The Federal Reserve Board’s aggressive and accommodative measures to bring down interest rates, thereby stimulating the economy, continue to raise concerns about future inflation, even while many feared the economy could be heading into a prolonged deflationary period. In turn, the prospect of higher inflation has sparked considerable investor interest in Treasury Inflation-Protected Securities (TIPS) and other inflation-hedging assets.

Cash flow into TIPS this year was $7 billion though September 30, 2010, as compared to $27 billion and $13 billion for full years 2009 and 2008, respectively. The significant increase in 2009 cash flow was in part due to investors’ flight to safety. Total net assets of $104.5 billion as of September 30, 2010, clearly indicate that the TIPS market has experienced significant growth since the government’s first inflation-protected bond was issued in January 1997.

An important reminder for investors seeking to protect a portfolio’s purchasing power is the fact that the total return on a TIPS fund is a function of both actual trailing inflation and the bond market’s expectation regarding future inflation. Consequently, while a TIPS portfolio does adjust an investor’s principal investment by the actual trailing inflation rate, changes in inflation expectations can produce subpar or negative total returns even when actual inflation is positive. Yet, regardless of the direction inflation takes in the future, some bond investors may benefit from knowing that they have some degree of inflation protection.

To help investors assess the role of TIPS in a broader portfolio, we review the mechanics of TIPS, the concept of the break-even inflation rate, and the nature of the inflation protection provided by a TIPS fund. We then compare the absolute performance of a broad TIPS portfolio over the past 10 years with the actual inflation rate, and the relative performance of a TIPS portfolio compared with that of a portfolio of nominal U.S. Treasury bonds. Finally, we frame a discussion about an appropriate allocation to TIPS as part of a taxable bond portfolio by summarizing the relative market capitalization of the TIPS market.

Mechanics of TIPS and the Break-Even Inflation Rate

To truly hedge inflation, an investment’s return should increase at least as much as the rate of inflation (as measured by the non-seasonally adjusted Consumer Price Index for All Urban Consumers, or CPI-U). However, nominal bonds are issued with a stated principal value that is fixed for the life of the bond. Hence, the real (inflation-adjusted) value of a nominal bond falls when actual inflation exceeds the “expected rate” of inflation that was built into market interest rates when the investor purchased the bond.

Unlike nominal bonds, TIPS are designed to provide for inflation-adjusted increases (or decreases) in both principal value and interest payments. The real rate of return (above the actual rate of inflation) provided by TIPS comes from three sources:

- Monthly inflation adjustment to principal value, which can be positive or negative, based on a two-month-lagged value of the CPI-U.

- Coupon interest, starting with a fixed interest rate. The actual dollar amount of the semiannual coupon payment to the investor changes with the actual rate of inflation over the life of the bond and is derived by applying the fixed coupon rate to the inflation-adjusted principal value of the bond.

- Change in price of the bond, based on changes in real yields in the marketplace.

To understand the differences in yields between TIPS and nominal bonds, it’s useful to review the components that make up the nominal yields for both securities:

Treasury nominal yield =

Real yield + expected inflation rate over the life of the bond + inflation risk premium

TIPS nominal yield =

Real yield + lagged actual inflation rate

As these formulas show, the yields on nominal Treasuries and on TIPS will differ depending on both the size of the inflation risk premium (which reflects the difficulty of forecasting long-run inflation) and the gap between expected inflation and actual lagged inflation. Under most economic and market conditions, expected inflation and actual lagged inflation will not deviate substantially over short time periods. As a result, the size of the inflation risk premium will be the main factor in the yield differences between TIPS and Treasuries.

The difference between the yields of a nominal Treasury bond and a similar-maturity TIPS bond is known as the break-even inflation rate (BEI). The break-even inflation rate represents not only the bond market’s expectation of future inflation over the life (or maturity) of the bonds but also risk premiums that reflect the uncertainty about future inflation and the relative liquidity of the two bonds.

For perspective, we note that on September 10, 2010, the yield of 10-year TIPS was 0.75%, while the nominal 10-year Treasury yield was 2.53%. Thus, the 10-year break-even inflation rate was 1.78%, down from 2.41% at the end of 2009 but considerably above the 0.12% spread that existed at the end of 2008. The rise in the BEI relative to December 2008 may be attributed to both improving economic conditions and broad concerns that the fiscal and monetary stimulus will lead to inflation down the road.

Hypothetical Performance of TIPS Versus Treasuries

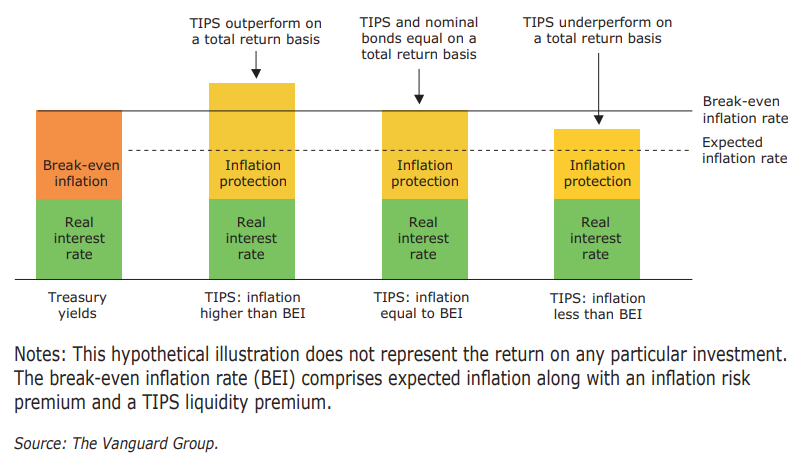

As illustrated in Figure 1, the performance of a TIPS portfolio relative to that of a portfolio of similar maturity nominal Treasury bonds is determined not only by the level of actual inflation but also by whether that realized inflation has exceeded the break-even inflation rate at the time the portfolio was purchased.

Figure 1. Hypothetical Illustration of TIPS Return Relative to Nominal Treasuries

Hypothetically, if actual inflation is above the break-even inflation rate, TIPS will outperform fixed-rate Treasuries of equivalent maturities. For this reason, TIPS can provide an economic benefit in the event that future inflation in the United States is higher than the bond market currently anticipates. If actual inflation is equal to the break-even inflation rate, investors, theoretically, would be indifferent about owning TIPS or equivalent Treasuries. If actual inflation is lower than the break-even inflation rate, nominal bonds may outperform over the life of the bonds.

In the long run, nominal bond returns should surpass the returns of TIPS by an amount equal to the cost of the inflation risk premium. This premium is the reward earned by investors in nominal Treasury bonds for bearing inflation risk (i.e., the uncertainty over what the rate of future inflation will actually be). For this reason, the total return on a nominal Treasury bond portfolio has tended to be slightly more volatile than that of a similar-maturity TIPS portfolio.

Actual Performance: 2000–2010

As an inflation hedge, TIPS should be evaluated in terms of their ability to provide returns above the rate of inflation. However, inflation alone does not determine how well TIPS perform. There is no guarantee of a positive return, real or otherwise, even in the case of an inflation surprise, because TIPS returns are a function of the inflation accrual and the change in real yields.

Yields are affected by many risk factors. The most significant would be changes in the break-even inflation rate associated with either a change in forward inflation expectations or a change in the inflation risk premium required by investors in nominal bonds. TIPS returns may also be affected by changes in the shape of the yield curve and by other factors such as liquidity risk, the supply of new issues (of both TIPS and nominal Treasuries), or the amount of inflation built into a bond.

Figure 2. TIPS Returns, Treasury Returns, and Inflation

To demonstrate that TIPS returns can be lower than the rate of inflation or even negative when inflation is high or rising, we compared actual annual inflation with annual returns for TIPS and nominal Treasury bonds of comparable duration (about three years) for the period 2000 through September 10, 2010 (Figure 2).

During this period, there were three years when the TIPS total returns did not provide a return above actual inflation. In 2005 and 2006, negative inflation-adjusted returns were primarily the result of rising real rates as the Fed tightened monetary policy. In 2008, TIPS returns lagged inflation and underperformed nominal Treasuries owing to investors’ dramatic flight to quality and the relative illiquidity of TIPS compared with nominal Treasuries. On the other hand, there were seven full years during this time when the break-even inflation rate rose and TIPS returns were greater than actual inflation (2000 through 2004, 2007 and 2009). Throughout 2009, the TIPS market gradually priced in a recovering economy. The widening of the break-even inflation rate was a function of rising yields on nominal Treasuries, as well as declining yields on TIPS. This led to the strong outperformance of TIPS relative to nominal Treasuries for the year (+11.4% versus –1.4%, respectively).

Investment Implications

The decision to invest in TIPS is based on the following: a speculative view that future inflation will be higher than market expectations or a preference for diversifying higher inflation risk, albeit at the cost of a lower expected return.

A useful starting point to frame a discussion about an appropriate allocation to TIPS in a broader taxable bond portfolio is to summarize the relative market capitalization of the TIPS market. TIPS represent only a modest portion (3.9%) of the overall U.S. taxable fixed-income market, as represented by the Barclays Capital U.S. Aggregate Bond Index. For investors considering substituting TIPS for standard Treasuries, TIPS represent 6.0% of all Treasuries and 11.0% of the Treasuries included in the Barclays index (as reported by the Securities and Financial Markets Association and Barlcays Capital Live).

While there is no “one-size-fits-all” solution for preserving purchasing power that is appropriate for all portfolios, in a 2009 Vanguard study Donald G. Bennyhoff found that TIPS can be a useful option in a real-return strategy. The study concluded that TIPS may be most appropriate for “policy” portfolios—such as pension plans—with well-known liability streams that are highly correlated with the CPI-U. However, if the cost of the liability in the future is higher than forecast, Bennyhoff found that the real return of TIPS may not be sufficient to compensate for the shortfall.

Determining an appropriate allocation to TIPS depends largely on the portfolio objective of the individual. For example, for an investor with an aggressive strategy designed to optimize total return over a long time horizon, an allocation to TIPS may be less important. However, for an investor with a more defensive strategy who is concerned about inflation eroding purchasing power, TIPS can be useful. Thereafter, determining the size of the allocation to TIPS will depend upon the level of risk that the investor wants to mitigate.

Conclusion

In summary, historically, no asset class has provided a “pure” hedge against inflation. However, for investors looking to protect themselves from the risk of unexpectedly high inflation, TIPS are a viable option and can play a role within a diversified and balanced portfolio. Although TIPS represent only a modest portion of the bond market, they do generally provide a relatively low-risk hedge against unexpected inflation. This hedge, however, is not a guarantee. There can be circumstances when TIPS do not provide positive returns, even during periods of unexpected inflation. Nevertheless, in most instances of an inflation surprise, TIPS can provide an important benefit.

John from NY posted over 15 years ago:

Peter from MD posted over 15 years ago:

Charles from WI posted over 14 years ago:

Jim from CT posted over 14 years ago:

Jim from CT posted over 14 years ago:

Scott from NY posted over 14 years ago:

Gerry from IL posted over 13 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account