) = 18 years. This should be thought of as 17 withdrawals of $100,000, beginning “now,” with a smaller 18th withdrawal. Had the multiple been closer to 3.5, the magic number could have been approximated by averaging the magic numbers of multiples 3 and 4.

Suppose you want your retirement fund of $1 million to last 30 years and you need to know “how much” you can withdraw annually beginning in one year if the expected interest rate is 6%. The first step is to determine the magic number by rearranging Formula 1 to become Formula 3.

Formula 3: M = n × i

where,

M is the magic number

n is the total number of years

i is the interest rate multiplied by 100

In this example the magic number is calculated by multiplying 30 by the expected interest rate of 6 (0.06 × 100) to get 180. Inspecting Table 1, we see that this value is close to the magic number 186, and therefore that a magic number multiple of 6 may be used to approximate the withdrawal amount.

We determine the initial withdrawal amount by multiplying the multiple by the interest rate and then dividing this by the multiple minus one. Formula 4 calculates the percent of the initial fund amount to be withdrawn.

Formula 4: w% = (m × i%) ÷ (m – 1)

where,

w% is the withdrawal percentage

m is the magic number multiple

i% is the interest rate

In our example, the math is (6 × 0.06) ÷ (6 – 1), which gives a multiplier of 7.2%. Therefore, beginning in one year, you could make 30 withdrawals of approximately $72,000 (7.2% of $1 million).

If you are at retirement age and will be withdrawing from your fund beginning “now,” the annual amount is approximated by dividing $72,000 by 1 plus the interest rate, or $72,000 ÷ (1 + 0.06), which results in $67,925.

Let’s reverse the process and ask, “how much will I need” to have saved in order to be able to withdraw $72,000 each year for 30 years if the expected interest rate is 6%? This question is essentially the opposite of asking “how much can I withdraw” given a set retirement savings, interest rate and number of years over which withdrawals will be made.

We know from our previous calculations (Formula 3) that, given a withdrawal period of 30 years and an interest rate of 6%, the magic number is near 186 and the magic number multiple near 6.

We need to determine the multiplying factor, which is calculated by simply subtracting one from the multiple and dividing it by the product of the multiple and the interest rate as a decimal. Formula 5 shows the process for determining the multiplying factor.

Formula 5: f = (m – 1) ÷ (m × i%)

where,

f is the multiplying factor

m is the magic number multiple

i% is the interest rate

In our example, the math is: (6 – 1) ÷ (6 × 0.06), which gives us a multiplying factor of 13.8889.

The estimated amount needed one year before the first withdrawal is the multiplying factor times the withdrawal amount, or 13.8889 × $72,000, which results in $1,000,000.

To determine the amount needed one year from “now,” simply increase the $1 million by the interest rate, to $1,060,000.

The opposite of depleting a retirement fund is the accumulation of savings and the determination of “how long” it will take to achieve a desired goal. Suppose you wish to accumulate $1 million for your retirement fund, you are able to invest $6,000 at the end of each year and you expect to be able to invest at an interest rate of 8%. The first step for this process is to determine the appropriate multiple from which a magic number can be obtained. Formula 6 shows this process.

Formula 6: m = (i + s) ÷ s

where,

m is the magic number multiple

i is the interest rate multiplied by 100

s is the savings rate multiplied by 100

The savings rate is simply obtained by dividing your annual contribution by your goal, or $6,000 ÷ $1 million = 0.6%. The magic number multiple is the sum of the interest rate (8%) and the savings rate (0.6%) divided by the savings rate: (8 + 0.6) ÷ 0.6 = 14.33.

Since the multiple of 14.33 is close to 14.5, we calculate the average of the magic numbers for 14 (274) and for 15 (281) at 277. Rearranging Formula 3, the number of years can then be determined by dividing the magic number by the interest rate times 100: 277 ÷ (0.08 × 100) = 34.6 years.

Say you don’t have 34 years until retirement: You only have 30 years to accumulate the $1 million fund. Say you also change your expected annual interest rate to 7%. What should your savings rate be? Formula 7 shows this process.

Formula 7: s% = i ÷ (m – 1)

where,

s% is the savings rate

i is the interest rate multiplied by 100

m is the magic number multiple

The first step is to use Formula 3 to determine a magic number by multiplying the number of years (30) by the interest rate times 100 (0.07 × 100), or 30 × 7. This gives the magic number 210. From Table 1 we see 210 would be close to the average of the magic numbers 202 (multiple of 7) and 216 (multiple of 8), or (202 + 216) ÷ 2 = 209. Our multiple would therefore be 7.5.

The savings rate will be the interest rate times 100 divided by the multiple minus one, or (0.07 × 100) ÷ (7.5 – 1). This gives a multiplier of 1.0769%. To accumulate $1 million in 30 years you would have to save approximately 1.0769% of $1 million each year. This amounts to $10,769 at the end of each year. The exact annual savings would be $10,586.41.

In an effort to maintain constant or non-diminishing lifestyles, retirement planning usually includes an estimated inflation factor for periodic withdrawals from retirement funds. Magic numbers may be used to determine the duration or initial annual withdrawal, so that the purchasing value of the withdrawals may remain constant with respect to inflation.

Suppose that, beginning in 12 months, you would like to withdraw $90,000 from that $1 million fund that is earning 8%, and to keep pace with inflation, you wish to increase that amount annually by 3%. You need to know “how long” the fund will last.

As in the example above, we need to determine which magic number is appropriate. The first step, however, is to determine an effective interest rate. This is accomplished by subtracting the growth rate from the interest rate, or 0.08 – 0.03, which gives an effective interest rate of 5%. The initial withdrawal rate is 9%, ($90,000 ÷ $1 million). We then find the magic number multiple by dividing the withdrawal rate by the difference between it and the effective interest rate, or 0.09 ÷ (0.09 – 0.05), which gives a multiple of 2.25 (Formula 2).

From Table 1 we see that the multiple of 2.25 is between the multiple of 2 and the average of the multiples of 2 and 3 (2.5). Because 2.25 is significantly closer to the multiple of 2 than it is to the multiple of 3, it may not be “safe” to use either of the two multiples or their average. Therefore, we should interpolate. The magic number to use will be the magic number for the multiple of 2 (72) plus the fraction of the multiple between 2 and 3 (0.25) times the difference between the magic number for the multiple of 3 (114) and the multiple of 2 (72), or 72 + [(0.25) × (114 – 72)] = 82.5. We then divide the magic number by the effective interest rate multiplied by 100, or 82.5 ÷ 5, which gives 16.5 years. This should be interpreted as 16 withdrawals of $90,000 and a 17th withdrawal of approximately $45,000.

Formulas 8, 9 and 10 show the process.

Formula 8: m = w% ÷ [w% – (i% – g%)]

where,

m is the magic number multiple

w% is the withdrawal rate

i% is the interest rate

g% is the growth rate

Formula 9: M = ML+ (m – ml) × (MH – ML)

where,

M is the magic number

m is the magic number multiple obtained from Formula 8

ml is the next lower multiple

MH is the next higher magic number

ML is the magic number for ml.

[The subscripts L and H refer to lower and higher magic numbers, respectively.]

Formula 10: n = M ÷ ( i – g)

where,

n is the total number of years

M is the magic number

i is the interest rate multiplied by 100

g is the growth rate multiplied by 100

There is a condition on the use of Formulas 8 and 10: The interest rate must be greater than the growth rate. If otherwise, a negative magic number would be necessary to have a positive number of years, which is not realistic. If the interest rate and growth rate are equal, then it is necessary to use a different set of formulas, because the denominator in Formula 10 becomes zero, indicating an infinite number of years. The withdrawal rate, w%, must also be greater than the effective interest rate, (i% – g%), otherwise the denominator of Formula 8 becomes 0 or negative. Finally, because the magic numbers are derived using logarithms, the approximations for multiples less than 2 are less reasonable than those for multiples of at least 2. This is due to the fact that the curve of logarithms is rather steep for values between 0 and 1 and “flattens” for greater values.

Beginning with a $100,000 withdrawal the first year, your $1 million fund will last less than 15 years at an interest rate of 8% and a growth rate of 3%. Suppose you want it to last 25 years beginning 12 months from now. “How much” should the initial withdrawal amount be?

The first step for this is to determine the effective interest rate, which is 8% minus 3%, or 5%, as previously calculated. The magic number is the desired number of years times the effective interest rate multiplied by 100 (0.05 × 100), or 25 × 5, which gives a magic number of 125.

Inspecting Table 1, we see that the number 125 is between 114 and 144 and not close enough to either value to choose one of them. We can, however, interpolate a multiple using the spread. The difference between 125 and the lower magic number (114) is 11. The difference between the higher magic number (144) and the lower magic number (114) is 30. The interpolated multiple would be the multiple of the lower magic number (3) plus the ratio of 11 divided by 30. The math is 3 + (11 ÷ 30) = 3.37. Formulas 11 and 12 show the process.

Formula 11: M = n × (i – g)

where,

M is the magic number

n is the total number of years

i is the interest rate multiplied by 100

g is the growth rate multiplied by 100

Formula 12: m = mL + (M – ML) ÷ (MH – ML)

where,

m is the interpolated magic number multiple

mL is the lower magic number multiple

M is the magic number

ML is the lower magic number

MH is the higher magic number

[The subscripts L and H refer to lower and higher magic numbers, respectively.]

The initial withdrawal will be the multiple (3.37) times the effective interest rate (5%), divided by the multiple minus one, or (3.37 × 0.05) ÷ (3.37 – 1), which gives a multiplier of 7.11%. The initial withdrawal will be approximately 7.11% of $1 million, or $71,100. If you plan to begin “now,” simply divide $71,100 by one plus the interest rate (1.08) to get $65,833. Formula 13 shows the process.

Formula 13: w% = m × (i% – g%) ÷ (m – 1)

where,

w% is the withdrawal rate

m is the multiple

i% is the interest rate

g% is the growth rate

Suppose your plan for income in retirement is to begin with an initial amount of $75,000 and increase it by an expected inflation rate of 3% for 30 years. You expect to invest at an interest rate of at least 5%. You want to know how much you will need 12 months before the initial withdrawal in order to save accordingly.

As with level annuities, the first step is to determine the magic number using the effective interest rate (2%). This is the product of the number of years and the effective interest rate times 100, or 30 × (0.02 × 100), which gives a magic number of 60 (according to Formula 11). Again, we need to interpolate the multiple.

Since the number of years for a multiple of 1 is zero with a magic number of 0, Formula 12 would give 1 plus the ratio of 60 divided by 72, or 1 + (60 ÷ 72) = 1.8333. In order to determine “how much,” you will need a multiplying factor, which is the reciprocal of Formula 13. This arithmetic is the multiple minus one divided by the multiple times the effective interest rate, or (1.8333 – 1) ÷ (1.8333 × 0.02), which gives a multiplying factor of 22.7268. Formula 14 shows the process.

Formula 14: f = (m – 1) ÷ [m × (i% – g%)]

where,

f is the multiplying factor

m is the multiple

i% is the interest rate

g% is the growth rate

The estimated amount of funds you will need is the multiplying factor times the initial withdrawal, or 22.7268 × $75,000, which gives the estimated fund amount as $1,704,510. The estimated amount on the date of the initial withdrawal would be increased by the interest rate (5%) to $1,789,736.

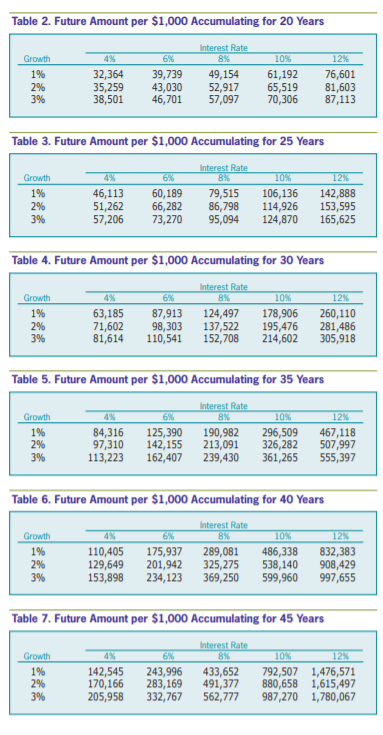

The formula for determining the future amount of geometrically increasing annuities requires the future amount of the interest rate compounded annually for n years minus the compounded amount of the growth rate compounded for the same n years. Unfortunately, there are no algebraic techniques to isolate this difference in order to use the rules of 72, 114 and 167. Simplification to determine the approximate number of years or the initial amount to be invested is not possible. For this reason, Tables 2 through 7 are included to show the actual future amounts per $1,000 of savings made at the end of year 1 and increased each year thereafter for the respective numbers of years.

Tables 2 through 7 may be used to determine an initial required savings to achieve a “needed” future amount. Suppose your time horizon is 30 years to accumulate $1 million. You expect to be invested at an interest rate of 6% and expect your annual savings rate to increase by 3%. We look in Table 4 (30 years) at the intersection of the 3% growth rate and 6% interest rate and find the value of $110,541. We then divide the “needed” amount ($1 million) by $110,541 and get 9.04642. To determine the initial annual savings, we move the decimal point three places to the right (by multiplying by 1,000) and get $9,046.42.

The final withdrawal from a present value and the final savings for a future amount may be approximated using the magic numbers.

You have determined that beginning in 12 months you can withdraw approximately $72,624 the first year and increase the annual amount by 3% if the fund maintains an interest rate of 8if the fund maintains an effective interest rate of 5%, for 30 years. This means that you would adjust the withdrawal rate to “accommodate” the interest rate. You wonder what the 30th withdrawal will be.

You can determine this figure by modifying Formula 3, using the growth rate instead of the interest rate to determine the magic number. Formula 15 shows this process.

Formula 15: M = (n – 1) × g

where,

M is the magic number

n is the total number of years

g is the growth rate multiplied by 100

We subtract one from the number of years and multiply the result by the growth rate times 100, or (30 – 1) × (0.03 × 100) which gives us 87 for the magic number. Because 87 is reasonably close to 72, we may use a multiple of 2. The approximate final withdrawal will be this multiple times the initial withdrawal or 2 × $72,624 = $145,248.

An initial dollar amount is not necessary to determine the final withdrawal if a percent of the present value of a fund or a current salary is known.

Suppose you and your employer contribute a combined 9% of your salary to a retirement fund over a 45-year working career. You expect your salary to increase by 3% each year. Formula 15 gives the magic number as (45 – 1) × (0.03 × 100), or 132. This value may not be sufficiently close to the magic number 144 to use a multiple of 4. We could make use of Formula 12 to find a closer approximation. Since 132 is between the magic number 114 (multiple of 3) and 144 (multiple of 4), the approximate multiple will be 3 + [(132 – 114) ÷ (144 – 114)]. This gives us a multiple of 3.6. The final-year salary and contribution will be approximately 3.6 times your initial-year salary and contribution. For example, suppose your initial salary is $40,000. Your final salary would be approximately $144,000 (3.6 × $40,000). The initial contribution would be 9% of $40,000, which is $3,600, and the 45th contribution would be approximately $12,960 (3.6 × $3,600). You expect the fund to be invested at 8%. We can determine the final accumulation by using Table 7 (45 years). We simply replace the comma by a decimal point in the value at the intersection of the 8% interest rate and the 3% growth rate and multiply by the initial contribution, or 562.777 × $3,600. This multiplication gives an accumulation of $2,025,997 (and we can answer the questions “how long will it last?” or “how much can I withdraw?” using the aforementioned formulas).

With these formulas and tables, a simple calculator is all that is needed to estimate how long your money will last, how much will be needed for a desired retirement income, how much you can withdraw for a desired number of years, or how much you must invest each year to achieve a financial goal.

As stated, any formal analysis will require precise formulas, but for preliminary work, the magic numbers provide a convenient way to “get into the ballpark.” If you are told X and you know the “ballpark” should be Y, you will be prepared to respond. Remember that it is your money that is being discussed.

In addition, manipulating the magic numbers serves as a mental exercise and might remove our total dependence on sophisticated devices.

For more detailed math on magic numbers and their use in annuities, a PDF file is available here.

Financial Planning

Portfolio Strategies

Portfolio Strategies

Walter from CA posted over 14 years ago:

Makhtar from NJ posted over 14 years ago:

Lawrence from MD posted over 14 years ago:

Peter from UT posted over 14 years ago:

John c from IL posted over 14 years ago:

W from PA posted over 14 years ago:

George from OK posted over 14 years ago:

Charles from IL posted over 14 years ago:

Dan from NC posted over 14 years ago:

Allen from PA posted over 14 years ago:

Robert Reichert from AZ posted over 11 years ago:

Robert Reichert from AZ posted over 11 years ago:

Robert Reichert from AZ posted over 11 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account