Charles Rotblut leads a class in AAII's new Essential Investing Video Course. Go to https://www.aaii.com/ves for more information and to subscribe.

Multiple studies have shown that price to book value (P/B) is the most effective valuation measure in determining a stock’s performance. Although the price-earnings ratio (P/E) is considerably more popular, buying at low price-to-book multiples leads to better returns.

Book value is the theoretical value of what a company’s net assets are worth. It is also referred to as equity. In theory, book value is equivalent to the amount of cash shareholders would receive if all of the company’s debts, both short-term and long-term, were paid off and all remaining assets were sold. Its compelling use as a measure of valuation can be explained in one statement:

No quality company should sell for a price equivalent to or less than its theoretical liquidation value.

Remembering and constantly applying this statement will do more to help you make money than just about any other investment concept. Benjamin Graham encouraged investors to look for companies trading near or below their book values in his 1934 classic “Securities Analysis.” More than 75 years later, buying stocks trading at low price-to-book multiples (share price divided by book value per share) continues to work.

The reason why book value is such a powerful measure of valuation lies deep in the concept of what book value is and what it means to an ongoing business concern. Book value is what a company’s net assets are worth. A price-to-book multiple of 1.0 means the company is worth the same as its net assets. This multiple means the market is indifferent as to whether the company opens its doors tomorrow. If the business is shut down, the debts paid off and the assets liquidated, shareholders’ wealth will, theoretically, be unchanged. If the company stays open, shareholders’ wealth may increase or decrease—not liquidating the company essentially becomes a roll of the dice.

Such a view is admittedly callous. Workers depend on the company staying open to continue collecting their salaries. Suppliers will lose business if the company closes and customers will be forced to find another vendor and either potentially pay higher prices or get a lower quality product, or both. However, the market is apathetic as to whether or not a business opens it doors tomorrow. Stocks are bought and sold for one reason—to make money. If the same amount of money can be made by liquidating the company as can be made by keeping the doors open, then where is the incentive to take the chance that the stock will be worth more tomorrow or the day after tomorrow? The market is essentially telling shareholders that the reward for keeping the company open is minimal.

In theory, shareholders should vote to liquidate any company below book value. In reality, however, a company may be worth more as a going concern than the value of its net assets. An existing company has a necessary organizational structure encompassing management, employees, accounting procedures, customers and suppliers. It has office equipment in place, such as desks, computers, phones and cabinets. It may also have machinery, tools and warehouse equipment. Intangible assets such as a brand name, a website address, a physical address and phone number(s) are established.

While this may all seem immaterial to a company’s worth, these intangibles are the essence of an ongoing corporation and, therefore, add value. For instance, suppose an (extremely wealthy) investor wanted to enter the soda business. He could buy an existing soda company or he could start up his own company. If he chose the latter, he would have to acquire office space, set up bottling facilities and establish a distribution system. In addition, he would have to hire employees, create a management structure, build a customer base and promote his company. None of these even accounts for mundane activities such as purchasing office supplies, paying bills or getting phone service established.

Creating a business from scratch takes a lot of work and a lot of money. Even after much effort and capital is put into the venture, most companies fail within their first few years of operation. The money invested in a failed corporation is not the only loss; there is also the opportunity cost of not having invested the money elsewhere. Opportunity costs compound monetary losses.

The opportunity cost of investing in an ongoing concern can be lower, particularly if a good management team is in place. An existing company has a physical structure (office space, furniture, copiers, etc.), an organizational structure (a chain of management, employees, etc.) and intangibles (branding, a recognizable address, etc.). It also has procedures for acquiring necessary supplies and lines of credit. Most importantly, an established company has paying customers, distribution systems and a method for bringing new products to market. Everything necessary for a company to function is already set up and operational.

Measuring Realized Return

A mathematical argument can also be made for why an ongoing concern should not sell for near or below book value. A profitable, well-managed company will generate a return on its assets. This profit can either be maintained as cash (increasing book value), invested in new projects (potentially creating a higher stream of earnings in the future) or given back to the shareholders (dividends or stock buybacks). In any of these scenarios, shareholders may benefit more by keeping the doors open than they would by liquidating the company.

This can be demonstrated by using the return-on-equity (ROE) ratio. Return on equity is proportionate profit generated off the company’s net assets. ROE is simply calculated as:

net income ÷ shareholder’s equity

For the purpose of presenting the mathematical argument against liquidation, let’s use a fictional company with a market capitalization (share price times number of outstanding shares) of $900 million and $1 billion in shareholder’s equity (total assets minus total liabilities). Shares of this company trade at a price-to-book multiple of 0.9 ($900 million ÷ $1 billion). During the past five years, the company has generated an average return on equity of 10%. For the sake of simplicity, we will also assume that net income has increased proportionately to the increase in shareholder’s equity.

If shareholders voted to liquidate the company, they stand to gain 11% on their investment. This would be a one-time gain of $100 million dollars spread among all shareholders, whose total investment, according to the market value of the company, is $900 million.

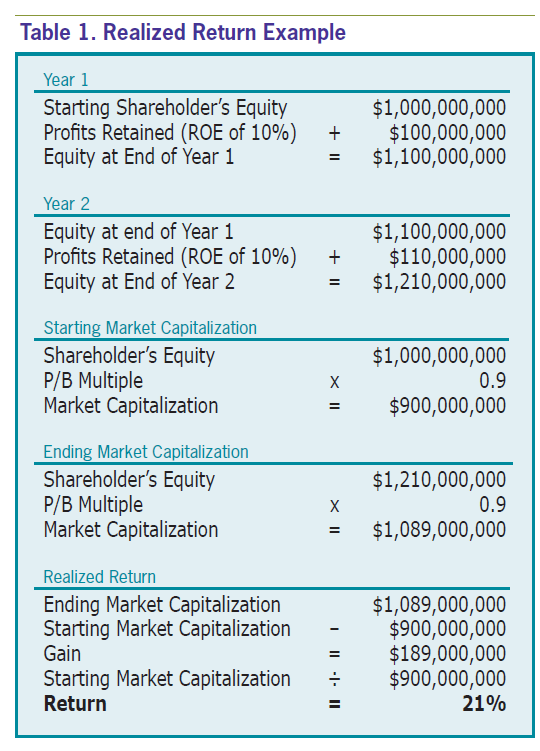

A return of 11% may seem pretty good, but if shareholders decide to roll the dice and assume that the company will continue to be profitable and generate 10% return on equity into the foreseeable future, the potential gains are even bigger. In fact, in about two years, shareholders can get nearly double the return even if the stock continues to trade at a price-to-book multiple of 0.9. Table 1 shows the calculations.

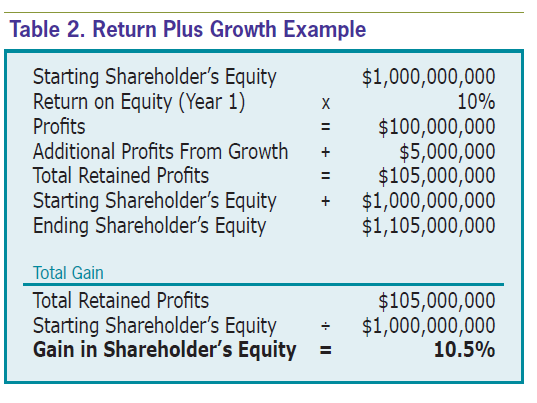

If just a modest increase in the rate of growth is assumed, the numbers turn even more in favor of maintaining the company as an ongoing concern. For instance, assume the same company is able to generate a 5% growth rate above the increase in its net assets, for a total growth rate of 15% over the next 12 months. We know that without any growth, the company would earn $100 million (ROE of 10% × shareholder’s equity of $1 billion). Factoring in the low amount of growth increases the profits up to $105 million. If all of the earnings are retained, shareholder’s equity at the end of 12 months increases to $1.105 billion—a gain of 10.5% (see Table 2).

A 10.5% gain may not sound very spectacular, but if the company continues to maintain this modest improvement in the rate of its growth, the numbers begin to compound very quickly. After just two years, the total return jumps to 27% (versus 21% without the increase in the growth rate). If all earnings are retained, shareholder’s equity jumps to $1.58 billion in five years. This equates to a nearly 60% increase.

I used very simplistic models to calculate the returns for both liquidating the company and maintaining it as a going concern. Therefore, while the numbers do show a mathematical argument against liquidation, there are a few factors that should be taken into consideration.

Liquidation, as I will soon explain, is not a simple process. The actual proceeds realized from the liquidation are often different than the numbers stated on the balance sheet. It is also a very difficult process and a nearly impossible one for an individual investor to initiate. Not to mention, there is the risk that any subsequent investment could produce a lower return than would be realized if the company were maintained as a going concern. (To be fair, it is possible that the subsequent investment could generate a higher return.)

As far as keeping the company as a going concern, we do not know for sure that management will increase shareholder’s equity in the years to come. Five years from now, the actual return realized by shareholders will probably be far different than the proposed 60% gain. The company could lose money, thereby lowering the amount of retained earnings. Management could make bad decisions on how to utilize the assets. The company could go bankrupt.

On the other hand, growth could be considerably stronger than expected. Management could choose to pay dividends to shareholders. The company could be acquired at a sizeable premium. The market could realize that the valuation is too low and bid the price of the shares up. It is impossible to say what the future holds.

In addition, we simply do not know how much the company will spend on new equipment, facility expansion or marketing campaigns. Anything affecting the company’s growth (e.g., the introduction of a blockbuster product) will affect the percentage of earnings actually retained from year to year. Because it is not possible to predict with any amount of accuracy how much a company will spend from year to year, forecasting future book value is largely a waste of time. Even when multiple scenarios are examined, the projected book value will probably be materially different from what the company actually reports.

The great thing about the price-to-book multiple is that it does not need to be used as a forecasting tool. Rather, the ratio should be used to determine one simple thing: Is the market adequately recognizing a company’s worth as an ongoing concern? A well-managed company trading at or near book value is too cheaply valued and therefore should be considered as a potential investment. (A rule of thumb for purchase is a price-to-book ratio of 2.0 or lower, though 1.25 or lower is even better.) A well-managed company trading at a significant premium to book value (price-to-book ratio of greater than 4.0) should be watched, but is only suitable for speculative trading until the valuation becomes reasonable. A company that is not well managed should never be purchased for any reason.

If a company has superb management, a great business model and fiscal strength, but trades at a book value of 2.25, it should be considered for purchase. Is it a better value at a price-to-book ratio of 1.25? Absolutely, but if the company is that well managed, then it should be trading at a premium valuation anyway. It is always better to pay slightly more for a great company than slightly less for a subpar company. Never pay a high premium for a stock, but do not pass on a great quality company just because its valuation is slightly above what you would like to pay.

Put another way, what matters is whether the purchase price represents a reasonable discount. If management is capable of creating shareholder value in the future and the current price does not reflect this fact, then the stock is a good value. If management is suspect and the current price reflects too much optimism about the company’s prospects, then the stock is overvalued. The best way to determine whether the stock is undervalued relative to its prospects is book value. Great companies are always worth considerably more than the underlying value of their assets. Similarly, poorly managed companies and those with bad business models deserve to trade at valuations equivalent to the value of their assets because their future is uncertain.

The Other Side of Book Value: Liquidation

Suppose a company is poorly managed and is trading below book value: Does it have appeal simply because the price is so low? There are two ways to look at this situation.

The first is to assume that the company does have worth as an ongoing concern and simply needs new management. Effecting a change of management is difficult, especially because it requires a majority (or a supermajority) vote by shareholders. Furthermore, if the board members fail to recognize that current management is a failure, it begs the question: How likely are they to find a highly competent CEO to effect change?

A competitor could acquire the company, but waiting for an acquisition to occur is a fool’s game. Without controlling a majority of shares, individual shareholders cannot push management to seek a buyer. Furthermore, a potential buyer may not want to pay a premium over the current price. Even after an acquisition has been announced, there is no guarantee that the merger will be completed. It is not unheard of for a potential merger to be called off.

The second alternative is liquidation: Sell all the assets, pay off all of the debts and give the remaining money back to the shareholders. In theory, this should generate a positive return.

If this concept were to hold true in reality, then the smartest investment strategy would be to buy poorly managed companies trading below book value and liquidate them. Returns would be nearly guaranteed. Calculating profit would boil down to simple arithmetic: Book value less market capitalization equals profit. It would make little sense to invest in any company worth more than its book value.

Unfortunately, life and investing are never quite that easy. If making money boiled down to simply buying poorly managed companies trading below book value and liquidating them, everyone would be doing it. The unintended effect, however, would be that valuations would be pushed closer and closer to book value, thus limiting profit. More dollars chasing after the same stock would boost the price. Blame it on the law of supply and demand.

Another obstacle is corporate charters. Approval by the majority or even a super-majority of shareholders is required for liquidation to occur. Clearing such a hurdle means seeking the consent of large shareholders and, possibly, many small shareholders. There would also be potential lawsuits filed by dissident shareholders, new hurdles created by corporate executives and objections from unions and debt holders. Depending on the level and intensity of the objections, achieving approval of liquidation could be a very lengthy and costly process.

There is also the potential problem that the actual amount of cash generated by the sale of a company’s assets and the payment of all debts will differ materially from the recorded book value. Under a liquidation scenario, buyers will pay as little as possible for the assets. New payables would arise, such as accounting fees. Penalties for breaking leases and contracts could be assessed. Legal costs would present themselves, including the possibility of lawsuits by dissident shareholder groups.

The asset side is just as messy. The recorded value of assets often is disconnected from the price a willing buyer would pay. For instance, office furniture may be fully depreciated, but still have value. Inventory could be worthless— especially specialized parts—or could sell for considerably less than purchase price. Certain customers, knowing that the company is being liquidated, could attempt to avoid paying invoices, thus making receivables worth less. Intangible items might command a dollar value completely unrelated to what is listed on the balance sheet.

Inexact, But Good

Remember, valuation is not an exact science. Book value is merely an accounting number, influenced by tax laws and management.

Fortunately, book value does not have to perfectly measure the underlying value of a company’s assets to be a highly effective tool for selecting stocks. Rather, it works because a profitable, well-managed concern is effectively using its assets to make money. The desks, the machines, the patents, and even the website address are worth more than their face value because, combined, they can increase shareholder’s net worth. A company worth owning should be worth more than its book value.

This article is excerpted from Charles Rotblut’s book, "Better Good Than Lucky: How Savvy Investors Create Fortune With the Risk-Reward Ratio" (W&A Publishing 2010).

Cyril from NC posted over 14 years ago:

Charles from IL posted over 14 years ago:

Richard from OH posted over 14 years ago:

Richard from OH posted over 14 years ago:

Daniel from AL posted over 14 years ago:

Andrew from Italy posted over 14 years ago:

Fernando from FL posted over 14 years ago:

Charles from IL posted over 14 years ago:

Ed from WA posted over 14 years ago:

Vern from CA posted over 14 years ago:

Charles from IL posted over 14 years ago:

Alan from PA posted over 14 years ago:

Jeffrey Hayes from CO posted over 13 years ago:

Charles Rotblut from IL posted over 13 years ago:

Bruce from ON posted over 12 years ago:

Bruce from ON posted over 12 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account