Related

Portfolio Strategies

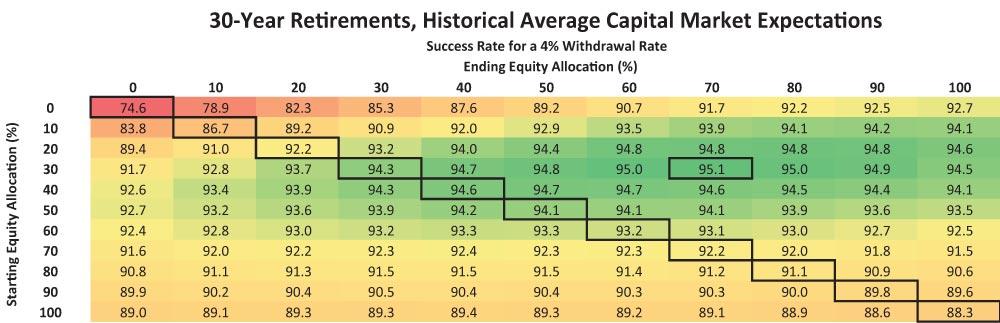

Starting retirement with a 30% allocation to equities and then gradually increasing it to 70% leads to a 95.1% probability of not outliving your savings.

For the past 20 years—due to the growing research on safe withdrawal rates, the adoption of Monte Carlo analysis (a method of considering many simulations), and just a difficult period of market returns—there has been an increasing awareness of the importance and impact of market volatility on a retiree’s portfolio.

Dubbed “sequence of return” risk, retirees are cautioned that they must either spend conservatively, buy guarantees (e.g., annuities), or otherwise manage their investments to help mitigate the danger of a sharp downturn in the early years.

One popular way to manage the concern of sequence risk is through so-called “bucket strategies” that break parts of the portfolio into pools of money to handle specific goals or time horizons. For instance, a pool of cash might cover spending for the next three years, an account full of bonds could handle the subsequent five-to-seven years, and equities would only be needed for spending more than a decade away. This “ensures” that no withdrawals will need to occur from the equity allocation if there is an early market decline.

Yet the reality is that strict implementation of such a cash/bonds/equities bucket liquidation strategy is more than just an exercise in mental accounting; it can actually distort the portfolio’s asset allocation and lead to an increasing amount of equity exposure over time. This occurs as fixed-income assets are spent down while equities continue to grow. Recent research shows that despite the contrary nature of the strategy—allowing equity exposure to increase during retirement when conventional wisdom suggests it should decline as a retiree ages—it turns out that a “rising equity glide path” (where the path of equity exposure ‘glides’ higher year after year) actually does improve retirement outcomes. If market returns are bad in the early years, a rising equity glide path ensures that retirees will dollar cost average into markets at cheaper and cheaper valuations. Conversely, if the markets are good, retirees won’t have a lot to worry about in retirement anyway (except, perhaps, how much excess money will be left over at the end of their life).

Of course, the challenge to utilizing a rising equity glide path strategy as a retiree is that many would obviously be concerned about having more equity exposure during their later retirement years. Yet the research shows rising glide paths can be so effective that exposure to stocks can start much lower to begin with—so low, in fact, that the strategy may actually lead to lower average equity exposure throughout retirement, even while obtaining more favorable outcomes. And ironically, it turns out that for those who do want to utilize a rising equity glide path, the best approach might actually be to implement it as a bucket strategy in the first place, where cash and bonds are spent down over time and equities are allowed to run (higher) for a period of years.

In the 1990s, William Bengen published his first research on safe withdrawal rates. He made the fundamental point that it doesn’t matter what a retiree’s average returns are to determine if their plan will be successful; instead, it’s necessary to look at the sequence in which those returns occur, as there are numerous historical scenarios where the long-term average may have been healthy, but the sequence meant retirees had to withdraw far less. After all, it doesn’t really matter if returns average out in the long run, if ongoing retirement withdrawals plus bad market returns early on mean there’s no money left when the good returns finally arrive.

Accordingly, the conclusion of the safe withdrawal rate research was that retirees should set their spending targets based not on average returns, but on the worst-case scenarios that have occurred in history1. Spending rates are presumed to be “safe” if they are low enough to survive all of those scenarios (whether due to below-average returns throughout retirement, or reasonable returns but an unfavorable sequence).

Of course, in practice, retirees often notice the importance of return sequencing the moment a bear market occurs as they’ve begun down the retirement path. They see their account balance fall precipitously and begin to worry—sometimes excessively so—about whether they need to adjust their spending or change their portfolio (or both). Accordingly, some retirees have adopted various forms of “bucket” strategies over the years, designed to help them get comfortable with their ongoing volatility. For instance, if there’s a “bucket” with three years of cash, retirees may worry less about a short-term market decline. If there’s a second pool of money with intermediate bonds for the subsequent few years, such that equities don’t have to be touched for eight to 10+ years in total, retirees may be further soothed. If the bulk of ongoing expenses can be covered from direct cash flow sources (e.g., Social Security payments, a pension, annuitized income, etc.), it may be even easier to tolerate the market volatility.

However, the reality is that many of these types of bucket liquidation strategies often are more than just an exercise in mental accounting acrobatics; having alternative fixed-income sources to tap in the early years can help, both mentally and financially, to mitigate the danger of sequence risk. After all, the mathematical reality is that if there are no cash flows (i.e., there are no necessary withdrawals) then return sequencing is no longer an issue. In other words, as long as the retiree truly doesn’t have to take any withdrawals from equities in the early years and can allow time for any early retirement bear markets to recover, the primary sequence risk of the portfolio/retirement scenario can be avoided.

While bucket approaches—from just holding cash reserves, to “time-segmenting” pools of money for use over time, to partially annuitizing to reduce income needs in the early years—can be effective at reducing sequence risk, the reality is that such strategies disproportionately spend from fixed-income assets and let equities grow. As a result, bucket approaches will end up, after a number of years, with “distorted” asset allocations: A shrinking fixed-income allocation and a rising percentage of equities. Of course, such outcomes can be averted by systematically replenishing the cash and fixed-income buckets, but separate research has shown that approach can actually result in less retirement income2. The retiree simply ends up dragging too much into cash/low-yield investments as those asset classes are constantly replenished over time. In fact, as it turns out, the best outcomes are the ones where the short-term buckets are used to mitigate sequence risk in the early years, but are not replenished. For instance, if the fixed-income assets are used to partially annuitize the portfolio, with the remainder predominantly or fully invested in equities (and never reallocated back to bonds later), the results actually improve3.

In fact, as our research on partial annuitization showed4, it turns out that much of the benefits being attributed to that bucketing strategy were not about the benefits of annuitization and having cash flows to avoid early withdrawals at all. Instead, the benefits of the strategy were actually primarily attributable simply to the path that the retiree’s asset allocation follows as a result of spending down fixed-income assets in the early years and letting equity exposure rise. We label this the “rising equity glide path” throughout retirement. In other words, it was less about “not liquidating stocks in down markets” and more about “letting equity exposure grow over time” instead. Accordingly, in our latest research paper (“Reducing Retirement Risk With a Rising Equity Glide Path,” Journal of Financial Planning)5, we delve further into this rising equity glide path effect and find that in reality, increasing equity exposure throughout retirement can actually enhance retirement outcomes. Doing so is so effective that the retiree can start more conservative and may even end up with less average equity exposure over their lifetime.

For instance, Figure 1 shows the probability of success (not outliving savings) of various stock/bond asset allocations based on a 4% withdrawal rate approach. The figure uses historical returns with an average annual compound real (inflation-adjusted) growth rate of 6.5% for stocks and 2.4% for bonds. The starting equity exposure is on the vertical axis of Figure 1, and the ending equity allocation is on the horizontal axis. Thus, for instance, a portfolio that starts at 60% in equities and ends at 60% in equities (the intersection of the 60% row and column) has a 93.2% probability of success. However, a portfolio that starts at 30% in equities and finishes at 70% in equities actually has a higher (95.1%) probability of success, not to mention a lower average equity exposure through retirement (an average of only 50% in equities instead of 60%).

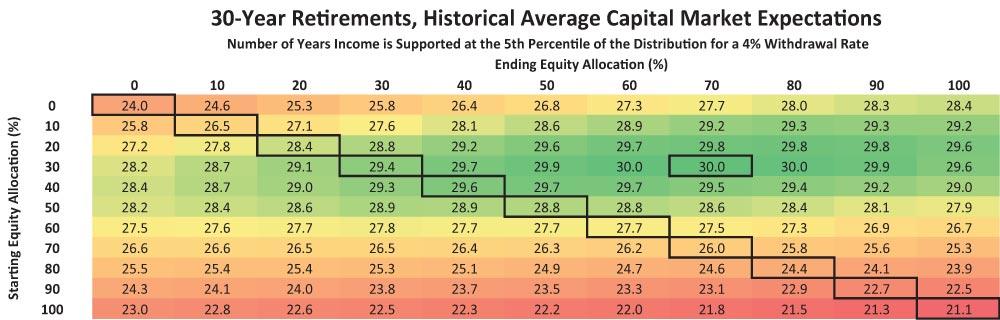

When viewing the magnitude of potential failures, we see a similar effect in Figure 2. Looking at how many years the portfolio lasts at the fifth percentile (i.e., how quickly we ran out in money in the worst one-out-of-20 scenarios), the 30% to 70% glide path portfolio lasts for 30 years, while the constant 60% equity exposure portfolio is depleted in 27.7 years (or faster) in the 5% worst scenarios. (It’s worth noting that historically, a 60% stock/40% bond portfolio has never actually failed, implying some potential for time diversification6 or mean reversion that we did not specifically model in our Monte Carlo analysis for this research.)

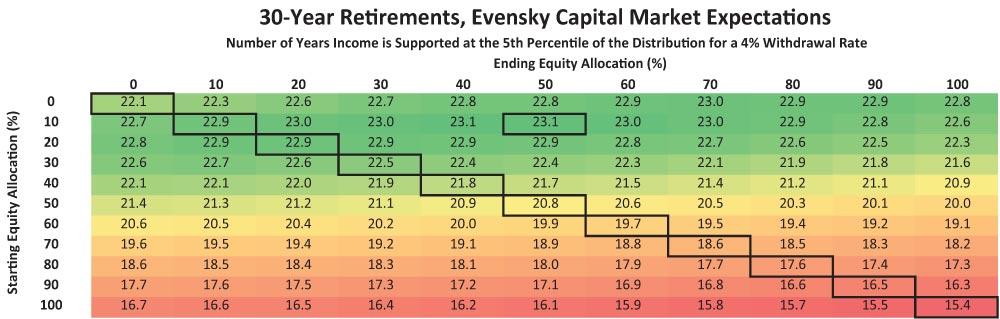

Of course, some will contend that today’s environment will have diminished returns, even over the long run, relative to historical standards. Accordingly, Figure 3 shows the glide path results with the return assumptions that Harold Evensky recommends for MoneyGuidePro7, a financial planning software package that is popular among advisers. The assumptions use arithmetic real returns of 5.5% for equities and 1.75% for bonds, which given their volatility result in geometric means of 3.4% and 1.5%, respectively. Notably, these assumptions reflect both a lower overall return environment compared to historical averages and also a reduced equity risk premium (i.e., the excess return of stocks over bonds is diminished).

Given the reduced return environment (and especially the reduced “bonus” for owning equities), all of the scenarios face earlier failure points. The “best” is only 23.1 years at the fifth percentile, while the optimal glide path becomes even more conservative, starting at 10% and rising to only 50%. Nonetheless, in this environment the rising glide path effect is still present. In fact, the conservative rising glide path lasts almost 20% longer at the fifth percentile than the static 60%/40% stock-bond portfolio.

From a retirement planning perspective, these results may be somewhat surprising. In a world where the conventional wisdom is that retirees should reduce their equity exposure throughout retirement as their time horizon shortens, this research suggests that in reality the ideal may actually be the exact opposite.

Yet, when viewed from the perspective of sequence risk, this result should not be surprising. After all, as shown previously in the May 2008 issue of The Kitces Report8, outcomes for a 30-year retirement time horizon are driven heavily by the results over the first 15 years (i.e., the first half) of retirement. If the first half of retirement is good, the retiree is so far ahead that a subsequent bear market cannot threaten their retirement goal (though obviously a late-retirement decline will reduce the remaining legacy at death). Conversely, if the first half of retirement is bad (e.g., a retiree starting in the late 1920s or late 1960s or, more recently, the late 1990s), there is a danger that even if returns average out favorably through the whole of retirement, if the portfolio is depleted too severely by withdrawals and bad returns in the early years, there won’t be enough (or any) money left when the good returns finally arrive. And notably, the truly dire situations are not merely severe market crashes that occur shortly after retirement, but instead the extended periods of “merely mediocre” returns that last for more than a decade9. These are far too long to “wait out” just using some cash and intermediate bond buckets.

In this context, the problem with the “traditional” approach of decreasing equity exposure through retirement becomes clear. If the retiree started in an environment like the late 1920s or late 1960s and decreases equity exposure systematically (e.g., by 1% to 2% per year), then by the time the good returns finally show up (about 15 years later) equity exposure will have been decreased so much that there simply won’t be enough in equities to benefit. In other words, even if spending was conservative enough to survive the time period, selling equities throughout flat or declining markets amounts to liquidating while the market is down and not being able to participate in the recovery and the next big bull market whenever it finally arrives. Conversely, when the equity glide path is rising and the retiree adds to equities throughout retirement (and especially in the first half of retirement), then by the time the market reaches a bottom and the next big bull market finally begins, equity exposure is greater and the retiree can participate even more.

Or viewed another way, the reality is simply that if market returns are poor throughout the first half of retirement, a rising equity glide path is the equivalent of systematically dollar cost averaging into the market (with all the benefits that entails). In contrast, decreasing exposure amounts to reverse dollar cost averaging out of a bad market (with all the adverse results that apply). The strategy effectively becomes a default mechanism to ensure that retirees are buying at favorable market valuations if they’ll need to do so to make their retirement work. And notably, this implies that other valuation-based investment strategies may also have favorable outcomes (as discussed in the May 2009 issue of The Kitces Report). In fact, the reality may simply be that a rising equity glide path is simply a way to ensure that retirees add to equities if valuations become cheap (i.e., returns are mediocre) through the first half of their retirement.

Of course, in a scenario where a retiree is following a rising equity glide path, and it turns out market returns are good—and the retiree suddenly winds up with far more wealth than ever anticipated—there’s always an option to change paths at that point, whether by bringing spending up or by taking equity risk off the table. Technically the retiree will be so far ahead that a rising equity glide path isn’t a “risk” (i.e., even with a bear market, they’re far enough ahead with few enough years remaining that there’s no more failure risk). But certainly some retirees will decide that, after a great bull market that changes their planning outlook and ability to achieve their goals, it may be prudent to get more conservative at that point. But for retirees who go through a poor market in the early years, the rising equity glide path becomes key to being able to sustain through the second half of retirement when the good returns finally arrive (in case the likely double-digit earnings yields on equities aren’t enticing enough at that point). In other words, the rising equity glide path becomes “heads you win, tails you don’t lose.” (Plus, in the former, more favorable scenarios, the retirees can change to whatever they want later instead).

From a practical perspective, there’s no doubt some challenge to actually becoming comfortable with the idea of increasing equities through retirement, given that many retirees are so fearful (and likely would be even more frightened and negative about stocks if they actually were going through a poor decade of results). Yet it’s worth noting from the research that: a) the average equity exposure is actually less than a classic static 60%/40% stock-bond portfolio; b) even results that just start conservative and end at 60% in equities end up better than those maintaining 60% in equities throughout (i.e., retirees don’t end with any more equity exposure than they would have had otherwise, they just start with less); and c) for many retirees, a rules-based approach like “just annually rebalance to a new equity exposure that increases by 1% per year” may actually be a more comfortable way to execute, because it’s based on a systematic rule and doesn’t require in-the-moment decisions that are difficult to execute in the midst of a scary market environment.

In other words, the glide path approach can be implemented just like a “normal” rebalancing approach and done systematically. The asset allocation to which the retiree is rebalanced shifts systematically by a small amount every year, as opposed to reverting back to a static amount (e.g., 60%/40%). If the retiree is rebalancing annually anyway, there may not even be any impact on total transaction costs; it’s just that the trades to buy/sell may be slightly larger or smaller in amount than they otherwise would have been. And as Kitces has written previously, the math of rebalancing alone is sufficient to ensure retirees don’t liquidate materially from equities during a bear market10, even without a separate cash reserve.

Ironically, though, perhaps the best way to handle the psychological aspects of implementing a rising equity glide path strategy is to frame it and think about it as a bucket strategy. As noted earlier, the research that we produced on partial annuitization showed that much of the benefits attributed to the bucket strategy were simply a rising glide path effect, and Pfau has also previously noted that in truth many bucket strategies are actually just an asset allocation mirage11 given that they often result in the exact same allocation that would have occurred without the buckets. On the other hand, there’s little doubt in practice that retirees mentally respond better to bucket strategies. As a way to frame and explain the glide path strategy, it can be highly effective to use the bucket analogy, as long as the bucket implementation doesn’t so distort the portfolio and the retiree’s balance sheet that it turns out to be harmful (as can be the case for large cash reserves).

For those who are still approaching retirement, the question remains about how best to transition into the lower-starting-equities rising equity glide path in retirement. The implication of this research is that the ideal strategy may be to begin decreasing equity exposure in the years leading up to retirement—as the retirement goal is approaching and it’s more dangerous to take the same amount of equity risk as the portfolio reaches its largest point: gliding downward in the years before retirement and then slowly climbing again thereafter. In other words, the ideal equity exposure throughout life may look something like the letter U, with equity exposure at its highest in the early years of accumulation, decreasing as retirement approaches, troughing as retirement begins, and then climbing again in the retirement years thereafter.

At the same time, though, while a rising equity glide path may be a more effective portfolio solution for sustaining a retirement income, the financial industry simultaneously still needs to do a better job in presenting, reporting, and explaining/thinking about it in a bucket format12—especially when suggesting and implementing a rising equity exposure throughout retirement. This is important in order to get investors comfortable with what otherwise may be an effective but initially counterintuitive retirement strategy.

Footnotes

1. “What Returns Are Safe Withdrawal Rates REALLY Based Upon?,” Nerd’s Eye View, August 15, 2012.

2. “Research Reveals Cash Reserve Strategies Don’t Work... Unless You’re A Good Market Timer?,” Nerd’s Eye View, June 6, 2012.

3. “Making Retirement Income Last a Lifetime,” John Ameriks, Robert Veres and Mark J. Warshawsky, SSRN, January 3, 2002.

4. “Understanding the True Impact of Single Premium Immediate Annuities on Retirement Income Sustainability,” Michael Kitces, Nerd’s Eye View, July 24, 2013.

5. “Reducing Retirement Risk with a Rising Equity Glide Path,” Wade D. Pfau and Michael E. Kitces, Journal of Financial Planning.

6. “Optimal Portfolios for the Long Run,” David Blanchett, Michael S. Finke and Wade D. Pfau, SSRN, February 5, 2014.

7. “MoneyGuidePro,” Harold Evensky.

8. The Kitces Report, May 2008.

9. “Why Merely Mediocre Returns Can Be Worse Than a Market Crash,” Michael Kitces, Nerd’s Eye View, February 22, 2012.

10. “Are Cash Reserve Retirement Strategies Really Necessary?,” Michael Kitces, Nerd’s Eye View, April 18, 2012.

11 “Understanding The True Impact Of Single Premium Immediate Annuities On Retirement Income Sustainability,” Wade D. Pfau, Nerd’s Eye View, July 24, 2011.

12. “Should Financial Planners Invest Using Bucket Strategies Or Just Report That Way?,” Michael Kitces, Nerd’s Eye View, May 15, 2013.

Portfolio Strategies

Investor Professor

Robert Sadofsky from NY posted over 12 years ago:

G Flowers from AZ posted over 12 years ago:

Charles S from TX posted over 12 years ago:

Tim Fenning from PA posted over 12 years ago:

John Eterno from TX posted over 12 years ago:

Roberto Plaja from Switzerland posted over 12 years ago:

Richard Thomas from FL posted over 12 years ago:

G Fischer from VA posted over 12 years ago:

Vern Andrews from CA posted over 12 years ago:

Donald Griffith from CA posted over 12 years ago:

Donald Griffith from CA posted over 12 years ago:

Harry Rich from OH posted over 12 years ago:

FinancialDave from WA posted over 12 years ago:

Dave Gilmer from WA posted over 12 years ago:

Ruben Rosales from MA posted over 12 years ago:

Michael Henry from OR posted over 12 years ago:

Steve Rawlinson from California posted over 9 years ago:

Scott Sarratt from VA posted over 9 years ago:

Pete Mumford from MN posted over 6 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account