Related

Portfolio Strategies

This portfolio has different return characteristics than a portfolio of large-cap stocks and long-term Treasurys but was capable of beating inflation.

by Charles Rotblut | June 2012

Charles Rotblut leads a class in AAII's new Essential Investing Video Course. Go to https://www.aaii.com/ves for more information and to subscribe.

“How can I construct a portfolio that is capable of producing returns different than those of the S&P 500 and long-term Treasurys and that is also capable of warding off the threat of inflation?” This is what many AAII members have asked me for.

The good news is that I was able to create such a portfolio. In fact, over the time period tested, its performance topped that of a traditional large-cap/long-term bond portfolio. The portfolio can be replicated using exchange-traded funds. Unfortunately, this alternative portfolio is more volatile than a traditional portfolio comprised of large-cap stocks and long-term bonds. Furthermore, the time period used to test the portfolio may not be long enough to show whether its performance advantage will last well into the future.

The alternative portfolio does complement a more traditional portfolio. It includes a mix of assets that provide diversification benefits to a traditional portfolio and enhanced returns over the time period studied. The benefits come at the cost of increased volatility, however. Thus, the alternative portfolio’s best use may be as a supplement to, rather than as a replacement of, a more traditional portfolio.

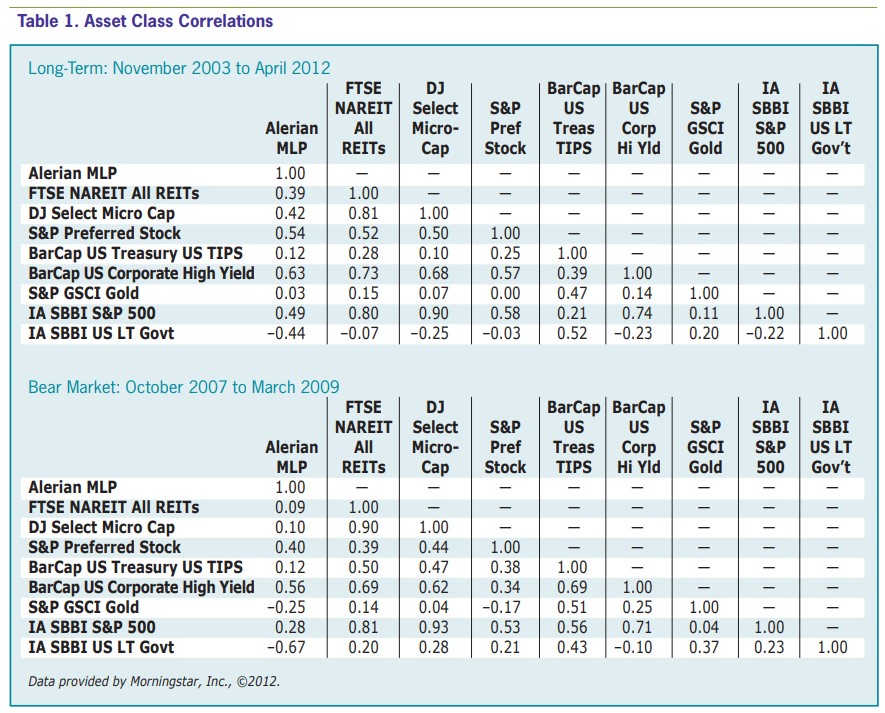

One of the most basic building blocks for any portfolio is correlation. In terms of investing, correlation shows how similar the returns of two asset classes are. Correlations of, or near, +1.00 imply that assets experience the same type of return characteristics. Correlations of, or near, –1.00 imply that assets tend to have completely opposite return characteristics. Correlations of, or near, 0.00 imply that the assets have different return characteristics. Two assets with a correlation near +1.00 will typically move in the same direction and will experience similar magnitudes of change in price. Assets with correlations near 0.00 will have different returns: As one asset moves up in price, the other may move up in price, move down in price or stay unchanged. There is no relationship between the return characteristics.

Historically, large-cap U.S. stocks and long-term government bonds have had a correlation of 0.06, according to the 2012 Ibbotson Stocks, Bonds, Bills, and Inflation (SBBI) Classic Yearbook (Morningstar, 2012). This implies that simply combining the two asset classes in a portfolio gives diversification benefits. Including other asset classes increases the level of diversification benefits, but only to varying degrees. Small-company stocks have a –0.09 correlation with long-term government bonds, but a 0.72 correlation with large-cap stocks. Long-term government bonds have a 0.06 correlation with large-cap domestic stocks, but a 0.89 correlation with long-term corporate bonds. In other words, small-cap stocks experience similar, but not the same, types of returns as their large-cap counter parts. The same holds true for long-term government bonds and long-term corporate bonds.

As you can see, once you move beyond two asset classes, it becomes more difficult to construct a portfolio completely out of assets that are not highly correlated with at least one other asset. Leveraged strategies, hedge fund strategies, currencies and derivatives can help. The downside is that these investments are often more complex and harder to analyze, can be more risky, and may be more expensive to use.

It is also important to realize that during periods of financial distress, correlations tend to move toward 1.00. This is what occurred during the 2008 financial crisis, when global stock prices fell, as did prices for other asset classes. These types of movements are tied to the human tendency of wanting to sell all risky assets when a bear market roars. Once a crisis ends, correlations widen, meaning they pull away from 1.00. This is why, when constructing a diversified portfolio, it is important to pay attention to long-term correlations.

Correlation only measures the similarity in returns, not whether one asset has a higher or lower return than another. It does not tell you how risky any particular asset is, either. Financial goals, time horizons, the emotional ability to withstand losses, and other factors impact an investor’s risk tolerance and influence the level of returns desired and the type of assets held. Thus, a portfolio designed solely to be well diversified from the standpoint of correlation without taking into consideration other factors may be completely unsuitable for many investors.

My goal was to create an alternative portfolio that is diversified and investable and that avoids complex strategies and assets. I wanted this portfolio to be accessible to individual investors who were comfortable buying and selling exchange-traded funds (ETFs).

To accomplish this goal, I started with a few basic rules for building the portfolio. First, the selected assets had to have low, or at least reduced, correlations with the S&P 500 index (which is comprised of domestic large-cap stocks) and long-term Treasury bonds. Secondly, the assets had to have low correlations with the other assets held in the portfolio. Third, it had to be easy for the average individual investor to buy and sell investments in those assets. Finally, the investments had to be easy to understand and track, and they could not use any type of leverage.

These rules might seem simple, but they have large implications. Requiring all investments to be easy to buy or sell by the average investor made annuities, non-public real estate, hedge funds and private equity off limits. The requirement that investments be easy to understand and that they not use leverage eliminated convertible bonds, option strategies, futures, exchange-traded notes, inverse and leverage (e.g., ultra) funds, currencies, and funds that mimic hedge fund strategies.

Why be so seemingly strict? Costs were one reason. Liquidity was another: I wanted a portfolio with investments that are easy to buy and sell through a traditional brokerage account. Doing so enables rebalancing and helps those investors facing required minimum distributions. Simplicity reduces risk. An easy way to lose money is to buy an investment you don’t understand.

Working within these restrictions still gave me a quite a bit of leeway in choosing what to add and what to restrict. I felt a bit like a mad scientist walking into a laboratory. I knew what I wanted to create, but wasn’t completely sure what type of portfolio I would end up with once I started tossing assets into a beaker.

So, I started with a bit of brainstorming to figure out what assets would make sense. On the equity side, I chose master limited partnerships (MLPs), real estate investment trusts (REITs) and micro-cap stocks. On the bond and income side, I chose Treasury inflation-protected securities (TIPS), high-yield corporate bonds and preferred stocks. Finally, I selected gold to provide exposure to commodities via a physical asset.

A few notes of explanation about these asset classes:

To see whether these assets not only offered reduced correlations with large-cap stocks and long-term bonds, but also relative to each other, I reached out to Annette Larson and Michelle Swartzentruber at Morningstar. I asked them to run the numbers on each of the asset classes and compare them to large-cap stocks and bonds.

The results are presented in Table 1. The table is presented in grid format, so you can see the correlations between any two of the asset classes used in the alternative portfolio and how they compare to large-cap stocks and long-term Treasurys. The correlations for most asset classes are below 0.60, which implies they would provide diversification benefits when held together in a portfolio. There are a few areas, however where the correlations run higher.

High-yield corporate bonds have a 0.73 correlation with REITs, a 0.68 correlation with micro-cap stocks and a 0.74 correlation with large-cap stocks. Though higher than I would have expected, this is not surprising. Demand for high-yield bonds ebbs and flows with economic trends. Periods of economic expansion reduce default rates and increase tolerance for risky assets like junk bonds. Periods of economic contraction increase default rates (declining profits make it more difficult for companies to repay their debt) and reduces tolerance for risk. You may also notice the 0.63 correlation between high-yield bonds and MLPs. I cannot attribute it to the comparatively high yields offered by both, because the correlation between MLPs and REITs is just 0.39. If yield were the factor, I would expect MLPs and REITs to have a higher correlation.

Micro-cap stocks have a 0.90 correlation with large-cap stocks and a 0.81 correlation with REITs. REITs have a 0.80 correlation with the S&P 500. These elevated correlations are tied to investor sentiment toward stocks. During bull market periods, demand for equity-type investments rises; during bear market periods, it falls. The correlations are still below 1.00, however, and signal that there are diversification benefits to be realized.

Gold had the lowest overall correlations, but it is difficult to value and produces no cash flow.

Due to the limited histories of the some of the indexes used for this study, the data only goes back to 2003. If the data were to be calculated over a longer period, it is possible that the numbers could change and show either larger or smaller diversification benefits.

The second grid in Table 1 shows how the bear market of October 2007 through March 2009 affected correlations. Correlations for some assets moved closer together, such as micro-cap stocks and large-cap stocks. Again, this is common during periods of market distress. Correlations fell for some asset combinations, reflecting differences in attitudes toward each asset class. One example is micro-cap stocks and MLPs, which saw correlations fall from 0.42 to 0.10 during the last bear market.

I calculated performance using monthly total returns for the following:

Allocating among these indexes was a challenge, because of a lack of available models to base this type of portfolio on. So I created an alternative portfolio and a supplemental portfolio.

The alternative portfolio was based on the 70% stocks/30% bonds composition used for our moderate portfolio allocation model. (This model can be viewed at www.aaii.com/asset-allocation.) I evenly allocated 60% among MLPs, REITs and micro-cap stocks, since they track stocks and equity-like vehicles. I assigned 10% to gold since the volatility and cash flow characteristics of commodities make them more akin to stocks than bonds. The remaining 30% was split evenly between preferred stocks, TIPs and high-yield bonds, since all three have specific income-producing benefits.

The supplemental portfolio mixed a traditional large-cap stock/long-term Treasury allocation with the alternative assets. This portfolio started with a 70% allocation to traditional assets, split 70/30 between stocks and bonds (49% of the total portfolio was allocated to domestic and international stocks and 21% was allocated to long-term Treasury bonds). The remaining 30% of the portfolio was allocated to the alternative assets using a proportional split based on the alternative portfolio allocation. This meant REITs, MLPs and micro-cap stocks each received a 6% allocation; preferred stocks, TIPS and high-yield bonds each received a 3% allocation; and the remaining 3% was allocated to gold.

To provide a means for comparison, I also created a benchmark portfolio that held a 70% allocation in large-cap domestic stocks and a 30% allocation in long-term Treasury bonds.

All three portfolios were rebalanced when the allocations drifted off target by five percentage points or more at the end of a calendar year. When this occurred, the portfolios were rebalanced back to their original allocation targets. The alternative portfolio was rebalanced at the start of January 2007, January 2009 and January 2010. The supplemental and benchmark portfolios were rebalanced at the start of January 2009 and January 2010.

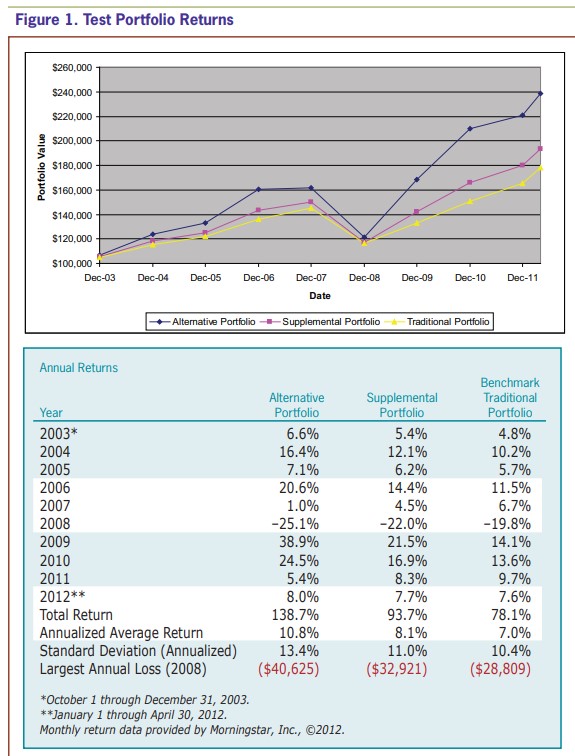

The performance of all three portfolios can be seen in Figure 1. The alternative portfolio generated the best returns, but was also the most volatile, as measured by standard deviation. The supplemental portfolio has the second-best performance, but also the second-highest level of volatility. The benchmark portfolio had the lowest level of volatility, but also the lowest rate of return. The alternative portfolio also realized the largest loss in 2008 of the three portfolios.

Part of the reason the alternative portfolio had the highest level of volatility, and the biggest loss in 2008, was that correlations between the asset classes moved closer together. When Annette and Michelle ran the data for October 2007 through March 2009, they calculated that micro-cap stocks had a correlation of 0.90 with REITs. The correlation between micro-cap stocks and large-cap stocks rose to 0.93. These numbers show that when investors panic, they tend not to be discriminatory about what they sell. Thus, what might be diversified under calm market conditions may not be so diversified under periods of market duress.

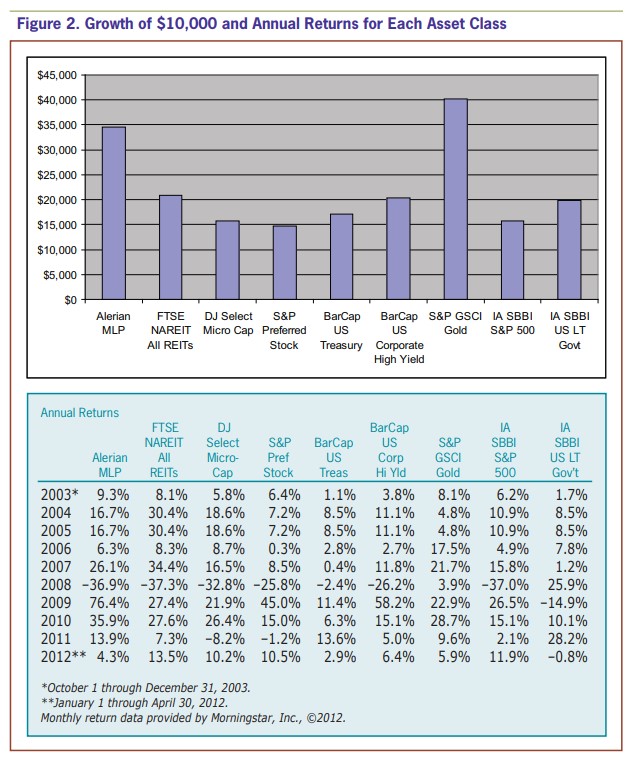

Figure 2 details the performance for each asset class, showing both the cumulative growth of a $10,000 investment in each asset class and the year-by-year returns. Gold produced the highest returns over the period studied, while preferred stocks produced the lowest return. Keep in mind that this is a relatively short time period and performance over the next 10 years may differ.

The return data demonstrates a few important points. First, reduced correlations do not eliminate volatility. Diversification reduces the risk of holding any one asset, but if you construct a portfolio out of risky assets, you will still have a risky portfolio. The difference is that your portfolio will be less risky than if you only held one or two assets that were highly correlated with each other. Second, during periods of market distress, the benefits of diversification are reduced. Third, there is a trade-off between risk and return. The alternative portfolio delivered the best overall performance, but it also was the most volatile. Fourth, the alternative portfolio only worked well for the time period tested. Over a longer period of time, the returns may differ and could potentially lag those of a more traditional portfolio.

If your goal is to create a portfolio that preserves your capital, you should consider constructing a bond ladder or purchasing annuities. Among the downsides, however, is the potential that you will not achieve a high enough return after costs to grow your assets at a pace faster than inflation. Thus, while you can reduce volatility, you cannot do so without sacrificing absolute return. You must choose between how much return on capital and return of capital you desire. As the alternative portfolio shows, you can use non-traditional assets to increase return on capital, but at the trade-off of risking return of capital.

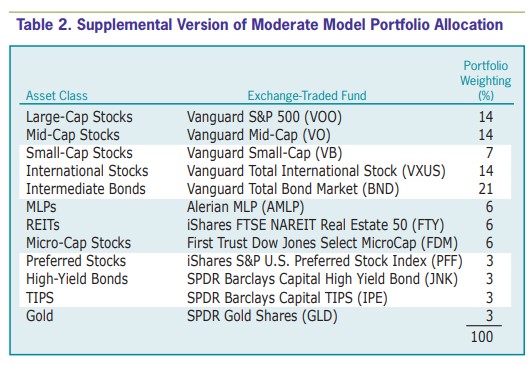

Thus, the best strategy may be to incorporate the alternative portfolio into an existing portfolio, but modify the allocations proportionately to fit your financial goals and tolerance for risk. Using our moderate portfolio allocation model as a basis, Table 2 shows what a supplemental portfolio would be like using exchange-traded funds (ETFs). Note that ETFs similar to the ones listed do exist and may warrant using if your broker provides commission-free trading, if the annual expenses are cheaper or if they are more actively traded. Just be sure to read the prospectus to ensure you understand exactly which index the ETF tracks.

Keep in mind that you do not have to own every asset class included in the alternative portfolio. Gold, MLPs and TIPS had the lowest across-the-board correlations, whereas micro-cap stocks had the highest correlations over the time period studied. Since correlation does not factor in the absolute return or valuation, you should consider the risks—including the potential for future losses—before adding any asset to your portfolio.

Portfolio Strategies

Commodities

Ed from New Jersey posted over 14 years ago:

Morton from NC posted over 14 years ago:

Robert from MA posted over 14 years ago:

Floyd from FL posted over 14 years ago:

Billy from CO posted over 14 years ago:

David from WA posted over 14 years ago:

Teck See from Malaysia posted over 14 years ago:

Charles Rotblut from IL posted over 14 years ago:

Hwan Perreault from WA posted over 13 years ago:

R Herrera from TX posted over 13 years ago:

Ed from NJ posted over 12 years ago:

Michael Henry from OR posted over 12 years ago:

Barry P. from FL posted over 12 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account