Charles Rotblut leads a class in AAII's new Essential Investing Video Course. Go to https://www.aaii.com/ves for more information and to subscribe.

The allure of target date funds is simple: a single fund that provides a diversified portfolio and alters its allocation as shareholders approach the date when cash withdrawals will be taken. The promise of an “all-in-one solution” to investing for retirement is attracting both investors and employers. Yet, behind the simple appeal are complex strategies that offer more volatility and risk than these funds are perceived to have.

A target date fund is a mutual fund or an exchange-traded fund (ETF) designed so that its portfolio strategy evolves as a specified date nears. The date is listed in the fund’s name—for example, the Fidelity Freedom 2020 fund (FFFDX) is designed with a target date of 2020. An investor planning to retire in 2020, or within one or two years of that date, would consider investing in this fund.

As the target date moves closer, these funds change their composition to adjust for the level of risk the fund sponsor believes shareholders should be taking. The actual allocation and how often the allocation changes vary from fund to fund. Furthermore, at the target date, a fund can either adopt a final allocation or continue to evolve.

Target date funds are funds of funds. Instead of holding individual securities, they hold shares in other funds from within the same family. Fidelity target date funds, for instance, invest in other Fidelity funds. This allows the target date fund manager to focus on making allocation decisions instead of also having to consider what securities should be held. The downside is that an investor has no control over the funds chosen and is locked into the target fund’s family.

Shareholder Confusion

Any discussion of target date funds needs to start by addressing their biggest problem: Many investors don’t understand them. The premise of a single fund that fulfills an investor’s needs is appealing, but the simplicity of the pitch veils the underlying complexity and volatility of these funds. In 2008, target date funds were criticized for incurring larger losses than investors perceived they would incur. Four years later, a study by ING found that a large number of investors still don’t understand the very basics of target date funds (“Target Date Funds Misunderstood,” April 2012 AAII Journal; available at AAII.com). According to the study, just 44% of investors surveyed knew that a target date fund’s allocation is designed to automatically change over time.

Part of the problem may be that many investors simply don’t read the funds’ prospectuses. This is unfortunate because these documents, provided by every fund family, explain how a fund is designed, its investment strategy and expenses, and other important information. Target date fund prospectuses also provide information about how the allocation is designed to change over time and what happens both at the target date and afterward.

Another problem is that allocation strategies themselves may be misunderstood. A goal of a long-term allocation strategy is to find an optimum mix of long-term return and risk. A proper allocation strategy does not avoid losses; it helps to reduce the amount of risk to a level that is appropriate for a given investment time horizon and wealth level. Since target date funds cannot be adjusted to account for the wide variances in wealth among their shareholders, these funds are managed solely on the basis of time horizon. An investor with a long time horizon can tolerate significant short-term volatility since he has several years to recoup any bear market losses. Conversely, an investor with a short time horizon does not have as much ability to recoup market losses. Thus, as a person nears retirement or becomes fully retired, his portfolio’s allocation should become more conservative.

Allocation Strategies

Target date funds adjust their strategies by maintaining a higher allocation to stocks for longer-dated funds and a smaller allocation to stocks for shorter-dated funds. This can most clearly be seen when comparing target date funds offered by the same fund family. Vanguard’s Target Retirement 2015 fund (VTXVX) has 55.8% of its portfolio allocated to stocks and 44.2% allocated to bonds. Conversely, Vanguard’s Target Retirement 2035 fund ![]() (VTTHX) has 86.5% of its portfolio allocated to stocks and 13.5% allocated to bonds. Both funds share the same manager, Duane Kelly. The difference is that shareholders in the 2035 fund have a longer period until retirement and therefore can financially withstand more volatility.

(VTTHX) has 86.5% of its portfolio allocated to stocks and 13.5% allocated to bonds. Both funds share the same manager, Duane Kelly. The difference is that shareholders in the 2035 fund have a longer period until retirement and therefore can financially withstand more volatility.

| Fund |

Stock (%) |

Bond (%) |

Other (%) |

Cash |

| (%) | ||||

|

Fidelity Freedom 2020 |

48.9 | 36.5 | 0.9 | 13.7 |

| Schwab Target 2020 (SWCRX) | 60.3 | 34.3 | 0.8 | 4.6 |

|

T. Rowe Price Retirement 2020 |

69.5 | 24.1 | 0.9 | 5.5 |

| USAA Target Retirement 2020 (URTNX) | 40.7 | 48.8 | 2.5 | 8.0 |

| Vanguard Target Retirement 2020 Inv (VTWNX) | 63.4 | 32.0 | 1.5 | 3.1 |

| Thrift Savings Plan L 2020* | 54.5 | 7.3 | 38.2 | 0.0 |

| iShares S&P Target Date 2020 (TZG) | 61.5 | 37.6 | 0.7 | 0.2 |

| *The Thrift Savings Plan L 2020 holds an allocation in the G fund, which invests exclusively in a nonmarketable, short-term U.S. Treasury security that is specifically issued to the Thrift Savings Plan. | ||||

| Source: Morningstar Inc. and the Thrift Savings Plan and iShares websites. Data as of 8/31/2012. | ||||

It is worth noting that the 2015 fund has more than half of its assets allocated to stocks, even though the retirement date for its shareholders is less than three years away. This is not surprising since the need for growth does not end at retirement. Rather, as average life spans expand, so does the time period that withdrawals will be made from retirement savings. Retirees need a significant allocation to stocks to ensure that their portfolio grows at a rate faster than inflation over the long term to offset longevity risk (the risk they will outlive their portfolios)—even as they make periodic withdrawals from their savings. (The conservative allocation model on AAII.com calls for a 50% allocation to stocks.)

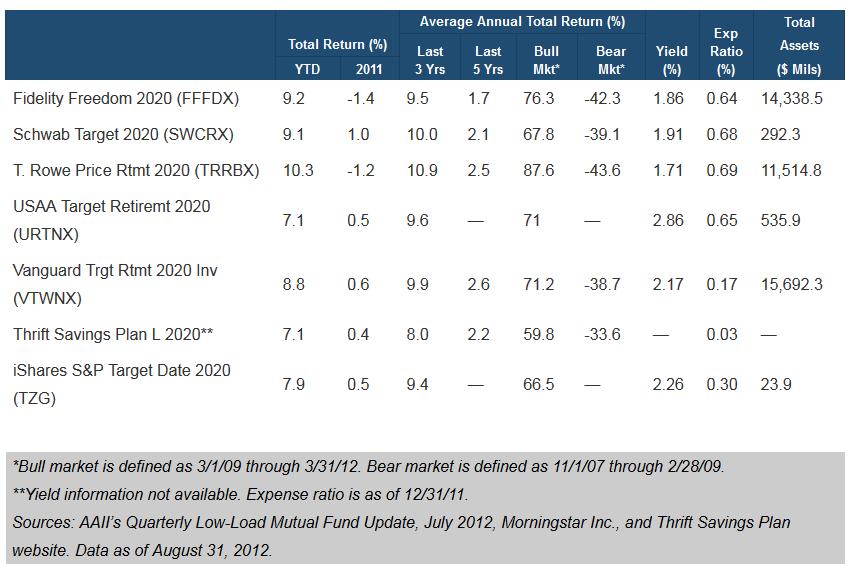

Table 1 and Table 2 show how the current and final allocation strategies vary for 2020 target date funds from various fund families. These funds assume shareholders will retire in 2020. (Typically, target date funds are offered in five-year increments.) The funds displayed are the largest for this category. I’ve also included the L 2020 fund from the federal government’s Thrift Savings Plan and the iShares S&P Target Date 2020 ETF (TZG) to provide comparisons of other target date funds that are available. (Target date ETFs have so far not attracted much in the way of assets, but this could change in the future.)

| Fund |

Stock (%) |

Bond (%) |

Other (%) |

Cash (%) |

Year |

| Reached | |||||

|

Fidelity Freedom 2020 |

20.0 | 40.0 | — | 40.0 | 2030–2035 |

| Schwab Target 2020 (SWCRX) | 25.0 | 68.0 | — | 7.0 | 2040 |

|

T. Rowe Price Retirement 2020 |

20.0 | 80.0 | — | — | 2050 |

| USAA Target Retirement 2020 (URTNX) | 30.0 | 70.0 | — | — | 2020 |

| Vanguard Target Retirement 2020 Inv (VTWNX) | 30.0 | 65.0 | — | 5.0 | 2027 |

| Thrift Savings Plan L 2020* | 20.0 | 6.0 | 74.0 | — | 2020 |

| iShares S&P Target Date 2020 (TZG)** | 31.5 | 68.2 | — | 0.4 | N/A |

| *The Thrift Savings Plan L 2020 holds a 74% allocation in the G fund, which invests exclusively in a nonmarketable, short-term U.S. Treasury security that is specifically issued to the Thrift Savings Plan. | |||||

| **The final allocation for the iShares S&P Target Date 2020 fund is based on iShares Target Date Retirement Income Index Fund (TGR) allocation. The actual final allocation may differ and the timing of when it will be reached is not specified in the prospectus. | |||||

| Source: Fund Summaries and the Thrift Savings Plan website. | |||||

The allocation strategies of target date funds are commonly divided into a “to” or a “through” approach. A “to” approach adjusts the allocation up to a target date, at which time it becomes finalized. A “through” approach continues to adjust the allocation past the target date. As you can see in Table 2, most target date funds glide past the target date, evolving in their allocation until a certain point after the target date. The amount of time the fund glides and what its final allocation is vary, however.

In reviewing the tables, you will notice that Vanguard allocates a greater percentage of its assets to stocks, both now and at retirement, than Fidelity does. These differences reflect divergent views on asset allocation. Though a common rule of thumb for determining the percentage of your portfolio to allocate to equities is to subtract your age from 110 (e.g., a 60-year-old would have 50% of his portfolio allocated to stocks), the actual number varies. Many in the finance community believe a significant allocation to equities is needed to fend off the adverse effects of inflation and longevity risk. However, the Vanguard fund has a shorter glide period than the Fidelity fund, reaching its final allocation by 2027 instead of Fidelity’s planned range of 2030 to 2035.

You can find out how the allocation of a target date fund evolves over time and what happens to the allocation at and after the target date by reading the fund’s prospectus.

Bear Market Volatility

As stated, allocation strategies are intended to control risk, not eliminate it. During bear market cycles, target date funds will lose money. In 2008, the losses were greater than many investors had anticipated.

Table 3 shows performance and expense figures for the largest target date funds, as well as similar Thrift Savings Plan and iShares funds. The bear market return column shows how each fund performed from November 1, 2007, through February 28, 2009. Using 2020 funds as an example, you can see how the T. Rowe Price Retirement 2020 fund ![]() (TRRBX) suffered the worst performance, losing 43.6% of its value. This was largely because TRRBX had the largest allocation to stocks of the funds shown. When the market rebounded, TRRBX led its peers with a bull market return (March 1, 2009, through March 31, 2012) of 87.6%. More stocks equal more volatility.

(TRRBX) suffered the worst performance, losing 43.6% of its value. This was largely because TRRBX had the largest allocation to stocks of the funds shown. When the market rebounded, TRRBX led its peers with a bull market return (March 1, 2009, through March 31, 2012) of 87.6%. More stocks equal more volatility.

Target date funds follow long-term allocations strategies; they are not designed to time the market. When prices for their largest asset class swing, so does the net asset value of the funds. Therefore, while target date funds will keep your portfolio allocation on track to achieve your long-term goals, they will experience volatility over shorter periods of time. Any investor planning to use target date funds must therefore approach them with the intent of holding such funds for the long term, rather than panicking and selling during bear markets.

All the funds have a mechanism for bringing their allocations back to the intended composition when market volatility causes one asset class to become too large or too small. The triggers for when this rebalancing occurs were not stated in the prospectuses reviewed for this article, however.

How Do You Choose?

There are two primary characteristics you want to consider when choosing among target date funds:

- the amount of volatility you are comfortable withstanding leading up to and at your retirement date, and

- the post-retirement allocation you think you will be comfortable with.

Your intended retirement date will influence the “year” of the target date funds you choose (e.g., 2015, 2020, 2025, etc.). If you plan to retire in 2020, the seemingly obvious choice would be to select a 2020 fund. However, if you do not expect to be reliant on your portfolio for retirement income—thanks to a pension or other sources of income—you could choose to go with a 2025 fund instead. A later-dated fund will give you a greater allocation to stocks at retirement and thereby more long-term growth. On the flipside, if you don’t think you will be able to withstand a bear market near your retirement date, you should consider a shorter-dated fund, such as a 2015 fund. Such a fund will have a smaller allocation to stocks on your retirement date, reducing downside risk and providing more portfolio income.

The trade-off for choosing a fund with a date that precedes or occurs after your retirement date is that you are either giving up potential portfolio growth or risking more market volatility. There are always trade-offs in investing, and while target date funds offer the allure of simplicity, they do not negate the tough decisions that an investor has to make.

Once the date for a fund is selected, the next step is to select an allocation glide path. As previously shown, each fund family has its own strategy for gliding to the final portfolio allocation. Vanguard evolves to the conservative allocation within seven years of retirement; T. Rowe Price takes 30 years. The Vanguard strategy will give you a more conservative, income-producing strategy sooner in retirement. The T. Rowe Price strategy will give your portfolio more opportunity to grow at a rate faster than inflation during your retirement years, but at the risk of increased volatility.

None of these funds moves out of stocks completely during retirement. Rather, it is the pace at which they reduce the exposure to equities in retirement that differs. It is up to each investor to determine his comfort level.

Performance and expenses do matter, but both are influenced by the size of the equity allocation. A higher comparative allocation to stocks will give better long-term returns, but will also increase risk. Greater bond exposure can increase costs, but reduces volatility.

Alternatives to Target Date Funds

Since most target date funds are merely funds composed of other funds, any investor can create their own synthetic target date fund. It comes down to determining the proper allocation and selecting funds that match the portfolio needs. Using our asset allocation models on AAII.com as an example, a portfolio could be constructed out of large-cap stock, mid-cap stock, small-cap stock, international stock, emerging market stock, intermediate-bond and short-term bond funds (www.aaii.com/asset-allocation). Doing so allows an investor to choose the best fund for each category, as opposed to relying on the performance of a pre-specified set of funds.

Following this approach requires more involvement, however. Not only must fund performance be monitored, but the investor also needs to make allocation decisions regarding the portfolio. A strategy must be implemented for reducing the portfolio’s exposure to stocks over the long term. In addition, it is up to the investor to rebalance his portfolio when the allocation percentages for each asset class stray too far from their desired range. Failure to do so can lead to increased volatility. Finally, the investor must be willing stay with stocks—and perhaps even increase his equity allocation—during bear markets.

Supplementing Target Date Funds

Target date funds tend to follow fairly basic allocations: domestic stocks, international stocks and bonds. Only Fidelity includes specific exposure to commodity companies. None of the prospectuses I read made any mention of micro-cap stocks.

An investor seeking to include a broader range of assets should start by reading the target date fund’s prospectus to see what it invests in. (This process will likely lead to reading the prospectuses of the funds held within the portfolio.) Once this information is known, assets outside of the dominion of the target date fund can be added to increase a portfolio’s diversification. The risk of the target date fund can also be adjusted by adding more stocks (to seek higher returns) or more bonds (to produce more income) to an individual’s portfolio. Doing so, allows the investor to customize the characteristics of his portfolio, while using a target date fund as his core strategy.

Related

Dispatches

Gordon Robinson from NC posted over 13 years ago:

Charles Rotblut from IL posted over 13 years ago:

Michael M from IL posted over 13 years ago:

James Selva from NY posted over 13 years ago:

Melvin Rosen from WI posted over 13 years ago:

Earl Mitchell from CA posted over 13 years ago:

Vaidy Bala from AB posted over 13 years ago:

Fletcher Cole from NH posted over 13 years ago:

Charles Rotblut from IL posted over 13 years ago:

Tony Hausner from MD posted over 13 years ago:

Tony Hausner from MD posted over 10 years ago:

Ed Ward from Georgia posted over 10 years ago:

Donald Myers from AZ posted over 8 years ago:

Donald Myers from AZ posted over 8 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account