Charles Rotblut leads a class in AAII's new Essential Investing Video Course. Go to https://www.aaii.com/ves for more information and to subscribe.

Michael Mauboussin is head of Global Financial Strategies at Credit Suisse and the author of several books, including “The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing (Harvard Business Review Press, 2012). He and I spoke about the role skill and luck play in investing.

—Charles Rotblut

Charles Rotblut (CR): A big theme in your recent book is the distinction between skill and luck. Could you explain what the difference between the two is?

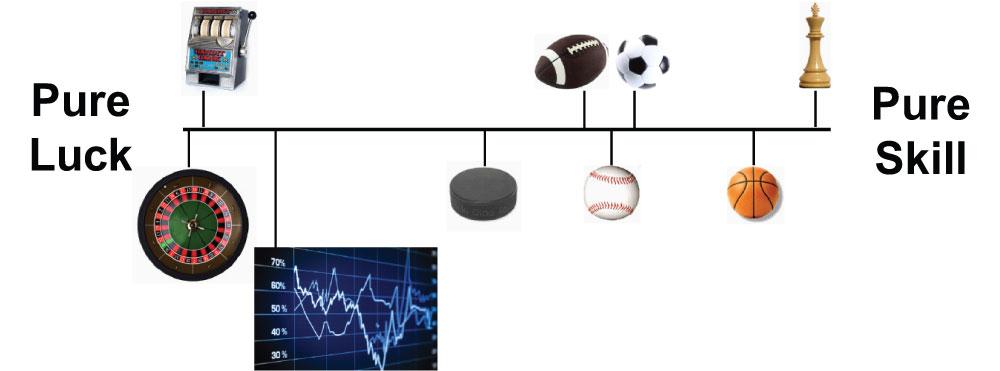

Michael Mauboussin (MM): One of the ways I like to think about this is as a continuum of activities from pure luck and no skill on one end to pure skill and no luck on the other end [Figure 1]. Obviously, most things reside somewhere between the extremes, and where an activity sits can be very important. But before we get going, it is important to define the terms.

I’m going to define skill right out of the dictionary: The ability to apply one’s knowledge readily in execution or performance. You know how to do something, and when you’re asked to do it, you can do it effectively.

Luck is much more difficult to define. It actually spills into moral philosophy pretty quickly. I’m going to say that luck exists when three conditions are in place. Number one, it operates on an individual or an organizational basis, such as you or your team or company. Second, it could be good or bad. By that, I don’t mean to suggest that it is symmetrical, as in it could be equally good or bad. But rather there is a plus sign or a minus sign. The third thing is that it is reasonable to expect that a different outcome could have occurred. If those three things apply, then you’re in a situation where luck exists.

Not surprisingly, when you look out into the world, whether it’s business, investing or your favorite sports team, both skill and luck are contributing. The real question is, in what proportion?

CR: Do you think investors confuse the two when looking at their own performance, in that they think they are skillful when they have actually gotten lucky?

MM: There is actually a very interesting test to determine if there is any skill in an activity, and that is to ask if you can lose on purpose. If you can lose on purpose, then there is some sort of skill. Investing is very interesting because it is difficult to build a portfolio that does a lot better than the benchmark. But it is also actually very hard, given the parameters, to build a portfolio that does a lot worse than the benchmark. What that tells you is that investing is pretty far over to the luck side of the continuum. That is the first important thing.

The second thing is that luck is a very difficult thing for us to deal with psychologically. The main reason has to do with a part of your brain in the left hemisphere. If you give it any effect, it will immediately and effortlessly come up with a cause. That part of your brain knows nothing about luck. It only knows about causality. So it attaches skill to positive outcomes and it attaches lack of skill or maybe bad luck to poor or negative outcomes. So there is this kind of disconnect between what happens in the real world and how our mind interprets those events. And to your question, we tend to associate good outcomes with good skill alone and that’s often simply not the case. And bad outcomes are not necessarily associated with bad skill either. It’s a very tricky relationship to understand clearly.

CR: If someone is following a set process of picking stocks or bonds and it doesn’t do well, is this a case where the investor should look at how the strategy has performed in the past and if it has worked well, just attribute the poor performance to luck turning against them?

MM: For sure. Part of what I talk about in the latter part of the book is how to improve one’s skill. What I argue is that when you’re on the skill side of the continuum, your output and your skill are very closely related to one another. If I want to know if you’re a good violin player or a good tennis player, I can listen to you or watch you play and I can tell quite quickly. When you move over to the luck side, it becomes process-oriented and probabilistic. For example, there is a standard strategy for blackjack. You may play your cards properly and lose the hand, which is just bad luck, or you may play your cards foolishly and win the hand. So the connection between the quality of your skill and the outcome is broken. There, you really have to focus on process.

How do I know if my process is any good? Number one, has it worked in the past and is it economically sound? Number two, I think of good processes as having three essential elements. Element one is analytical: having an ability to find situations in which you believe something the world doesn’t believe and in which you have a good foundation for such a belief. The second is behavioral: we are all subject to behavioral mistakes and cognitive biases. Are you aware of those things and are you taking steps to manage or mitigate them? The third, which is less true for individuals and truer for organizations, is what I call institutional. This element relates to the constraints in your personal or professional life that don’t allow you to do the best thing possible in terms of your process. If you have a good analytical process, are aware of behavioral issues and organizational issues are not a problem, then you typically can develop a pretty effective process. If you’ve done that and you get a bad outcome in the short term, you pick yourself up, dust yourself off and you go back at it the next day because over time the process will lead to success.

CR: What about for investors who haven’t really thought about whether their strategies have worked in the past? How do they go about seeing if their strategies make sense?

MM: Those three points I just mentioned—analytical, behavioral and institutional—might be a guideline in thinking about whether your approach makes sense in the first place.

Certainly, you can think about what has worked in the past. For instance, over long periods of time, value investing has worked reasonably well, and that is buying things with low expectations and holding them for a longer period of time. That would probably be a good thing to think about.

The other thing is to just realize that investing is a difficult task. If you’re not inclined to do a lot of work on individual stocks or don’t think you have a high probability of having some sort of edge, that’s where the classic advice to buy mutual funds or index funds that are properly diversified may be your best bet. You are well-positioned, but you don’t have to worry about how good your process is for individual securities.

CR: Going back to luck versus skill, what about in the case of corporate earnings? How much of growth and good earnings is due to luck and how much is due to the skill of a good CEO?

MM: There has been some very interesting recent research on this. As you know, a lot of books have been written about success: Jim Collins’ “Built to Last” (HarperBusiness, 2002) and “Good to Great” (HarperBusiness, 2001), Peters and Waterman’s “In Search of Excellence” (HarperBusiness, 2006) and so forth. And it turns out, you have to be very careful in those types of studies. The typical approach is to identify success and then go backward to figure out what attributes are associated with that success. But the question is not, for example, whether successful companies are “hedgehogs” [Collins’ label for firms that concentrate on doing one thing well]. Rather, the question is, are all hedgehogs successful? That is a very different question.

I think all of that research on success is actually fundamentally quite flawed. It turns out that there have been some researchers who have analyzed the studies quite carefully, and what they’ve found is that if you take the top, say, dozen studies of successful companies, they can only confidently code about 10% to 15% of the companies mentioned as truly skillful. The rest are there by luck. Even in corporate performance, there is an enormous amount of luck. That said, as an investor, the key thing to differentiate or think about is distinguishing between the fundamentals of the business and the expectations built into the price. Those are really two separate things.

The clearest metaphor is the race track. You go to the race track and there are odds on the tote board. Those odds reflect the probability that the horse will win the race. The fundamentals are how fast the horse will actually run. Now if the odds reflect the horse’s abilities, it’s not an interesting bet, right? What you are looking for are misprices between the tote board and the fundamentals of the horse.

It’s the exact same thing with investing. What you’re looking for are not necessarily the best companies or the worst companies. You’re looking for mispriced companies. So a distinction between expectations and fundamentals would also be the root or core of any quality process.

CR: You’re looking for a stock that looks like a bargain relative to its valuation as well as relative to its past performance and future expectations?

MM: I would say it’s less about past performance and more about future expectations. You’re looking for a stock where the expectations for financial performance—sales growth rate, profit growth rate and so forth—are relatively modest vis-à-vis what your analysis has shown to be achievable. I mean, it’s easily said and difficult to do, but that is what it is all about.

CR: Would you say that the PEG (price-earnings to earnings growth) ratio would be a good measure for that?

MM: I have never liked PEG ratio, and there are a lot of different reasons for that. I should back up and say that I think there are a lot of shortcomings with price-earnings multiples and problems with earnings to start. The primary issue with earnings is that there is no reckoning for how much capital a company needs to invest in order to generate the earnings.

You might think of Company A, which invests $1.00 to earn $0.10, and Company B, which invests $2.00 to earn $0.10. In this example, you know that Company A is better than Company B, but the earnings number itself, the $0.10, doesn’t really reveal that. That is one issue. It turns out that the growth component is good only when you’re earning high returns on capital. But it can be bad if you’re earning low returns or indifferent when you are earning basically your cost of capital.

The PEG ratio doesn’t really capture that very effectively. Growth can be good, bad or indifferent, and a single number like that has a lot of shortcomings in capturing that. What I would advocate for, which may be beyond the scope of many investors, is to really lay out a stream of cash flows and to try to understand the present value of those cash flows. It is a more involved process and less reliant on rules of thumb or heuristics. But it ultimately gives you more insight into where expectations and mismatches lie.

CR: You brought up the Sony MiniDisc in your book, highlighting it as an example of a good product that had terrible timing for reasons beyond Sony’s control. Was this just a case of bad luck or is there something from that occurrence that investors can think about to avoid when looking at a company?

MM: This is a really important issue, and it is a difficult mindset when you get involved in business and investing. In a sense, everything is somewhat probabilistic. There is very little you can say for certain.

The MiniDisc example, which I learned from a researcher named Michael Raynor, is a great one. Sony had a lot of wonderful products—the Walkman, their well-known televisions—and then they had some flops. They learned from both their successes and failures. And then they came out with the MiniDisc, which at the time was considered to be kind of a brilliantly conceived and strategically excellent product. A lot of the mistakes they had made they corrected.

But, whenever you’re in business, you always face three inherent uncertainties. One is what do your customers want? And their desires can shift based on what is going on in the world. Second is what are your competitors going to do? You like to think about what they’re going to do, but you don’t really know what they’re going to do. The third is technological change.

As you pointed out with the MiniDisc, all three things went badly for Sony. Hence, this thing that was very promising and certainly well-conceived ended up flopping. So, that’s the thing: When it’s probabilistic, you have to focus on process and you have to recognize going in that even if you’re doing your work properly, some percentage of the time you’re going to fail, just by the nature of probabilities.

There is also a flip side, where you could be doing a bad job and succeed. This may falsely embolden you to where you think what you’re doing is actually sensible. People often say that you don’t want the first stock you buy to go up because then for the rest of your life you think you know what you’re doing. In investing, business and other things—such as managing a sports team where you’re hiring and firing players—there should always be this sense of humility or recognition that it’s all inherently probabilistic. There really are no certainties.

CR: What about in terms of mutual fund performance? If an investor is looking at a mutual fund manager who’s had a good run the past few years, is there any way to determine whether it was luck or skill?

MM: It is very difficult. Let me first say that you can’t focus on the outcomes, like my example of a top tennis player, where outcomes are almost a pure indicator of skill. That’s not true for investing, so you have to focus on process.

If you look at how investors actually behave, they tend to dwell heavily on past outcomes. In fact, people tend to buy what has done well and sell what has done poorly. This actually causes a lot of slippage, where investors tend to buy something that has done well right before it stops doing well and sell what has done poorly right before it improves. If you’re very motivated, I would say try to set aside recent outcomes, if possible, and to the best of your ability focus on process.

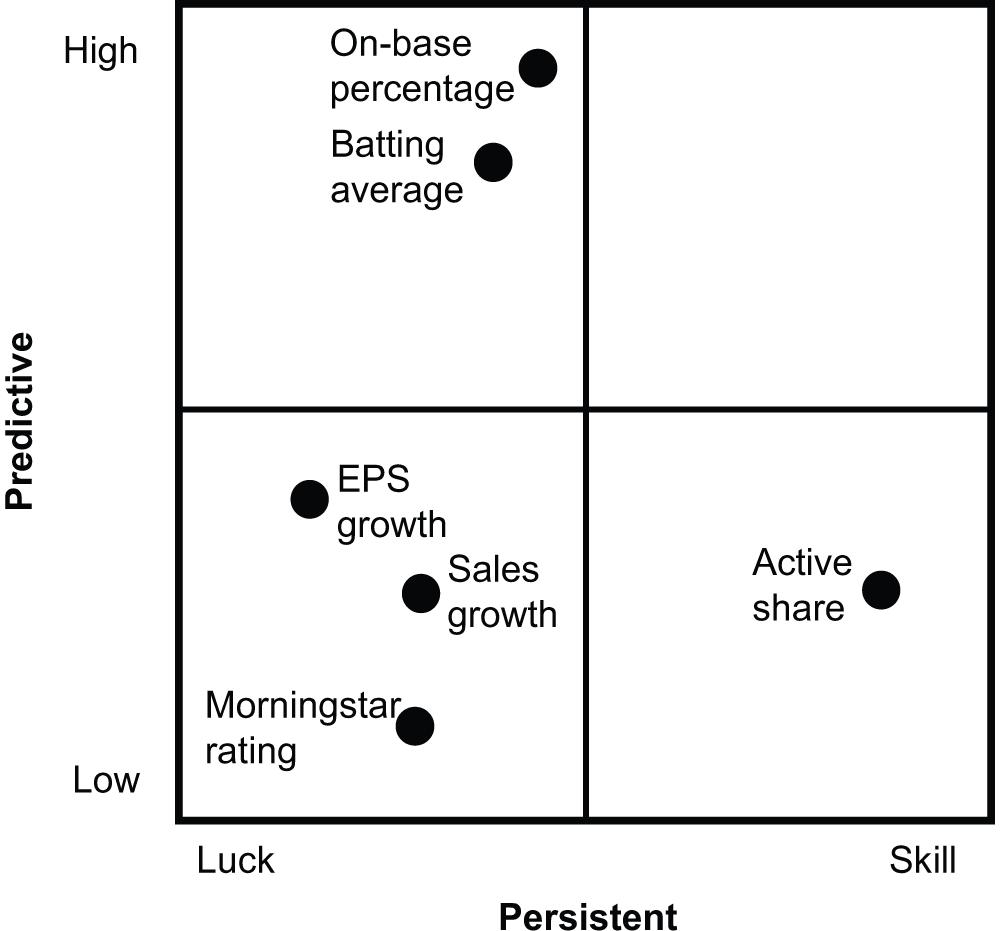

There are some measures, for example, that you can access through databases and so forth that may give you a glimpse into process. One would certainly be looking at things like fees. Another thing would be to look at a measure called active share, which is basically how much stockpicking a portfolio manager is actually doing versus just mimicking the benchmark, for instance. So there are some ways for motivated investors to get a better grasp of the process. And I would say focusing too much on outcomes typically leads to poor results.

CR: In terms of process, in the book you mention having checklists. You use the example of a doctor who tried to change surgical outcomes. If an investor were to create a checklist about what they should follow and what they should be doing, what would be on their list to make sure their process is good?

MM: I think that is hard to answer because it is probably different for every individual investor. That said, there are certain principles, which I follow myself, that are important.

The notion of diversification is still a very significant concept. I know that people have been a little spooked by all of the events surrounding the financial crisis. But over long periods, diversification is a very important concept.

Another one is making sure you’re getting what you’re paying for. You want to pay professionals for the services they provide, but you want to make sure those fees are reasonable.

A third thing that is important is something Warren Buffett calls the circle of competence: Stay within what you know you can do and avoid things that you don’t know much about. I think when we see others succeed wildly with something, we are tempted to wade a bit beyond what we’re comfortable with. And that typically doesn’t work out very well.

And then if you’re talking about the specific process, I’ll just go back to being a broken record and repeat the three key things again: make sure you have an analytical focus, understand the behavioral issues, and understand the organizational issues.

CR: What about trying to deal with reversion to the mean? Bond yields are a great example right now, where bond prices have stayed at or near historically high levels. How does someone cope with that, in that they know something is being overvalued and it is staying with a high valuation?

MM: Reversion to the mean in statistics actually has a very technical definition. I should first say that any time there is luck in a situation, there is reversion to the mean. So that’s an important thing to just get out of the way. If there is luck, which includes almost everything in life, there is reversion to the mean. What reversion to the mean says is that for outcomes that are far from the average, the expected value of the next outcome is something closer to the average. It doesn’t mean that it is going to go all the way back, but it does mean it should move closer to the average.

Now, this is something that is very important for picking mutual funds, such as the example you mentioned where a mutual fund has been doing very well for a few years. What does reversion to the mean tell us? It says that if there is an outcome far from average, the expected value of the next outcome is closer to the average. It does not mean that it’s going to be average, but rather that that is the rough direction it will move in. So, this means avoiding hot things—those that have done very, very well—or scaling them back. And recognize that things that have done poorly are likely to not do as poorly, even if they may not necessarily do well. I think that is important to think about.

The other key question is reversion to what mean? What is average? And to your point about bonds: The central banks around the world, with this consistent quantitative easing, in a sense they are creating an artificial mean, an artificial level of asset prices. Now we have to become tea-leaf readers as to when the government is going to scale those programs back. That becomes a very difficult task. But I think everybody would agree that if left to the market’s devices, it’s unlikely the current yield, for example, on U.S. Treasuries or many sovereign debt yields, would be where they are today. They would likely be something higher. It would be more a question of when that occurs rather than if it occurs. But it is a very difficult thing to predict accurately.

CR: If someone is looking at their allocation models, should they be thinking about what has been working in the long term and just stick to bonds or should they think about adjusting it?

MM: I would take two things into consideration. First, what has done well over time? Second, from what point are we starting? For the former, bonds have been doing great for 30 years and equities have been okay for 30 years, but the starting points are very troubling. It is very difficult to envision a scenario where for the next 20 or 30 years bonds do extraordinarily well. It is hard to see how that scenario unfolds. There are many scenarios where they don’t deliver particularly good returns at all. So that is something that has to color your analysis to some degree. Stocks are a little bit trickier. By some measures stocks are fairly valued, and by others I think they are undervalued, but certainly not to the degree of onus to the initial valuation of the stock market as we see in the bond market. I would think about long-term returns, but I would probably shade it or color it based on our initial points with much more concern on fixed-income land versus equity land.

CR: When you look at the market, what indicators do you pay attention to? What indicators do you suggest investors look at?

MM: The ones we look at are probably a little fancier than what most people have access to. I do look at the level of the equity risk premium, for instance. The expected return for the equity market is typically a combination of the risk-free rate, which is usually the 10-year U.S. Treasury note yield, plus an equity risk premium. So, with the 10-year note at about 2.25% today [early June 2013], and the equity premium by some reckonings about 5.5%, let’s call that 7.75% for the expected return of the market. I like to look at that equity risk premium, and especially the ratio of the expected risk premium to the risk-free rate. And that’s actually at very high levels, vis-à-vis history. So that tells you that equities are relatively attractive compared to bonds. So that would be one measure.

Another measure we look at is the present value of future value creation. It’s a fancy way of saying that when you buy a stock, part of the value is reflected in the operations that they have today and part of it is future value they are going to create. For example, McDonald’s has a certain number of restaurants in the world today, so that would be sort of the steady-state value of those profits. And the second part may be what future restaurants will be built that we know will be good restaurants. And that is also a ratio. Historically, about two-thirds of the value of the stock market has been the steady state and about one-third is paying for the future. Now, we are paying about 10% or 15% of today’s market value for future value creation. That’s a relatively low ratio.

We also look at levels of economic returns—return on equity, return on capital, that sort of thing—which in America are actually pretty good. By some of those metrics, things are quite healthy.

The average investor is probably going to look at things like price-earnings ratios; as a very rough measure it can be okay but, again, tricky for the reasons we talked about before. The issue is that we don’t really know if growth is embedded and we don’t really know what capital needs are embedded. As a shorthand, price-earnings ratios are not bad, but must be used with caution.

CR: Is there any economic data you pay attention to?

MM: Probably similar to what everyone else looks at, like basic GDP [gross domestic product] data. I certainly look at national income accounts, how the government is reporting aggregate profits, those kinds of things. Besides that, I don’t pay attention to a lot of economic reports.

CR: Is there anything from your personal process that you do to guard against your own mistakes?

MM: I’m a pretty textbook guy, actually. For my own portfolio, it is fairly diversified and low cost and I try to be very methodical about rebalancing.

Probably like many of your members, when it is time to rebalance, I sometimes feel like I don’t want to rebalance because I’m worried about this, that or the other thing. Just to be disciplined about rebalancing is another good strategy, I think. I rebalance by dates, not triggers, unless something is really out of whack that I need to revisit; I usually rebalance by dates about once or twice a year.

I try to practice what I preach to some degree in terms of diversification, low cost and consistent rebalancing to make sure the portfolio makes sense.

Discussion

FREE REPORT

Shane Milburn from TN posted over 12 years ago:

Peter Asprey from CA posted over 12 years ago:

James Hargreaves from GA posted over 12 years ago:

James Hargreaves from GA posted over 12 years ago:

Christian Hansen from AZ posted over 12 years ago:

Bruce Ballengee from Texas posted over 12 years ago:

Robert Kraft from NE posted over 12 years ago:

Fernando Robles from FL posted over 12 years ago:

Emmanuel Daugeras from France posted over 12 years ago:

Charles Foxx from NM posted over 12 years ago:

David Lash from CO posted over 12 years ago:

Pearl Spodick from CT posted over 11 years ago:

Vaidy Bala from AB posted over 9 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account