Related

Financial Statements

In this article, we showcase an example of a balance sheet and give you a clear understanding of the assets, liabilities and equity sections of this company report.

This financial statement analysis article marks the third piece in our ongoing series.

It is important as an individual investor to examine the balance sheet’s assets and liabilities as well as shareholder’s equity to effectively evaluate a company. That’s where this guide comes in. We walk you through balance sheets, one step at a time.

The balance sheet is the starting place to analyze a company’s financial strength. Unlike the income statement, which details a firm’s earnings and expenses over a period of time, the balance sheet lists all of a company’s assets and liabilities at a single point in time. The balance sheet provides a snapshot of a firm at the end of a fiscal quarter or year. The income, expenses and cash flow that come into and leave a firm during a period are not shown; rather, the balance sheet represents the total impact of all of these transactions at a certain date.

Annual and quarterly reports issued by companies are the best place to find the balance sheet. A firm’s annual report is typically available in the investor relations section of the company website. Separately, quarterly (10-Q) and annual (10-K) reports are required to be filed with the U.S. Securities and Exchange Commission (SEC) and are available to the public online through EDGAR (www.sec.gov/edgar.shtml).

On AAII.com, A+ Investor subscribers can access a summary of a company’s balance sheet by typing the stock symbol via the search bar on the home page. Select “Financials” on the stock evaluator page; you can toggle between the latest quarterly and annual financials. For even more information about a company’s balance sheet, you can visit major investment websites such as Morningstar.com and Yahoo Finance to find financial statements.

There are three major sections of the balance sheet—assets, liabilities and stockholder’s equity. It is crucial to remember that, as the name of the report implies, the sections must balance. The asset side of the balance sheet must equal the sum of liabilities and shareholder’s equity on the other side of the report.

Assets are items that the company owns and uses to conduct business. Liabilities are what the company owes to others. Shareholder’s equity is essentially what is left over, similar to a company’s “net worth.” A simple way to understand the balance sheet is to use your personal finances as an example. Your assets may include checking accounts, cars, properties and retirement savings. Some of these are short-term in nature, such as cash, and others are longer-term, such as a car or house. You may also have various liabilities that can include utility bills, car payments and mortgages. Like assets, some of these liabilities are short-term (e.g., utility bills) and others are long-term (e.g., the portion of your mortgage not due over the next 12 months). The difference between your assets and liabilities is your net worth, which is equivalent to a company’s equity.

Assets and liabilities arise during business transactions. For example, a company may issue debt to build a plant, expanding its business. This transaction increases both the assets (the plant) and the liabilities (the debt) sections of the balance sheet.

Studying assets, liabilities and equity can give individual investors an advantage at judging whether a company might be a strong or weak portfolio addition.

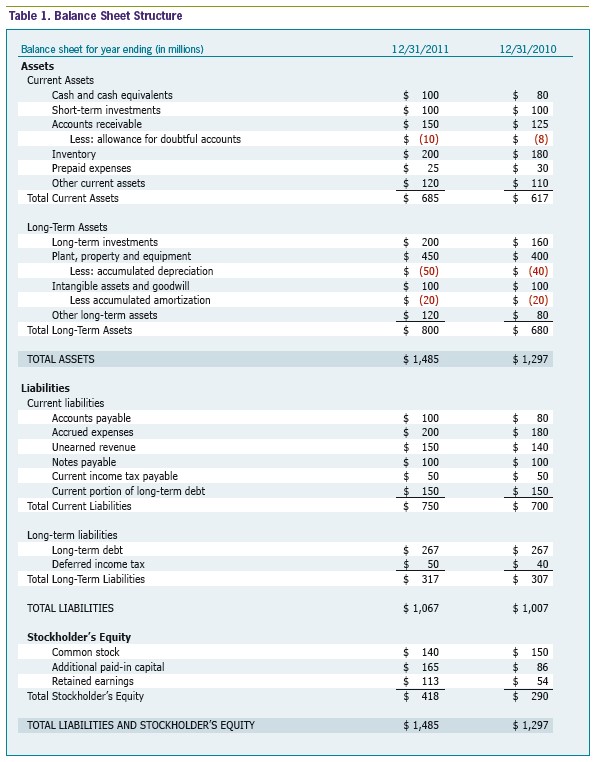

A typical company balance sheet is presented in Table 1. Different companies will report different line items on their balance sheets, and most companies also present notes to the financial statements that provide further details on the construction of various balance sheet accounts and the assumptions behind the reported figures. Most companies also report their total current assets and liabilities on the balance sheet; these figures are commonly used in ratio analysis.

Most company balance sheets look similar, showing major asset classes such as inventory and accounts receivable and liabilities such as accounts payable and unearned revenue. The balance sheets of banks are noticeably different, due to their distinctive business nature. Major asset classes that banks may report include net investment securities and net loans, while reported liabilities typically include deposits and securities sold.

In the next few sections, we examine common balance sheet items and discuss how they are used in investment analysis.

Assets are resources controlled by a company from which the firm expects to generate future benefits. Simply put, these balance sheet items represent what a firm owns. There are two types of assets on the balance sheet: current and long-term assets.

An asset is classified based on the length of time before it is expected to be consumed or converted into cash. The current assets on balance sheets are assets that are highly liquid and intended to be used during the course of the next year or during the current business cycle, whichever is longer. Current assets on balance sheets are typically listed in order of liquidity, beginning with cash and cash equivalents. Cash is the most liquid asset.

Cash equivalents include money invested in highly liquid assets for use within a 90-day period. These investments include money market funds and short-term Treasury bills.

Cash balances vary depending on the company’s industry. Certain industries, such as manufacturing, need more cash on hand than others, such as technology. The current ratio (current assets divided by current liabilities) and quick ratio (current assets less inventory divided by current liabilities) can be used to provide insight on cash levels. When analyzing cash, be sure to evaluate reported cash against competitors and industry norms.

Too little cash may not bode well for a firm, bringing into question its ability to maintain daily operations and pay obligations. However, too much cash may be problematic and may reduce the earnings potential of a firm. A well-run firm should be able to earn more through its normal business than the prevailing interest rate. Vast amounts of cash may also spur management to make poor decisions instead of making prudent investments or returning value to shareholders. Additionally, high-growth companies need cash on hand to fund expansion. Conversely, slowing or contracting businesses may temporarily see cash levels rise as expenditures are curtailed at a pace faster than the decline in revenues.

Accounts receivable is the amount owed to a firm from credit extended to customers for purchases. A relatively low accounts receivable figure may mean that a company is efficient in collecting its payments, that credit standards are strict (which can depress sales), or that a company operates in a payment-on-demand business (e.g., restaurants). A high accounts receivable figure may mean a company is having difficulty collecting payments or that credit standards are too loose. A better understanding of a firm’s accounts receivable figure can come from analysis over several years. Accounts receivables increasing at a substantially faster rate than overall sales is a potential red flag, signaling that the firm may be relaxing credit standards to boost sales. It can also mean that customers are having problems paying their bills, a troubling sign for future revenues and profits. In either case, as accounts receivables increase, a larger portion of invoices due will be uncollected, which reduces the value of the balance sheet line item. Companies may maintain a reserve against potentially uncollectable accounts receivables, titled ‘allowance for doubtful accounts.’ This contra-asset account represents management’s estimate of the dollar amount that will be uncollected because of customer defaults.

Keep an eye on the accounts receivable turnover, calculated as net credit sales divided by average accounts receivable. A significant or noticeable trend of change in accounts receivable turnover should be investigated. Note that accounts receivable turnover also varies by industry. Industries such as food and beverage have a higher proportion of cash transactions than industries such as automotive, leading to a higher accounts receivable turnover.

Inventory includes parts, raw materials (e.g., steel), products and other unsold goods that a company holds for sale to its customers. A certain inventory level is needed for firms to be able to meet demand and not lose sales opportunities. However, companies with very high inventory levels risk being unable to convert their inventory into sales. This balance is especially important in industries with constant product innovation. Over time, inventory can become obsolete or lose value if there is a product glut. For example, in the technology sector, the personal computing industry is very fast-moving. Firms with low inventory levels will lose customers who are buying computers and expect them within days. Firms with high inventory may risk being unable to sell computers at a reasonable profit or being stuck with out-of-date units. It is important to keep an eye on this figure; it should grow at roughly the same rate as sales.

Prepaid expenses account for goods and services that have been paid for, but not yet consumed. For example, the unexpired portion of an insurance premium will show up as a prepaid expense. The asset will be reduced as the goods or services are provided, while an expense will be recorded on the company income statement. The expense reduces net income and thereby reduces retained earnings, a shareholder’s equity line item that keeps the balance sheet in balance.

Other current assets on the balance sheets can be short-term loans or restricted cash that is short-term in nature and not directly applicable to the previously listed line items.

Most firms provide a total for current assets on the balance sheet. This amount is useful to compare against current liabilities (the higher the ratio, the better). We will discuss its use further in an article on ratio analysis.

Long-term assets on balance sheets are assets that are not intended for use within 12 months or within the current business cycle.

Long-term investments are stock, debt or royalties that a company intends to hold for a prolonged period.

Plant, property and equipment consist of fixed assets that a company acquires to maintain operations. Fixed assets are for long-term use and are not intended to be sold or quickly consumed. This account generally consists of the cost of buildings, machinery and computers less accumulated depreciation on the assets. The cost of a fixed asset is written off as noncash expenses each year over the estimated useful life of the asset.

Certain fixed assets depreciate faster than others. For instance, computers have a much shorter useful life than buildings. Additionally, even after an asset is fully depreciated and is no longer accounted for on the balance sheet, it may still hold some value.

The importance of plant, property and equipment varies by industry. Capital-intensive industries such as manufacturing will have more invested in fixed assets in the form of machines and factories. Be sure to compare a company’s plant, property and equipment figure to industry norms.

Goodwill is the premium paid over the accounting value of an acquired firm’s net assets. It reflects the extra value of an ongoing concern (a company’s ability to stay in business), potential market share gains, brands and other intangibles. A premium is often paid when an acquired company owns brands or recipes that have special value. For example, in the unlikely event of a firm being able to acquire Coca-Cola Co. ![]() (KO), its secret recipe would undoubtedly fetch a significant premium over the historical book value of its assets, which would be reported as goodwill on the acquiring firm’s balance sheet.

(KO), its secret recipe would undoubtedly fetch a significant premium over the historical book value of its assets, which would be reported as goodwill on the acquiring firm’s balance sheet.

Companies may overestimate goodwill. An acquiring firm will often pay a premium for a firm, based on expectations of future synergies and market share gains that may or may not be realized. The Financial Accounting Standards Board (FASB) requires companies to test goodwill for impairment at least annually. If the fair value of the goodwill is less than the reported value, the company must recognize the difference. This means reducing the reported value of goodwill and taking a noncash charge on the income statement. It is common for analysts to subtract intangible assets from shareholder’s equity to calculate a tangible net worth.

Intangible assets are other non-physical assets that have value, such as trademarks, copyrights and patents. Intangible assets that expire, such as patents and copyrights, lose value over time as they get closer to their expiration date and therefore must be amortized. Amortization is a noncash expense.

A company may also own other long-term assets on the balance sheet, such as restricted cash, overfunded pension benefits and deferred charges.

Total assets is the sum of the current and long-term assets. This amount is used in common ratios, such as liabilities to total assets (total debt to equity) and return on assets (net income divided by total assets). Total assets will also always equal the sum of liabilities and shareholder’s equity.

Liabilities are the obligations of a firm that require settlement at a future date. These balance sheet items represent what a firm owes. There are two types of liabilities on the balance sheet: current and long-term liabilities.

By definition, current liabilities on the balance sheet are obligations that have a maturity date that is less than one year or one business cycle away. These liabilities may arise from a number of transactions, but they are usually covered by several line items on the balance sheet.

Accounts payable is a major portion of most firms’ current liabilities on the balance sheet. This line item represents credit extended by suppliers to the firm, similar to the accounts receivable asset representing credit extended by the firm to its customers and distributors. This liability is typically paid as inventory is sold and cash is collected from customers. Accounts payable is another item that should fluctuate, over the long run, at a pace comparable to sales. If you notice slowing rates of payable turnover (credit purchases divided by average accounts payable), it may signal that the company is struggling to pay its bills. Increasing accounts payable should also be accompanied by increasing cost of goods sold and inventory.

Accrued expenses represents expenses that have been incurred but have not yet been paid. The most common accrued expenses are rent and salaries.

Unearned revenue is proceeds of sales for orders that have yet to be fulfilled or services that have yet to be rendered. The proceeds are shown as a current liability because the money has been received and the firm is liable for the product or service within the next 12 months or before end of the business cycle.

Notes payable represents short-term funds borrowed from financial institutions. Income tax payable is self-explanatory, marking income taxes owed to government entities.

The line item called ‘current portion of long-term debt’ reflects the portion of outstanding long-term debt that must be paid back within one year. This figure should be scrutinized, as a company must have the resources to retire this portion of its total debt either in the form of cash on hand or through the issuance of new debt.

Be sure to keep a close eye on total current liabilities when it is reported on the balance sheet. Firms must have sufficient liquidity to cover current liabilities coming due, or else they may have to incur more debt to cover the upcoming costs. As with total current assets, this figure is used in many liquidity ratios.

Long-term liabilities on the balance sheet are obligations that have maturities that are more than one year away. Long-term liabilities can include deferred income tax, long-term debt such as bonds, and pension obligations. The majority of long-term debt that firms accrue comes from issuing bonds that have periodic interest expense payments.

Just as with cash, long-term liabilities on the balance sheet as well as any outstanding debts should be carefully scrutinized. A company using long-term debt properly can generate value for shareholders. However, the amount of long-term debt on a company’s books should be reasonable. For example, using long-term debt to fund expansion projects provides tax deductions through interest payments and does not dilute shareholder’s equity, while allowing the company to fund profit-producing assets. The downside is that a company must be able to pay back its loans with interest. In addition, bondholders hold priority over shareholders in the event of liquidation. Once again, capital-intensive businesses require more cash, potentially leading to more long-term debt. Be sure to analyze long-term debt relative to industry norms.

As we mentioned in the first article in this series, a company may keep two separate sets of books—one for tax purposes and one to report to shareholders. Firms may account for depreciation aggressively when preparing tax filings in order to report lower profits, and thereby owe lower taxes, to the IRS. Contrarily, firms may use less aggressive depreciation methods when reporting to shareholders, resulting in higher profits and income taxes. The difference in the income tax between the two calculations shows up as ‘deferred income tax’ under long-term liabilities on the balance sheet.

Total liabilities is the sum of short- and long-term liabilities. This figure should not equal total assets (or worse yet, exceed total assets), as that would imply that shareholders have no assets to lay claim to.

The stockholder’s equity section of balance sheets includes the balancing amount after taking liabilities from assets. This is the firm’s net worth, or the net assets that shareholders can lay claim to.

Common stock has a par value (often just a penny) that is reported and that is generally meaningless. Stock offerings for common shares are conducted at a price significantly above the par value. To account for the difference between the offer price and the par value, companies maintain an account titled ‘additional paid-in capital.’

Another common shareholder’s equity account is retained earnings, which reflects the amount of earnings not returned to owners through dividends. As the name implies, these earnings are “retained” and reinvested back into the business.

There are a few other line items regarding the stockholder’s equity section of the balance sheet that companies may also report. Treasury stock represents the amount paid for shares that a company has repurchased. Treasury stock is listed as a negative number on the balance sheet because cash was used to purchase these shares. Companies may also list preferred stock, which is a hybrid security that companies sell in order to raise capital. These shares pay a regular dividend, but they have limited voting power. In the event of liquidation, preferred shares have priority over common shareholders, but not over bondholders.

Analysts often calculate book value as tangible assets less total liabilities. This amount is the value that shareholders would theoretically receive in the event of liquidation and is different from market value, which includes the value of a going concern. The stockholder’s equity section of balance sheets is important to evaluate before investing in any company or security.

The balance sheet provides a snapshot of a firm’s assets, liabilities and shareholder’s equity at a single point in time. It is important to analyze balance sheet trends across a period of time, as well as in relation to major competitors and industry norms. For many companies, year-over-year comparisons of financial statements are better than quarter-over-quarter comparisons because of seasonal factors. Big orders, sales or the initiation of big projects at the end of the quarter can also have an impact on quarterly filings.

As an investor, you want to make sure you fully understand the company that you’re investing in. To ensure that you are choosing the right security for your portfolio, you should take advantage of helpful resources like our A+ Investor service. A+ Investor offers a robust suite of screening tools that can help you vet that stocks could be good additions to your portfolio. Learn more and subscribe today.

If you’re interested in learning more about a company’s balance sheet or how to analyze this important report, check out the list of additional resources we’ve compiled.

Financial Statements

Financial Statements

Financial Statements

John from WA posted over 14 years ago:

Leslie Fewster from MD posted over 13 years ago:

Luca Bertozzi from NY posted over 8 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account