Related

Portfolio Strategies

by Timothy McCarthy | May 2014

After decades of working on Wall Street, the secret to investing successfully still remains the same as I had first learned in my early years.

Actually, it’s no secret; many investors have heard it already. The problem is that too many investors still do not practice it. Simply put, if you invest over a period of time, properly diversify across a variety of asset classes and leave the portfolio relatively stable, it will undoubtedly grow at a greater rate than by leaving it in the bank, but with much less risk than trading.

Why is it that so many people don’t follow such a straightforward plan?

One answer comes from listening to what people say about their investing strategy. Over the decades of helping investors of all ages across some 25 different countries, I have been amazed at how frequently I have heard the same statements in multiple languages from people at all levels of sophistication:

Yet, we have all seen that most investors who actively trade, especially across asset classes, on average lose money. Men in particular won’t tell you about their losses, but their losses are real. It reminds me of how frequently my friends have told me that they “broke even” while gambling in Las Vegas or Macau. But we know if all the men who say this really “broke even,” all those beautiful and expensive gambling hotels would not exist.

Why do so many people insist on actively trading their portfolios?

Today, I am more forgiving of such investors than I was before. After all, it is human nature to want to succeed, to want to do better than your friend, your brother-in-law, your fellow workers. It is this drive to excel that has made human beings accomplish so much. But there are two reasons why looking at investing as a competition can lead to problems.

Conversely, there is the other type of investor who is constantly in fear of losing their money and simply can’t sleep at night if any of their funds are exposed to volatility. Yet volatility over time is where you can make more returns than in assets that never fluctuate. So, sadly, this type of person ends up getting no long-term growth and may end up short when they are in their later years.

After years of frustration watching people make mistakes even after they had received sound investment advice, I began to refine a different approach for investors that could better reflect what they often want to do instinctively while keeping their portfolio goals on track. In working with a variety of advisers and their clients, I found that rather than giving clients lectures with lots of graphs and charts, people responded better to an approach that functions more like a client/adviser conversation guidance tool.

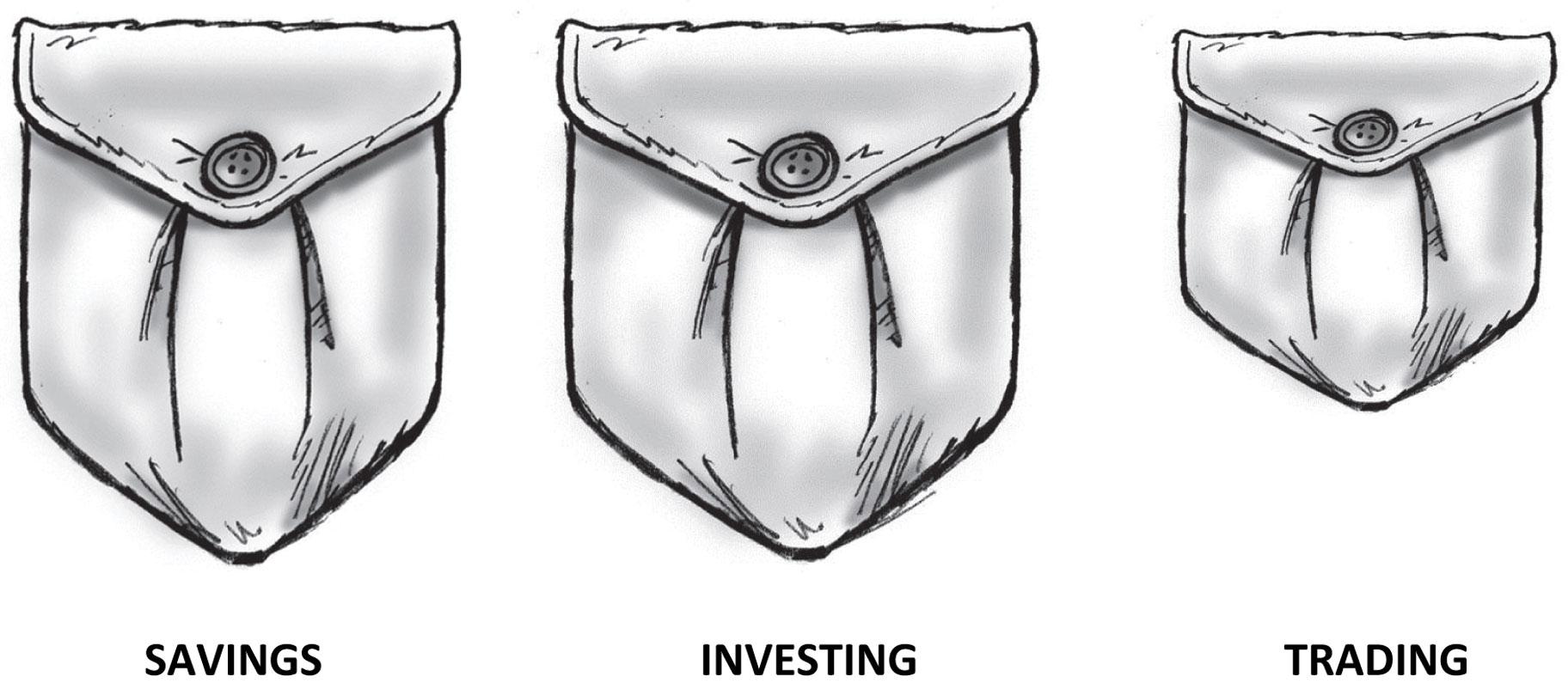

I call it Three Pockets because most people think of their money as being set aside in different pockets. The pockets are shown in Figure 1.

The first pocket helps an adviser work with an investor to find out how much money they really need to keep in their Savings Pocket. This pocket has two objectives:

Of course, everyone needs a Savings Pocket, for short-term needs and in case of an emergency. The question is, how much should stay there? After all, this pocket cannot grow, given how low interest rates are.

How much in this pocket is enough? It really depends on each person’s personality and short-term needs, but typically for a retired person, having around six to 12 months of your expected expenses in this pocket is sufficient. You may feel you need more, but remember: There is a portion of your investment pocket that is still growing but is invested in relatively liquid and low-volatility assets that will be available to you if you need it.

This is where the bulk of your money should be. The objective in this pocket is to:

How do you accomplish this task? As we discussed before, you just do the following:

Many of you may say, how do I know it will work? I took a look at the last century of data and said, what was the worst time that you could have been fully invested in a diversified package of asset classes including stocks and bonds? It was 1930, when the stock market dramatically crashed and took a long time to recover. If you had followed the strategy of trickle investing each year—in this case, starting to invest 15 years before retiring, and then, after retiring in 1930, slowly trickled out the same amount that you had been putting into your diversified Investing Pocket—guess what? You didn’t run out of money until you were well into your 90s. Whereas if you had had only a Savings Pocket where you had put all your money only into the bank, you would have likely run out of money in your mid-80s.

Why is this so? It turns out that markets typically crash after a recent run up. And the major markets throughout time typically do return to a more stable path. Thus, as long as you had spread out your investing into the various markets over a period of a decade or more, didn’t panic, and each year redeemed only the portion you needed to live off of, you did just fine even if you had bad timing luck.

I realize that for many people, especially after they have retired and can’t make back their money, it is scary to see markets drop. But as long as you bought over a long period of years, you will never have bought on average even near the top. And as long as you don’t panic and sell, you don’t lose what you don’t sell. And the global markets, at least for the majority of the asset classes, do come back.

Then, you might say, what do I need a third pocket for? Let’s first understand what a person does in this pocket.

This is your discretionary pocket. You don’t need to have one; however, this pocket can take care of a few important objectives.

Given the natural dangers in this pocket, it is typically not wise for investors to fund the Trading Pocket until after they have properly funded their Savings Pocket and Investing Pocket. The money that goes into here is the money that you can afford to lose. For instance, if you hit it big in this pocket, you can vacation in Hawaii. But if you lose your money in this pocket, you will just be barbecuing in the backyard this summer. The important point is that your long-term retirement nest egg is not put into jeopardy by what you do in this pocket.

The Trading Pocket can be a great tool for both the risk-seeking and, ironically, the risk-averse investor.

First off, for risk-seeking people, this is where they can channel their urge to excel. It is okay to make bets here as long as it does not affect the core investment portfolio. I came up with this idea after reading about how various doctors and researchers had positive results with many more patients when they did not always completely forbid them from doing something. They often had better long-term outcomes by working out a “maximum allowed’ restraint with each person. For instance, it is certainly okay for the average person to have a glass of wine when they are having a nice weekend dinner. But if they are finishing off a few bottles every night, it is clearly not good for their health. The same goes with trading. If a person really wants to trade, it is okay as long as it is a minority of their total portfolio and does not impact their core retirement money. Even when someone is good at trading, his or her spouse may say, “Honey, you are a good investment manager. But maybe you should not be our only manager.”

Discussing the Trading Pocket is a good exercise for people. For instance, when someone says, “I want to invest, but is this a good time?,” the best reply is that it is the right question for the Trading Pocket. But for the Investing Pocket—since you should regularly be trickling in and trickling out over the decades, irrespective of market timing—it is not a relevant question.

Ironically, the Trading Pocket can also be quite helpful to risk-averse investors. For instance, if you are the type who often worries about the markets collapsing, just fund the Trading Pocket each year with a small amount of money invested in, let’s say, in the U.S. stock market, above what you have already invested in your Investing Pocket. Then, when you panic, you have something that you can sell off. Just sell all or half of what is in your Trading Pocket and put it in cash. That way, you will feel good that you did something, yet it kept you from touching your Investing Pocket. The Trading Pocket can act as a useful “panic pressure release valve.”

How much can a person put into the Trading Pocket? The most important guideline is to first fund the Investing Pocket enough so that when you retire, you know you will have enough to live off of. But if you don’t have the patience to wait until after the Investing Pocket is funded, then just make sure you are only putting a small portion, less than 20% of your available investing money, into your Trading Pocket.

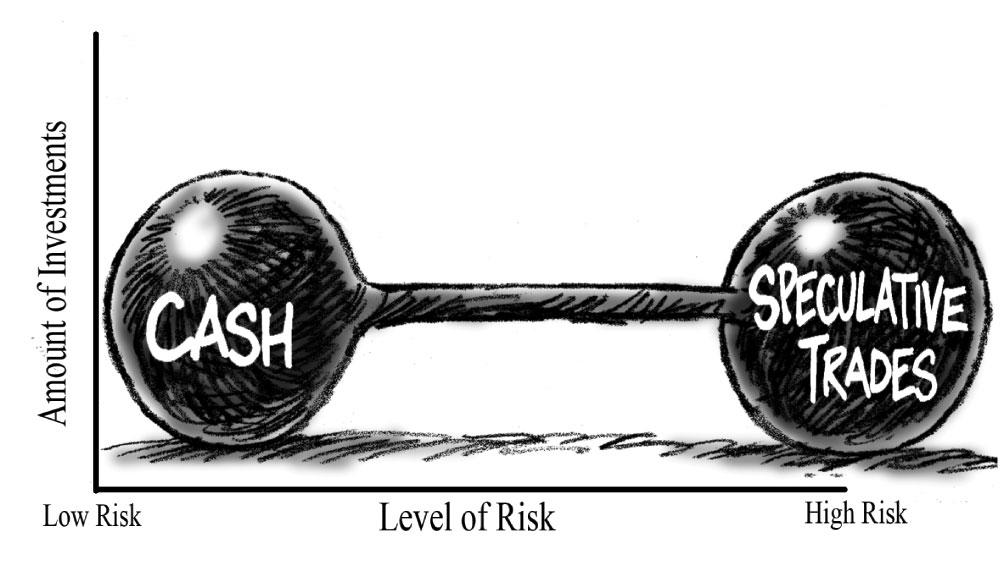

Normally, when people are retired, even if they are affluent, they should keep less than 15% to 20% of their total funds in this speculative pocket. But there are of course valid exceptions. A retired wealthy friend of mine said to me once, “Hey, Tim. This is my only fun in life. I like to trade and I already have enough saved up. I enjoy trying to beat the market.” His children probably didn’t like that half his money was allocated to active trading, but after all, it is his money and he should be able to do what he chooses. Figure 3 illustrates a different approach tycoons followed to balance their very high-risk trading investments and business ventures.

In sum, using the Three Pockets approach to allocating and managing your money before and after retirement can be quite useful.

From a risk management standpoint, you can feel comfortable that irrespective of what the world throws at you in the coming years, your money will ultimately grow. And at the same time, you have built in enough flexibility to follow your unique dreams in a reasonable fashion.

Portfolio Strategies

John Klein from OH posted over 12 years ago:

Barry Slatton from AL posted over 12 years ago:

Ted Rosenberger from PA posted over 12 years ago:

Jim Grant from OH posted over 12 years ago:

John Knox from AL posted over 12 years ago:

George Pledger from CA posted over 12 years ago:

Ben Lis from NY posted over 12 years ago:

Naim Ansari from Eastern Region posted over 7 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account