Related

Portfolio Strategies

Stocks are good hedges against inflation, preserve purchasing power and, over long periods, are less risky than bonds.

by Jeremy Siegel | August 2014

Jeremy Siegel is a professor at the University of Pennsylvania, the senior investment strategy advisor to WisdomTree Investments and the author of the best-selling book, “Stocks for the Long Run” (fifth edition, McGraw-Hill, 2014). He and I spoke in late May about the importance of maintaining a significant allocation to stocks.

—Charles Rotblut

Charles Rotblut (CR): You have a reputation for being bullish on the stock market, but from reading “Stocks for the Long Run,” it sounds like you’re more focused on the ability of stocks to prevent the loss of purchasing power than making a call on the direction of the market. Is that correct?

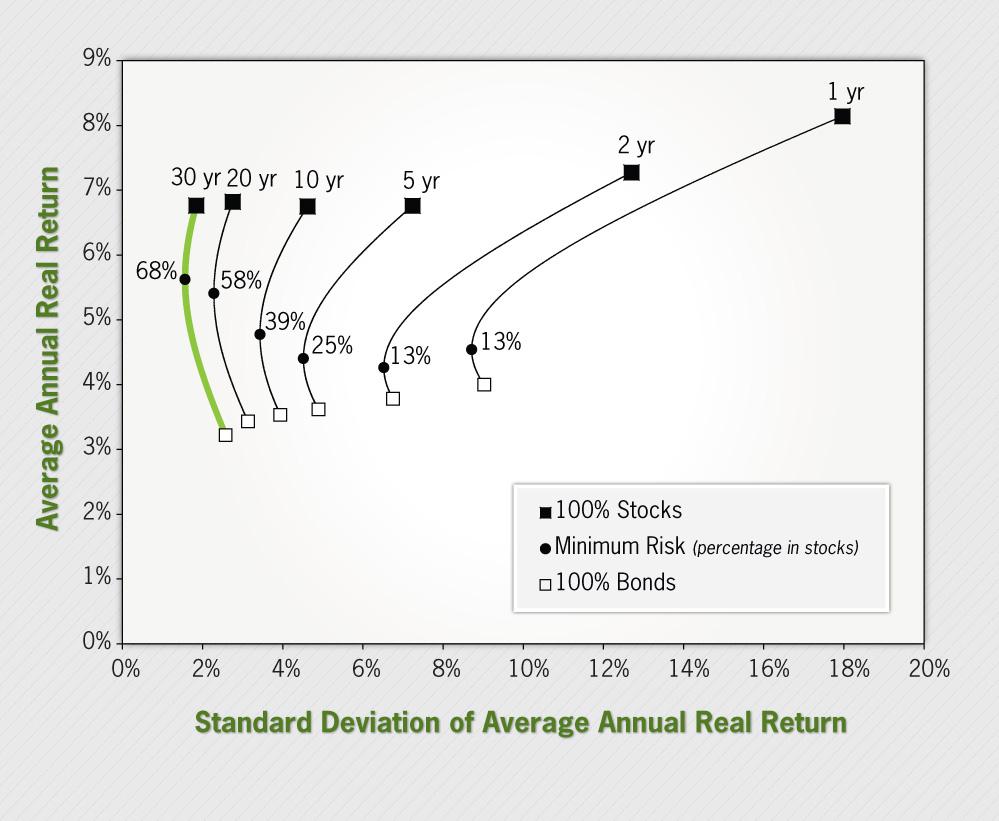

Jeremy Siegel (JS): My book emphasizes that the long-run return on stocks is between 6.5% and 7% per year after inflation (Figure 1). This return has been very stable in the long run. Over time stocks are good hedges against inflation, so they keep up with inflation and purchasing power, but even aside from that their returns are excellent compared to fixed-income assets. They dominate fixed-income assets, and particularly in today’s low interest rate environment I think the margin by which stocks will outperform bonds is even greater than it historically has been.

CR: Do you have any concerns? There’s obviously some doomsayers who believe historical returns won’t be repeated in the future.

JS: I don’t know why they say that. Stocks are selling very near their historical price-earnings ratios of 15 to 16, and from those price-earnings ratios you can expect to get 6+% real returns. If you’re at a price-earnings ratio of 30, like we were in 2000, then you can’t get those returns in the long run. But if you’re at or near the historical valuation, as I believe we are today, there’s very little chance in my opinion that stocks will not generate an excellent long-run return. Furthermore, with yields so low and likely to stay low, relative to historical experience, we might even see further expansion in price-earnings ratios, which might give an even greater boost to stocks in the short run.

CR: You wrote that the equity premium—the difference between what you earn on stocks and what you can earn on bonds— is higher than it should be because of what the Federal Reserve is doing in terms of quantitative easing [bond buying]. Is that correct?

JS: Yes, it’s higher than it should be because the yield on bonds is so low. But it is important to realize that there are many fundamental factors besides Fed policy that are pushing bond rates down. The historical margin by which stocks beat bonds is about 3% to 3.5% a year, but at current valuations, the margin is about 6% for stocks over bonds.

CR: Regarding market indicators, I know that obviously there are some popular ones, such as Robert Shiller’s CAPE ratio [cyclically adjusted price-earnings ratio]. Is there a certain ratio you use to judge the attractiveness of the stock market? You just mentioned a price-earnings ratio of 30, where people might want to be more cautious about stocks or where they might want to think about doing something with their allocations.

JS: I’ve written a paper on the Shiller CAPE ratio that’s been presented at professional organizations, and I show that it has been giving false alarms over the past several years, principally because the earnings being calculated and put into the model now are very different than where they were in earlier years. When I adjust for these factors, I find very little, if any, overvaluation in the market on the basis of the CAPE ratio calculations.

CR: Regarding allocation, you make the argument that stocks are actually less risky than bonds, and that’s primarily a return and a purchasing-power argument.

JS: Yes. That’s for holding periods of 20 years or more. After inflation, stocks are less risky than government bonds for holding periods of two decades or more.

CR: A lot of our members are retirees who have often been told “increase your bond allocation as you get older.” So how does someone find a good balance between stocks and bonds?

JS: I can understand that, because as you get older, more of your income comes from your savings and less from your work. Many move toward bonds, but I think people move too much toward bonds.

At today’s life expectancies, many people are living 25 to 30 years or longer after retirement. It’s over those longer periods that stocks definitively perform better and with less risk than bonds.

So, you shouldn’t suddenly convert everything to bonds once you’re 65 years old, particularly if you’re in good health, because you will have to take advantage of those higher returns on stocks in order to continue your lifestyle.

CR: Any guidelines on how someone should try to set the allocation mix or where they should consider trying to strike a balance between stocks and bonds?

JS: No, I think it’s very difficult, because it depends on what sources of income retirees have—for example, their Social Security, annuity or other payments. The question of whether they wish to leave a bequest or not is also very important. So I don’t think one number fits all. I just want people to realize that, again, we are living longer than ever before and they should not become too conservative with their stock/bond allocation as soon as they retire (Figure 2).

CR: What about from a behavioral standpoint, particularly with the price volatility of the market? Any suggestions for how individual investors should cope with the price fluctuations?

JS: Well, they shouldn’t try to trade to beat the market. I try to view those short-term dips as opportunities to get into the market if I’m not fully invested, but again, the average investor has to train himself or herself to ignore the fluctuations and focus on the long-term returns.

CR: Any tips besides just to avoid trading? Do you advocate bucket strategies or some type of rebalancing?

JS: Well, at WisdomTree, we have index portfolios that rebalance according to dividends and earnings, so I do think that it isn’t a bad idea to sometimes sell those stocks at the higher price-earnings ratios and buy those at the lower ratios.

Of course, low-cost index funds are the way to go. I believe in “fundamentally weighted indexing,” which rebalances a portfolio based on fundamentals; historically, this has done better than capitalization-weighted indexation. But even a cap-weighted index portfolio will serve many investors well in the future.

CR: Since you brought up WisdomTree, I know they have a dividend exchange-traded fund (ETF), which I believe you did some research on. Could you just comment on the role that dividends have played in stock returns?

JS: Dividends are an important component of stock returns. Those stocks that pay higher dividends have, over the last half-century, given investors higher returns with lower risk than the low- and non-dividend-paying stocks. We’ve examined the record completely over very long-term periods, particularly an analysis of the entire S&P 500 index, which was created in 1957. We find that in the long run dividend-paying stocks give investors a much better risk/return trade-off.

CR: Did you notice the same difference between just high yield and a yield with dividend growth?

JS: Well, WisdomTree focuses on dividend-paying stocks; we don’t try to forecast dividend growth. We do have a suite of products that are geared toward the growth of dividends, but forecasting is not necessary for superior returns.

CR: Going back to the subject of allocation: As you know, correlations between different global stock markets rose after the last bear market, and they seem like they have stayed somewhat high. Do you think this signals that we’re still in part of what is just a normal cycle? Or do you think that something’s changed because of the macroeconomic picture, and we’re going to see correlations perhaps stay at higher levels than in the past?

JS: Well, there are several reasons why global correlations have gone up. First of all, we had a synchronized global recession and business cycle to the greatest degree that we’ve ever had since the 1930s. Everyone was seeing the same types of stresses, and as a result stock markets moved together.

Secondly, information is instantly communicated across markets, so investor sentiment is transmitted between markets. As a result, especially in the short run, you’ll see more correlation in world stock markets. In the long run, though, I still think that you gain significant diversification benefits by international investing. I am an enthusiastic international investor.

CR: Do you see any difference between developed countries and some of the emerging markets?

JS: They are both worthwhile. I think emerging markets, which have taken quite a beating as of the last six months, are very good buys now. I’m not going to pick individual countries, but I think as a group they are very attractive.

I think Japan still has a way to go, I think the Japanese government of Shinzo Abe still wants to stimulate the economy and raise stock prices.

Europe has recovered dramatically; the only thing I worry about in Europe is perhaps a fall in the euro. European stocks, which used to be selling at a 20% to 30% discount to American valuations, are now selling at only a 10% discount.

CR: In the U.S., what about striking a balance between, say, large cap and small cap? Do you think investors should try to get both, or just go for a broad market index?

JS: I like broad indexes. Large-cap stocks are about 80% of the total market, and small- and mid-cap stocks are about 20% to 25%. If you keep that proportion, I think that that’s fine. I do not think it’s worth trying to time when small stocks are going to do better or worse. Clearly those people who are successful at that will get better returns, but I think it’s very hard to do.

CR: In regard to Treasuries and gold, you said those are the two assets that are probably the least correlated with stocks, correct?

JS: Yes, unless we get into an inflationary environment. If we do, then Treasuries will be more highly correlated with stocks.

Gold doesn’t seem to be much correlated with stocks, but there’s no return from gold outside of price appreciation, if any. There’s no earnings and there’s no dividend with gold. I really do not find gold to be an attractive asset even though it’s come down rather dramatically in the last 12 months.

I still don’t think bonds are a good asset, even though I don’t think interest rates are going to go as high as I once feared. But I do think interest rates will work their way higher, and at today’s yields that does not make long-term Treasury bonds a good investment.

CR: And what about some of the less directly correlated assets such as real estate investment trusts (REITs) and master limited partnerships (MLPs)? Have you done any research on their returns?

JS: Not a lot. I do like cash returns, and many of those assets have cash returns. If you’re not buying them at too high of a price, they can be rewarding. Some of them are not as liquid, obviously, as other stocks. Certainly I’m not objecting to those that want a little bit more yield, but I suggest that you could go to the dividend-yielding sectors of just the equity market and pick up yields that are comparable to some of these alternative assets. So although I don’t dislike those assets by any means, I do think you can get yield that’s just as good in the stock market.

CR: Regarding your preference for broad index funds, is it mostly a cost issue for you, or do you view the market as being somewhat efficient or following a random walk?

JS: You want the lowest cost, because those costs just keep on eating away at your return and index funds generally have the lowest cost. So I’m very attracted to them. For those people with a 20- to 30-year horizon, costs are going to mean a big difference.

It has been shown that active managers are not able to outperform sufficiently to offset the costs that they impose on investors, and that seems to be a negative for those funds.

CR: Finally, you talk in your book about using the 200-day moving average as a tool to determine when to get in and out of stocks. Could you comment on that?

JS: The 200-day moving average strategy has, over time, allowed you to get out of major bear markets. There are other times, though, when you are whipsawed back and forth going in and out of the market, and this is very costly. This is particularly true in markets with no trend. Over the long run, you don’t get as high of a return as buy-and-hold investors get, but you do get a reduction in volatility and do miss many bear markets, which many investors regard important enough to sacrifice some return for.

Portfolio Strategies

Growth Investing

John Croy from RI posted over 12 years ago:

Jerry McC from TX posted over 12 years ago:

James Strite from PA posted over 11 years ago:

Sanford Levey from MA posted over 11 years ago:

John Lalley from FL posted over 11 years ago:

Charles Rotblut from IL posted over 11 years ago:

Vaidy Bala from AB posted over 11 years ago:

Joe Alotta from IL posted over 11 years ago:

Edward Mueller from IL posted over 11 years ago:

Charles Rotblut from IL posted over 11 years ago:

Pat from KY posted over 11 years ago:

Charles Rotblut from IL posted over 11 years ago:

Rick Grant from GA posted over 11 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account