Simple, safe and stable: These are the three tenets of the Permanent Portfolio, a strategy invented by the late Harry Browne to help investors grow and protect their life savings no matter what was going on in the markets.

Over the last 40 years, the strategy has returned 9.5% compound annual growth. The worst loss, a drop of 5%, occurred in 1981. In 2008’s financial crisis, the portfolio was down only around 2% for the year. We think that’s pretty impressive for a strategy that appears so startlingly simple on the face of it.

The Basics

The basic premise of the Permanent Portfolio is this: The economy is always transitioning between four states. If you own an asset that can deal with each of those states, you will achieve powerful diversification. Harry Browne identified those states as:

- prosperity,

- deflation,

- recession and

- inflation.

What assets and allocations are best to deal with these economic states? Simply:

- 25% stocks (prosperity)

- 25% bonds (deflation)

- 25% cash (recession)

- 25% gold (inflation)

You buy these assets all at once and hold them at all times. While the Permanent Portfolio is simple, it is not simplistic. It actually reflects a sophisticated understanding of economics. Let’s explore this.

A Passive Approach

The Permanent Portfolio does not time the market and is completely passive. There is no need to analyze charts, follow market gurus, track moving averages or anything of the sort. This is a good thing because we’ve never seen any of those methods work reliably anyway. Adopting a strategy that treats the future as uncertain and deals with it realistically best serves investors. The net result is not only a portfolio that has low turnover (which means lower taxes), but also has very low volatility, which means lower chance of catastrophic losses (and stress).

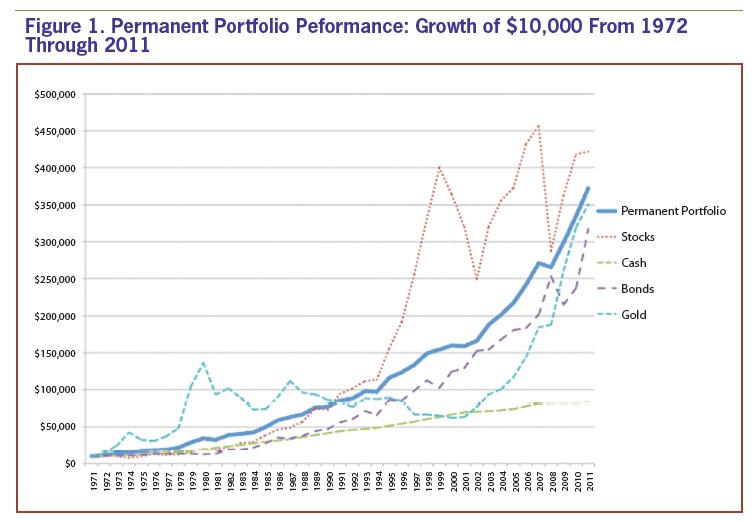

Figure 1 shows the performance of the portfolio from 1972–2011. Notice that the swings in assets individually had little impact on overall portfolio volatility each year.

Why It Works

Let’s talk about the four economic environments to understand how the diversification works.

Prosperity: Good for stocks

Prosperity is good for stocks as the economy is firing on all cylinders. During this time, it is not unusual to see double-digit gains in this asset. Indeed, owning the stock market is the best way to take advantage of the power of companies to innovate and produce wealth. The 1980s and 1990s showed the power of the U.S. stock market, as average returns were well over 10% a year (and closer to 15% in many cases). An investor who didn’t have stock exposure during those years missed huge profits.

Yet, the stock market can also encounter extended periods of very poor returns. The 2008 crash caused a nearly 40% decline, capping off a very bad decade of the 2000s. With high inflation, stocks can also have a hard time keeping up. This happened in the 1970s, where stocks had a decade-plus of negative real returns after inflation took its share.

Deflation: Good for bonds

We define deflation as a situation where market interest rates are falling steeply. Usually this is the result of fallout of a credit-fueled asset bubble, such as the real estate collapse in 2008 or the Great Depression of the 1930s. Falling interest rates are very good for high-quality U.S. Treasury long-term bonds. In 2008, the overall market was down almost 40%, but Treasury long-term bonds were up almost 30%.

The Achilles heel for bonds is high inflation and rising interest rates. These two things erode purchasing power and cause the price of bonds to fall as investors seek out higher yields to compensate. Just like with stocks, the high inflation of the 1970s eroded purchasing power of bonds. A dollar in the early 1970s was worth about half as much by the end of the decade. So investors relying on bond income alone to support themselves found their standard of living severely impacted.

Recession: Good for cash

A recession, in the Permanent Portfolio sense, is a sharp deliberate raising of interest rates by the Federal Reserve in an attempt to stop inflation. Last time this happened was in 1981, when then–Fed Chairman Paul Volcker enacted policies to bring the prime rate above 21%. In this condition, no asset really does well, but cash can act as a buffer while things settle out. Cash in the portfolio also is useful for emergency expenses and opportunistic rebalancing as the other asset classes are swinging in value. Cash also is a great diversifier emotionally because no matter what your portfolio is doing, you always have a stable anchor to tap if you need it.

As with bonds, though, high inflation is not a good thing for cash. While the asset can usually tread water as interest rates rise, the reality is that cash simply won’t generate a high enough rate of return to reliably beat high inflation. In many cases, cash can lag inflation each year and result in negative real returns.

Inflation: Good for gold

Gold is the most controversial asset in the Permanent Portfolio. People either love it or hate it. We try not to create a conviction for this asset because it’s just a tool for our purposes.

The fact is that gold provides strong diversification against the inflation risks inherent in stocks and bonds. Inflation in this sense can be the double-digit mess we had in the 1970s that eroded wealth over a decade. Or it could be the malaise of the 2000s with anemic stock returns but constant inflation, resulting in zero real returns for many investors. Yet over these same periods, gold turned in great returns that could be harvested and used to grow wealth. History provides clear lessons on why we think owning gold in a portfolio is a good idea.

Gold’s weakness, though, is that in a prosperous market investors simply won’t want to own it. If confidence in the dollar is sound because the economy is booming, investors will see no use for gold and its price will fall. Also, in a deflationary market, it could be the case that a rising dollar can make the price of gold go down as well.

The lesson?

While in hindsight many think they can predict the markets, the reality is that we simply don’t know what will happen. Narratives such as “gold is in a bubble,” “stocks are the best asset for the long run” and “rates on bonds can’t go any lower” have nothing to do with how markets actually perform. The truth is that no one knows.

Against this backdrop of uncertainty, what is the fate of the Permanent Portfolio investor who holds all four asset classes? Well, since he has nothing riding on any particular market prediction and has placed no bet on any particular outcome, he is ready for whatever economic conditions happen to show up. The bonus is that he also enjoys peace of mind because there is nothing the market can do that he isn’t already prepared to handle.

The Assets

The Permanent Portfolio holds four core assets:

25% Stocks: A broad U.S. stock market index such as one of the Dow Jones Total Stock Market (TSM) indexes or an S&P 500 index. Why? Because indexing will beat virtually all actively managed stock trading strategies over time.

25% Bonds: 100% U.S. Treasury long-term bonds with maturities between 20 and 30 years. U.S. Treasury long-term bonds are regarded as default-free and the safest to own for U.S. investors. The U.S. government can always tax or print money to pay bondholders (many other bond issuers can’t do both). This means when the markets are behaving very badly, the safety of the U.S. Treasury bond will dominate. It will be the last man standing.

25% Cash: 100% U.S. Treasury bills are the safest way to hold cash. They do not have credit risk, default risk, FDIC insurance risk or other risks that bank certificates of deposits (CDs), corporate bonds and even municipal bonds have. They are also the most liquid investment you can hold. In a market panic you’ll always be able to access your cash. Don’t discount this feature: In 2008, some prominent non-Treasury money market funds froze redemptions and even lost significant value.

25% Gold: Physical gold bullion stored securely in a custodian account at a bank in your name. As a form of money, gold is often used in the markets when the U.S. dollar is having problems. Note that the portfolio holds gold bullion, not gold mining stocks. There is a difference in that gold bullion is not affected by the same impacts that could influence gold mining companies. For extra safety, this asset can also be held outside the country where you live for geographic diversification against political impacts, or natural and manmade disasters that affect the markets. Exchange-traded funds (ETFs) can be used, but they are not as safe as custodial accounts in the event of a serious currency crisis.

Implementation

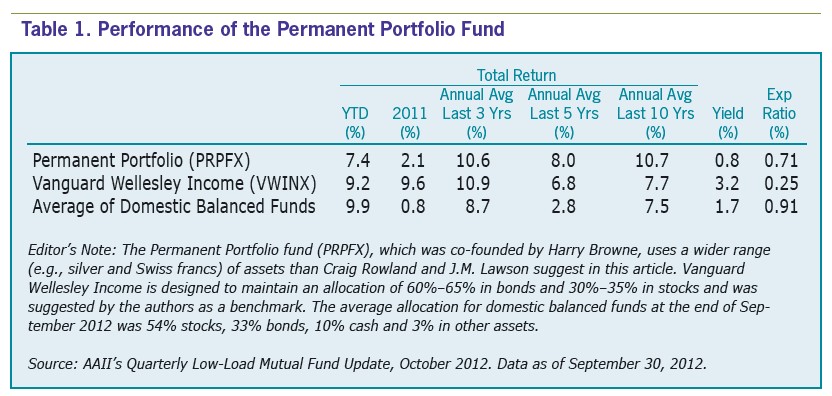

Implementing the strategy can range from very simple to more involved. At the simplest, there are two funds available that implement the basic ideas. The first is a mutual fund called the Permanent Portfolio fund ![]() (PRPFX), which has been in existence since the early 1980s. It implements an earlier version of the strategy, but has robust moderate growth. In 2012, a new exchange-traded fund from Global X also showed up, called the Permanent ETF (PERM). This new fund sticks more to the 25% allocation split and trades for a lower cost than PRPFX. Performance figures for PRPFX are shown in Table 1, along with a comparison fund and the average performance for balanced domestic funds.

(PRPFX), which has been in existence since the early 1980s. It implements an earlier version of the strategy, but has robust moderate growth. In 2012, a new exchange-traded fund from Global X also showed up, called the Permanent ETF (PERM). This new fund sticks more to the 25% allocation split and trades for a lower cost than PRPFX. Performance figures for PRPFX are shown in Table 1, along with a comparison fund and the average performance for balanced domestic funds.

While funds offer convenience, they do expose you to manager risk. This is the risk that the managers of the fund could do things to impact performance through their decisions. This isn’t a unique risk to these funds; it’s a risk to any managed fund. This is primarily why we recommend building your own portfolio if you are able so that you have more control.

There are easy ways to implement the portfolio, and more complicated ways to do it; all are explained in our book with the rationales. Consider the following simple example, which could be implemented mostly with Vanguard funds:

-

25% stocks: Vanguard Total Stock Market fund

(VTSMX);

(VTSMX); - 25% bonds: Vanguard Treasury Long-Term Bond fund (VUSTX);

-

25% cash: Vanguard Treasury Money Market fund (VUSXX), which is closed to new investors right now, or Vanguard Short-Term Treasury fund (VFISX) as a backup option; and

- 25% gold: A gold ETF, such as Central Gold Trust of Canada (GTU).

Note: Gold ETF options are for convenience, not safety. We cover some more preferred ways to hold gold in our book (even overseas). Do not use a precious metals and mining fund, such as the Vanguard Precious Metals and Mining fund ![]() (VGPMX). This asset must be physical gold bullion and not stocks of mining companies.

(VGPMX). This asset must be physical gold bullion and not stocks of mining companies.

Implement and rebalance

Take your funds and put 25% into the four assets above. When an asset rises to 35% or more, sell your position in it down to 25% of your portfolio’s value and use the profits to buy more of your under-allocated assets. If an asset falls to 15% or less, use profits from your winning assets to bring the allocation for the underperforming asset back up to 25%.

This rebalancing process not only can boost returns over time, but also provides strong protection from any one asset causing a serious loss if the market should turn south.

A firewall for your life savings

By splitting your life savings into four equal parts, you get an additional benefit as well: A firewall for your life savings. The split reduces the chance that a large market loss in any asset will be catastrophic. With 25% in stocks for instance, a crash in the market of –50% tomorrow means the largest impact you’ll have would be –12.5%. And that’s assuming no other asset goes up in price to offset the losses (which would be unusual). This is how the strategy provides protection against “Black Swan”–type market events.

Risks and Rewards

The portfolio’s assets largely offset each other’s risks and that’s what allows it to ride out very volatile markets. Over time, a big loss in one asset tends to be overcome by big gains in another. In fact, since a falling asset can’t lose more than 100% in value (and realistically rarely loses more than 50%, even in the worst markets) and a rising asset can easily see long-term gains of 100%, 200%, 300% or more, over time the overall portfolio tends to gradually drift higher. This doesn’t mean the portfolio can’t experience a loss over the short term, just that over time the results have historically tended to be upward, as shown in Figure 1.

Ironically, the primary risk to the portfolio is the investor himself (as it usually is). Three of the four assets are very volatile when you look at them individually (stocks, bonds and gold). It can be hard to watch a big drop in stocks, even though your bonds may have gone up and offset the decline in stock prices. Likewise, a sudden drop in gold can cause some people to get upset, even though the stock allocation may have risen enough to negate the losses. Furthermore, it is the hard-to-shake feeling you can predict the future and adjust the allocation based on your gut feeling that can cause lots of problems.

This is why we encourage investors never to look at assets in isolation. Only total portfolio value matters. If an asset has fallen by 20% in a year, but the total portfolio value has risen by 8%, does the decline in one asset really matter? No, it doesn’t. And since you can’t predict what asset will do best ahead of time, the constant exposure to all of them ensures you’ll always own a winner no matter what is going on. Further, the Permanent Portfolio only works as a package. If you tinker with the assets or do not own them at all times, you can seriously compromise the safety the Permanent Portfolio is intended to offer.

ED from NJ posted over 13 years ago:

Charlie Troell from TX posted over 13 years ago:

Edward Spitzer from PA posted over 13 years ago:

Robert Gilleski from GA posted over 13 years ago:

Edward Reifsnyder from CO posted over 13 years ago:

John from TX posted over 13 years ago:

Hemendra Parikh from IN posted over 13 years ago:

Ramesh Patel from OH posted over 13 years ago:

Bob from MA posted over 13 years ago:

Thomas Pruitt from CA posted over 13 years ago:

William from FL posted over 13 years ago:

William from FL posted over 13 years ago:

John from TX posted over 13 years ago:

Patrick Roszel from KS posted over 13 years ago:

Carmen Putrino from CA posted over 13 years ago:

Richard Paul from CT posted over 13 years ago:

Leamon Lorance from IN posted over 13 years ago:

James Moule from CA posted over 13 years ago:

John Heryer from MO posted over 13 years ago:

John Heryer from MO posted over 13 years ago:

Albert Meyer from NY posted over 13 years ago:

Wilford Poe from FL posted over 13 years ago:

Douglas Kuntzelman from OK posted over 13 years ago:

Elliot Cohen from PA posted over 13 years ago:

Albert Meyer from NY posted over 13 years ago:

Donald Goldmacher from CA posted over 13 years ago:

William Kloss from FL posted over 13 years ago:

Wayne Smith from OR posted over 12 years ago:

EdwardjK from NJ posted over 12 years ago:

rsmCanuck from CA posted over 12 years ago:

Aaron Cook from CA posted over 7 years ago:

Chris from Vermont posted over 7 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account