Anxious investors looking to preserve wealth and pick up yield have increasingly focused on fixed income. But it’s been a tough few years for yield-oriented investors—interest rates are low and the world is awash in liquidity.

As a total return–oriented portfolio manager, I’m constantly on the lookout for income vehicles that can augment our holdings in low-yielding common stocks. One solution: preferred stocks.

How They Work

Preferred stocks (“preferreds”) have been around for over a century. They represent a slice of a company’s capital structure that is senior to the common shares, but subordinate to the debt (both secured and unsecured).

As with common stock, dividends aren’t guaranteed and must be declared by the board of directors, usually on a quarterly basis. The dividend is usually a specific dollar amount per share or a percentage of par/stated value. (Par/stated values normally range between $25 and $50 per share.)

Unlike bonds, preferreds usually have no maturity date for when the principal is repaid. However, most can be called or redeemed by the issuer at a specific date and price.

Advantages

- Preferred status: Dividends must be paid on the preferred stock before they can be paid on the common stock. In a sale, liquidation or bankruptcy reorganization, the interests of the preferred holders usually come ahead of those of the common stock holders, but behind the debt holders.

- Liquidity: Most preferreds trade on the NYSE or NASDAQ in round lots of 100 shares, making them easier to purchase than bonds, which trade in lots of $5,000 to 10,000.

- Tax advantages: Currently, preferred dividends are taxed at an appealing 15%, but that rate—part of the Bush tax reduction—is set to expire on December 31, 2010. In 2011, dividends of all types will be taxed as ordinary income if Congress does not act.

- Accumulation: Most, but not all, preferreds are cumulative, meaning if a full dividend is not paid each quarter, it accumulates indefinitely until paid. No common stock dividends can be paid until preferred dividends in arrears are paid. Holders of a cumulative preferred may not receive dividends for a quarter or even years. Then, should the firm’s fortunes improve, the cumulative dividends will be paid. Some investors buy “broken” preferreds. These securities pay no dividends, but trade at big discounts to par/stated value; investors will hold them until the arrearage is cured (not a certainty). The shares normally rebound once dividend payments resume.

Disadvantages

- Minimal voting rights: Preferred owners can rarely elect directors. However, if the firm wants to issue senior securities, merge, or fundamentally alter the firm’s financial structure, the preferred owners usually have the right to vote on these matters.

- Callability: Almost all preferreds are callable at par/stated value at the issuer’s option, normally at a specified price after a specified time from issue date (usually five years). In the declining interest rate environment of recent years, many preferreds have been called, leaving holders with the challenge of replacing a high-dividend income stream. Companies are constantly looking to lower their cost of capital, and refinancing a high-cost preferred is one of the most logical ways to do this.

- Interest rate risk: Like most fixed-income vehicles, existing preferreds will rise in price if interest rates fall and decline in price if interest rates rise. (The preferred’s vulnerability to a change in interest rates is similar to a bond with a longer maturity.) While there appears to be minimal evidence that rates are about to rise sharply, preferred owners should realize that risks increase as yields rise. Investors are best off buying preferreds in a stable or declining interest rate environment and avoiding them if rates are about to rise.

- Credit risk: Deterioration in a company’s fundamentals could inhibit the ability to make preferred dividend payments. An issuer will eliminate a preferred dividend before it will default on its debt. Many preferreds are rated by Moody’s and/or Standard & Poor’s and investors should stick with preferreds that are rated investment grade (Baa/BBB) or better. A ratings downgrade is a sign that trouble may be brewing. To see how deteriorating fundamentals can hurt a preferred issue, take a look at the recent action in the preferred issues of Freddie Mac, Fannie Mae and others. Losses were huge, as investors questioned their ultimate viability.

The Preferred Line-Up

Now that you know the preferred basics, let’s talk more about the types of preferreds:

- Straight preferreds;

- Trust preferreds; and

- Convertible preferreds.

Straight Preferreds

These are your plain-vanilla issues, which pay a fixed dividend on par/stated value.

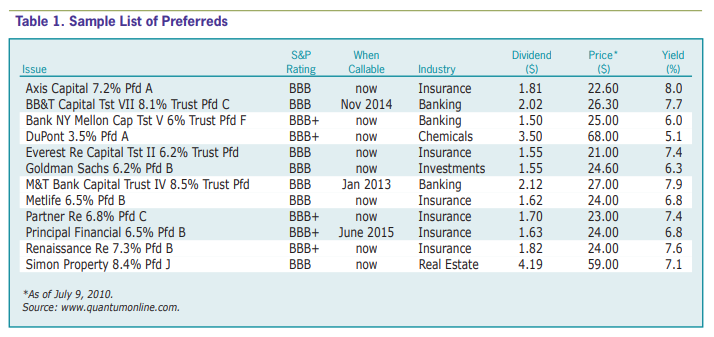

Take a look at the issues in Table 1. Most of these are straight or trust preferreds taken from the www.quantumonline.com database. All are rated BBB or better and most are now callable. Issues that are currently callable typically trade at or below the call price. As noted above, you don’t want to pay a premium to the call price today only to have the issue called at a lower price tomorrow. The average yield is 7%, well above what most bank CDs and money funds are paying. The higher return is indicative of higher risk including the credit and interest rate risk mentioned above.

Trust Preferreds

These preferreds are backed by a bond issue held in trust and they provide the increased safety of bonds with the liquidity of stocks. The bond interest flows to the preferred holder, making them tax deductible to the issuer but fully taxable to the preferred holder.

Trust preferreds come in two flavors: those created by the company issuing the bonds, and those created by a broker-dealer using bonds it buys from the issuer for that purpose.

Company-issued trust preferreds are usually a bit riskier. They often have a provision allowing dividends to be suspended for up to five years under certain conditions.

Broker-created trusts (known as third-party trusts) don’t have this risk and are usually rated higher than company-issued trusts.

Major issuers of trust preferreds include many utility, industrial, financial and communications firms. Denominations are usually $25 to $100 and redemption provisions can be tricky, so step carefully.

One advantage of this particular type is that, upon liquidation, a trust preferred’s debentures generally rank as junior debt, ahead of a company’s traditional preferred or common shares.

Convertible Preferreds

These provide the owner with the right to exchange a share of preferred stock for a share (or shares) of common stock in the same company based on a predetermined conversion or exchange ratio, which won’t change. Upon conversion, the owner has the rewards and risks of a common shareholder. (I am excluding discussion of mandatory convertible securities, which are complicated with many special provisions and are most suitable for professional investors.)

Generally, the yield on a convertible preferred exceeds the common stock yield.

Because of the dividend, the convertible preferred will usually decline less if the common stock declines, providing a cushion on the downside. If the common stock rises, the convertible will also rise because of the conversion feature.

The convertible preferred provides the best of both worlds—downside protection and upside potential. To the issuer, a convertible offers the chance to raise cash without giving away equity too cheaply, or paying a high interest rate on a bond.

The decision metrics on a convertible preferred are fairly straightforward. Assuming you like the company on a fundamental basis, some key elements include:

Conversion value:

conversion ratio × conversion price

Conversion premium:

convertible market price – conversion value

Yield pickup:

convertible dividend – (common dividend × conversion ratio)

Breakeven time:

conversion premium ÷ yield pickup

For example, say the convertible preferred of Company X ($25 par) is trading at $33 and pays a $2.50 per share dividend for yield of 7.6%. The conversion ratio is 6.2—meaning each preferred share is convertible into 6.2 shares of common. The common stock trades at $4.80 per share and does not yield a dividend. Assuming you like the company’s fundamentals and the convertible shares aren’t callable for several years, should you buy the convertible or the common stock? Here is the math:

Conversion value:

= 6.2 shares × $4.80

= $29.80

Conversion premium:

= $33.00 – $29.80

= $3.20

Yield pickup:

= $2.50 – (0 × 6.2)

= $2.50

Breakeven time:

= $3.20 ÷ $2.50

= 1.28 years

Generally, a breakeven time less than two years is very good. In the above example, a breakeven time of 1.28 years means that the premium paid for the conversion feature is recouped in a little over one year. (In other words, an investor is compensated for the premium cost of the preferred via the payment of dividends.) Once the breakeven point is passed, the investor has “paid for” the conversion feature in full and now earns the higher yield as long as he owns the convertible. Longer breakevens mean slower paybacks and a less attractive investment.

Should the investor at some point wish to “convert” his preferred shares to common, unless the conversion premium is small, it’s better to sell the convertible and use the proceeds to buy the common. This is because the conversion premium is valuable and exercising the conversion feature directly eliminates the opportunity to monetize that premium. (The idea is that it is more profitable to take advantage of the spread between the preferred and the common than to exercise the conversion feature of preferred stock.)

Evaluating Preferreds

Since a preferred holder lacks the enforceable claim to interest and principal at maturity that is enjoyed by a bondholder, and the right to participate in residual profits enjoyed by the common stock holder (except for convertible holders), sound analysis is essential. The investor must demand an extra margin of safety because of the discretionary nature of the dividend payment. Indeed, a generally profitable firm that incurs temporary losses is likely to suspend preferred payments, even though its cumulative profitability is more than adequate to make the payments.

For that reason, for a proper evaluation you need to focus on the following questions.

Do You Like the Company’s Fundamentals?

The focus here should be on the company’s profitability, growth prospects, financial strength and management depth. Profitability allows dividend payments after any interest payments are made, so accurate analysis is critical. Size and competitive position are equally important as contributors to earnings consistency. The nature of the industry is also important—growth and consumer products industries generally have better long-term prospects than cyclical or declining industries.

What’s the Capital Structure?

Preferreds with no bonds, notes or bank debt in front of them in the capital structure usually do better than those with any type of debt (which is paid ahead of the preferred).

Sometimes a company will have multiple classes of preferred shares outstanding, so make sure you know which ones are the senior securities. Even if an issuer has no debt, or other preferreds senior to your preferred, it may have the right to issue new securities (convertible or straight) that would be senior to yours. The only way to find out and protect yourself is to read the prospectus!

What’s the Call Risk?

As mentioned above, almost all preferreds may be called at a certain price (usually par/stated value) after a certain date. Make sure you don’t pay a premium to par, only to have the issue called away shortly at par. Generally, an issue approaching a call date will trade close to its call price. Sometimes a preferred will trade at a premium to call price up to and beyond its call date. This indicates investors are betting the issue won’t be called, usually because the company lacks the cash to do it.

A convertible preferred may trade at a significant premium to the call price because of the value of the conversion feature. For example, if the Company X common mentioned above was trading at $12 per share instead of $4.80, the conversion value of the convertible preferred would be $74.40 (6.2 × $12). Thus, the price of the convertible preferred would be driven by its conversion feature rather than its dividend.

Indeed, many issuers “force” the conversion of a preferred to common by calling the preferred at par or stated value. Continuing with the above example, if Company X called the convertible at par value of $25 a share while the market price is $33, my guess is they wouldn’t have many takers. Convertible holders would either convert to common or sell their convertible shares to someone who would. In either case, the issuer succeeds in replacing a high-cost preferred with low-cost common shares.

Is the Yield in Line With the Risk?

The old saying “there’s no free lunch” applies to preferred investing. If a yield appears too good to be true, it probably is.

Preferreds that have exceptionally high yields normally have them for a reason. Investors doubt the yield is sustainable because of fundamental issues and have priced the security accordingly, usually to reflect a looming dividend cut or declining credit quality.

Is There a Sinking Fund?

The presence of a sinking fund provides an extra measure of protection to a preferred holder by requiring the issuer to set aside cash (usually a percentage of consolidated income) for the express purpose of paying the dividend.

Again, such important details are normally buried in the prospectus.

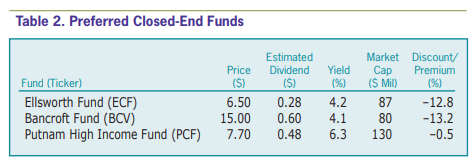

Preferred Closed-End Funds

Investors who don’t want the responsibility of building and maintaining a portfolio of individual preferreds might want to look at closed-end funds. There are both straight and convertible closed-end funds that offer the benefits of diversification, professional management and economies of scale.

Many also trade at less than underlying net asset value, providing the opportunity to buy a dollar’s worth of assets at a discount.

[For more information on closed-end funds please see “Rodney Dangerfield Investing: Closed-End Fund Opportunities” by John Deysher in the April 2007 AAII Journal, available at AAII.com.]

Table 2 notes some reasonable closed-end fund offerings.

Conclusion

Preferred stocks occupy a unique position in a firm’s capital structure and can provide attractive dividends and important tax advantages.

Convertible preferreds offer the upside of the underlying common and the downside protection inherent in the dividend.

Buying high-quality, highly rated preferreds at steep discounts to par/stated value during times of market turmoil can provide robust total returns.

There are numerous preferreds available, most of which trade on an exchange or NASDAQ (see www.quantumonline.com for a comprehensive listing). Another dedicated site is www.preferred-stock.com, but a portion is subscription based. Prospectuses may often be found on the EDGAR portion of www.sec.gov.

However, few preferreds are followed by Wall Street firms, and all are vulnerable to interest rate and credit risks.

Stringent analysis of operating fundamentals, coverage ratios and balance sheet strength is essential, as are patience and a long-term outlook.

Happy hunting.

Mike from CA posted over 15 years ago:

Antal from FL posted over 15 years ago:

Robert from WA posted over 15 years ago:

Gary from PA posted over 14 years ago:

Walter from PA posted over 14 years ago:

Larry from CA posted over 14 years ago:

Sanford from OH posted over 14 years ago:

Robert from WI posted over 14 years ago:

Robert from IL posted over 14 years ago:

Donald from MI posted over 14 years ago:

Maryanne from SC posted over 14 years ago:

Wayne from OR posted over 14 years ago:

Ed from NY posted over 14 years ago:

George from CO posted over 14 years ago:

Ron from TX posted over 14 years ago:

James from IL posted over 14 years ago:

Richard Jochem from WI posted over 13 years ago:

Everett B. Guthrie from CA posted over 13 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account