Related

Commodities

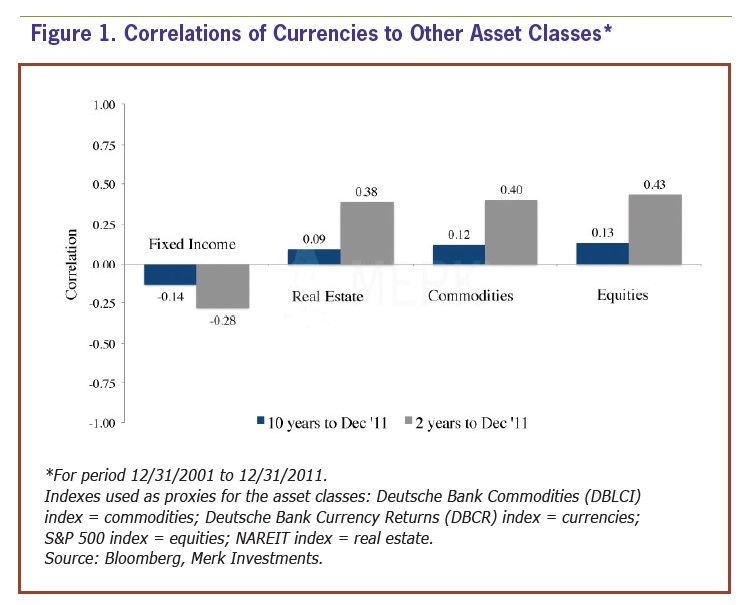

Investing in currencies can reduce the overall risk profile of your portfolio, as currencies have different and less volatile returns than stocks and bonds.

by Axel Merk | April 2012

Axel Merk is the president and chief investment officer of Merk Investments. I spoke with him in recently about investing in currencies.

Charles Rotblut (CR): When someone talks about investing in currencies, what does that actually involve?

Axel Merk (AM): Obviously, everybody has heard of the U.S. dollar, but other countries and regions have their own currencies—say, the euro or the Swiss franc or the Australian dollar or even the Chinese renminbi [yuan]. And if you want to conduct business in that currency, you have to exchange your money; currencies always trade in pairs, and it’s always one currency versus another one.

There are two main ways that we think about currency investing. One is called directional currency investing, and that would be the U.S. dollar versus a currency, a basket of currencies or a managed basket of currencies—say, the U.S. dollar versus the dollar index, which is a basket of currencies, or versus one of our currency funds, two of which are managed baskets of currencies.

The other way to think about currency investing is in a non-directional sense. Non-directional currency investing might take offsetting positions in currencies outside of the U.S. dollar. As an example, rather than taking a position in the U.S. dollar versus the euro, you might think about the Australian dollar versus the New Zealand dollar. What this entails is taking long or short positions in any one currency.

Think about the returns you may generate when you take a long position in the Australian dollar while you concurrently short the New Zealand dollar. You can’t guarantee that you will make money with that position, but you’re almost certain that the returns you generate will have very little correlation to anything else that you may be holding in your portfolio. That unleashes the full power of currency investing, in that you can design a portfolio that has a low correlation to the rest of your portfolio. Plus, if you have a profitable strategy, you may be able to add value without substantially adding to the risk of the portfolio.

CR: In terms of actually buying currencies, obviously, anybody can go to a currency exchange and buy euros or buy Canadian dollars, but what exactly are people investing in? Are they investing in futures? Are they investing in bonds?

AM: There are different ways to invest in currencies. In the most straightforward way, you actually go out and buy the currency, and then you hold it typically in a bank in a foreign country. Now, for most investors, it’s kind of complicated to set up such capabilities. What we do, for example, in our Merk Hard Currency Fund (MERKX) is go out and buy the currency, and then within that currency, we buy short-term money market types of instruments. So we would buy a German treasury bill, or the remaining days of a Finnish or Australian government bond, and own these cash-like instruments denominated in the foreign currency. That’s one way of doing it. In that case, by the way, currency investing is very similar to international bond investing. But unlike a bond fund where you have currency, interest and credit risk, in a directional currency fund, you focus on currency risk while trying to minimize interest and credit risks.

Now, that is how we invest in some of our funds. Another way of investing, which represents the vast volume of currency trading in the world, happens through forward currency contracts. You can use futures or forwards. People may be more familiar with futures trading, which happens on a regulated exchange, but that’s actually just a small fraction of the trading volume. The vast majority of the volume is in forward currency contracts. What that means is that you have a customized contract with a brokerage firm or with a bank to, say, buy a million euros one week from now or one month from now (or any specific date in the future). And the difference to taking delivery of the currency is that you retain your dollar cash until you buy that currency at the agreed-upon time. An advantage of doing this is that you can also sell or short a currency with minimal cost. And some people like to use leverage as they proceed with those sorts of transactions.

All together, there is $4 trillion daily volume in the currency markets, and an absolutely staggering volume happens because a lot of people are using derivatives to get exposure to different currency moves, and a lot of people use leverage in doing so.

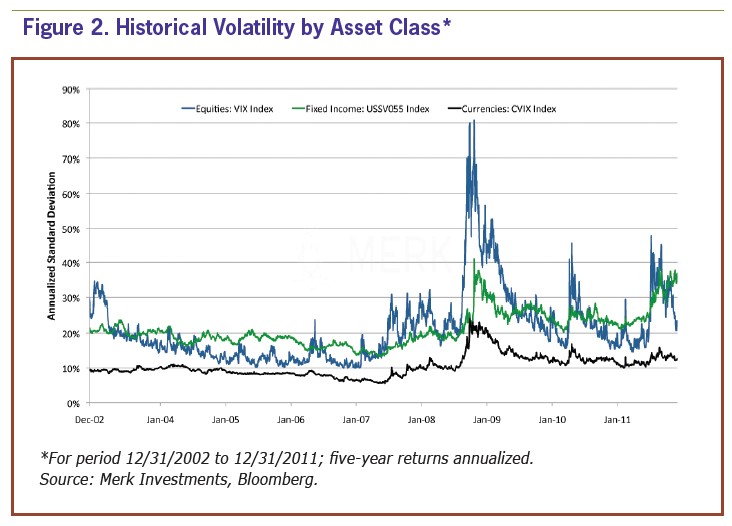

Now, you don’t have to use leverage. When you don’t use leverage, the currency market is actually much less volatile than the equity market or even the fixed-income market. When the euro moves, say, from 1.32 to 1.30, the entire world pays attention, because a two-cent move in the euro versus the U.S. dollar is very significant. On a percentage basis, though, it’s a very small move. Think about an Internet stock moving from 132 to 130; nobody would even blink. By not employing leverage, the currency market allows you to be a long-term investor. Just like in any other asset class, there are short-term traders and long-term investors, those who use leverage and those who do not.

CR: For an individual investor, what we’re talking about is actually investing and not active forex [foreign exchange] trading as promoted by the television commercials?

AM: That’s a good question. If you think you know what’s going to happen tomorrow in the markets, by all means, you’re probably somebody who would like to use leverage, because the currency markets are otherwise too boring. There are plenty of websites out there that allow you to take a speculative position with a lot of leverage. But on the other hand, if you think that there’s a long-term trend, say, that the U.S. dollar may weaken because we’re better at printing money than other countries are, you don’t necessarily want to use any leverage, because like any market, the currency markets are not a one-way street. Things go up and down in these markets. And if you use leverage, the cost of the leverage is going to erode your returns. At the same time, if you want long-term exposure, the question is, how can you achieve it? If you want to get exposure to one currency, you can buy it outright—you can use an ETF (exchange-traded fund) or a mutual fund; the difference is that a mutual fund would more likely be a managed basket of currencies rather than a single currency.

On that note as well, the person who thinks that something specific is going to happen in the market is probably going to have a very good idea about which currency they want to buy or sell. But if people just generally want to take advantage of the currency markets, they may be more inclined to use a basket of currencies to mitigate the risk of any one currency. In our case, for example, we try to add value by managing that basket, because most folks are not currency experts, and by having institutional access, where we get executions that an individual investor simply cannot get. If you’re an individual investor, you generally pay enormous commissions to buy and sell currencies, whereas on the institutional side, the commissions are absolutely minimal. There is very little cost involved in moving millions, even tens of millions, of dollars around. This is one of the reasons why speculators are attracted to that segment, because of the low transaction costs. At the same time, you don’t have to be a speculator; you can get exposure to baskets of currencies very efficiently through some investment products.

CR: What’s actually moving currencies against each other? I realize this gets complicated pretty quickly, but is there a simple explanation you could give?

AM: Sure. Well, most people think currencies are complicated. I would think following thousands of stocks or mutual funds is far more complicated. You have about 10 major currencies, and they are driven by supply and demand, just like anything else is. When more people want to invest in a currency, that currency will increase in value versus another currency. So on the most fundamental basis, it’s the same as with anything else.

Some people say that because currencies are a zero-sum game (one currency always has to gain at the expense of another, as currencies always trade in pairs), there is no chance to make money in the currency space. We could not disagree more. It is not a zero-sum game; there are some significant differences. Some countries print more money than others. At the same time, almost everybody who has taken an economics 101 course is told that the difference between currencies depends on the interest rate differential and so forth. While I think those theories are great for textbooks, in practice, studying interest rate moves alone is not going to give you a winning investment strategy.

There are investment strategies in the currency world, just as there are in equities or any other security. You can be a short-term investor, or you can be a long-term investor. You can invest based on technicals, or you can invest based on fundamentals. It turns out that in the currency market, you have more inefficiencies than in other markets. We believe this is due to a significant number of participants who are not profit maximizers. Aside from corporations that hedge their exposure, you have central banks that manage their reserves; you have tourists who are very active in transacting in currencies without trying to optimize the currency component of their transactions. You even have many international equity investors who are not necessarily looking to optimize the currency component of their investments. As a result, you have a lot of folks trying to arbitrage the sort of inefficiencies that come from all these participants.

Many of these strategies are very technically driven. But at the same time, you can also invest in currencies based on macro analysis, based on fundamental analysis. We have these billions of dollars that are being spent and trillions being printed. Well, the markets are moving when so much money is being printed and spent, but why take on the equity risk when the only thing investors are doing is chasing the next move of the policymakers? In the currency markets, you can very clearly express your view by buying the currency where policymakers, in your opinion, are more reasonable and are printing less money. And you can have an investment approach in the currency markets that is very similar to that in the equity markets and any other market. The important thing is of course that you have your own framework in which you’re thinking about the market. And then you put your money where your mouth is or where your thoughts are, and you apply the same discipline, you have the same pitfalls and so forth.

CR: I know you talked about how corporations hedge. We do have some members who are buying multinational corporations or who might be investing in foreign corporations. But you’re arguing that investing in currencies actually gives you a different exposure than buying the stocks outright, correct?

AM: Well, first of all, if you don’t use leverage, your volatility is much lower in the currency space than in the equity space. And as I just indicated, there’s a lot of noise in the equity space these days because people are just chasing the next move of the policymakers. And so you’re not really investing in many stocks because of their fundamentals but because of what you think the policymakers are doing, and I believe the currency space allows you to better express that.

Second is that, by all means, the companies in the S&P 500 index are very active internationally. But according to our studies, about 80% of the earnings of S&P 500 companies are hedged back into the U.S. dollar. So if you’re investing in the S&P 500, you’re only getting a muted impact of the international component that you’re trying to get. Conversely, many people invest in international equities. If you buy an international equity mutual fund that invests in large-cap companies, odds are these companies want to sell to American consumers. They’re not only selling here, but it’s one of the reasons that the correlation of international equities is so high with the S&P 500. Again, you may not be getting all the diversification that you want.

By choosing a currency fund, you have a pure play on the currency world. If you talk to a currency manager and then, say, an international small-cap equity manager, there’s a world of difference in what they focus on. And for good reason: The small-cap equity manager who invests in an Australian law firm is supposed to do fundamental research on the law firm; whereas, the fund manager focusing on currencies ought to think about the monetary policies, interest rate differentials, and fiscal and monetary risk in different countries. So there is very much a complementary effort in trying to access the same markets, but with very different dynamics. In our view, many of these things are complementary. Of course, any investor has to do their homework, with any instrument they look at, be that a mutual fund, a stock, or anything else.

CR: What about, in terms of allocating a portfolio, if someone is holding a portfolio of stocks and bonds, how do they make the decision as to what portion they should allocate to currencies? What’s a good percentage?

AM: And then, of course the related question is, where do you take it from, which of your buckets?

Let me answer that question first: Increasingly, investors are considering currency to be its own asset class. And it’s an alternative asset class. Especially when you invest non-directionally, as I indicated earlier, it is clearly its own asset class. When investing directionally, some people put it in the bucket of an international bond fund. And, by the way, there’s a third way that people use these sort of products these days: If they invest in international equities, for example, but become more cautious on the international equity markets, instead of selling the foreign stocks and going back to the U.S. dollar, some investors may save the international cash. Obviously, they have currency risk. By taking the currency risk but not the equity risk, they are reducing the overall risk profile of their portfolio, but they are still invested.

Now, as far as how much people are deploying, we conduct surveys regularly, and the most common answer that we get is that about 4%–6% of investors’ portfolios are allocated to currencies. Some allocate less, and some significantly more. The ones who invest significantly more are either very concerned about the purchasing power of the U.S. dollar, or, and this is in some ways a related angle, they want to have a more comprehensive way of managing the currency risk of their investments. They realize that, yes, they want to be invested in the S&P 500, and they want to be in equities, but they do have currency risk with the entire portfolio that they have, and they are looking for ways to manage that more actively.

CR: In terms of risk, I know some investors are worried about what’s going to happen with the U.S. dollar, particularly with interest rates rising. But if they go overseas to, say, the euro, they’re also concerned with what’s going on there. So is credit and interest rate risk a consideration?

AM: Well, of course. Ultimately, we believe there’s no such thing anymore as a safe asset, and investors may want to take a diversified approach to something as mundane as cash. Obviously, if you invest in the U.S. dollar, the only thing you should be worried about is purchasing power; although when you have your money in a prime U.S. money market fund, odds are that if you look deeply, the fund owns commercial paper issued by a European bank denominated in U.S. dollars. So through your U.S. money market fund, you are actually giving a loan to European banks like, say, Societe Generale. It’s within this context that we often say that we’d rather own a German treasury bill than a U.S. money market fund.

A country like China is ever more actively managing its reserves, and that’s kind of how an individual investor can think about it. Don’t trust your government any more to make sure your purchasing power is being retained. Take charge of your own reserves. Manage them as you deem most appropriate. And, by all means, investing in currencies is not the same thing as investing in Internet stocks. You can expect a different risk and return profile. But why not consider managing the currency risk even of the U.S. dollar by diversifying into baskets of currencies? Obviously, you’re taking on the currency risk, which you wouldn’t have by staying in the U.S. dollar. However, maybe that’s precisely what you want exposure to, given the purchasing power risk that you have, given the monetary policies that are being pursued here in the U.S.

CR: Gold is used as a hedge against inflation, as well. How do currencies and gold work together?

AM: We consider gold the ultimate sound money, the one currency that is very difficult to inflate—and I say very difficult, because it is possible to ramp up gold production, it just takes a long time to do it and it’s very expensive to do so. The other key difference between gold and currencies is that the liquidity in the gold market is much lower. As a result, the volatility in gold has to be much higher. The one thing we have observed is that even gold bugs rarely have all their money in gold, even if they have very negative views on the state of currencies. The simple reason is that they have their daily expenses in U.S. dollars, and gold can move quite radically, not just to the upside but also to the downside.

So when you employ currencies, you can spread your risks by using baskets of currencies, say, to get exposure to commodity currencies, for example. Commodity currencies such as the Australian dollar, New Zealand dollar, Norwegian krone, and the Canadian dollar are historically correlated to the price of gold without having the same level of volatility. It comes down to the broader assessment of what risk/return profile you want to have in your portfolio.

Ultimately, I would say, yes, gold does play a very important role in today’s portfolio, but at the same time, the first question any investor has to ask themselves is: Can I sleep with that investment at night? And if you cannot, then you are overexposed. That’s why the folks who like gold rarely have all their money in gold, because they need to be able to stomach a correction in gold, as well.

CR: In terms of tax implications from owning currencies, what are investors looking at?

AM: Well, it depends on how you own earning currencies, but just the mere fact of buying a currency and owning, say, a foreign cash instrument, of owning cash, you typically have to pay taxes on the gain that you have when you convert the money back into the U.S. dollar. If you buy an international fixed-income security, you have to pay tax on the gain you have in that international fixed-income security. With derivatives, it depends a little bit on the type of derivative you are using, but generally speaking, when there are gains, there are taxes. The futures market has a tad of a different treatment and, generally speaking, having gains in the currency space does generate income and a significant portion of it is likely going to be short-term income. If you, say, buy a short-term debt security, even if you have a long-term investing horizon, it is going to mature within a short period and as such be taxable as a short-term gain.

CR: Is there any time frame people should think about? If somebody’s going to allocate some money to foreign currencies, is there a time line they should follow?

AM: Absolutely. Any money that anybody needs in the short term, I would not recommend putting that money at risk, just as a basic rule of thumb.

Beyond that, it really depends on the risk tolerance of any one investor, just like any other investment. As I indicated earlier, I’m not going to dissuade somebody who thinks that they can forecast the markets on a short-term basis from trading. But the folks that we talk to the most, the folks that, I believe, also are in your membership, tend to be the longer-term investors. And one of the things that we believe we have done in our firm is to really educate people that you can use currencies as an investment, not just as a speculative tool. You can use long-term deployments to baskets of currencies, managed baskets of currencies, to mitigate the risk of any one currency. And we see that, especially given recent market turbulence, such as the issues in the eurozone, by actively managing that risk, you can mitigate the risk of any one of these things.

And by the way, we don’t think there’s a crisis in the eurozone, we think there’s a global crisis. This crisis is going to move from one place to the next, so you may want to think about how to position yourself to take advantage of the opportunities that these risks provide. Conversely, of course, it is not so much a question of knowing exactly what will happen, but a question of setting the risks. Is there risk that there will be inflation? Is there credit risk? And do you want to pare down those sorts of risk exposures? When you use currencies, you tend to try to minimize interest risk and credit risk exposures, so in that context, it can be very complementary to other investments that investors already hold.

CR: If investors are holding foreign bonds and they’re getting interest on those, is it treated similar to foreign dividends, where there are certain tax treaties, or do they have to worry about foreign taxes as well?

AM: It depends again on what instrument you is using, but say you’re investing in a mutual fund. You will get a Form 1099 from the fund, and it will tell you which boxes to fill in on your tax return. There are no foreign taxes to be filled in, so to speak. Typically, the mutual fund will take care of foreign withholdings and whatnot and reclaim those withholdings off mutual funds exempt from any of these things. But at the same time, any withholdings that have been taken will be noted on the 1099, which tells you exactly which lines to fill in on a tax form to make sure that all of those things are handled properly.

CR: Are there any implications for IRAs that individual investors need to be aware of?

AM: Again, it depends on how you buy currencies, but generally speaking, mutual funds are eligible for IRA accounts. If you have a mutual fund that tends to generate short-term gains, it might be advisable to hold it in a tax-deferred account for the simple reason that you would not have to pay the taxes on an ongoing basis as short-term gains are being realized.

Commodities

Steve from PA posted over 14 years ago:

Clyde from WI posted over 14 years ago:

Mike from TX posted over 14 years ago:

Samir Desai from TX posted over 13 years ago:

Richard English from VA posted over 13 years ago:

Al Connelly from NJ posted over 12 years ago:

James Hargreaves from GA posted over 12 years ago:

Peter Rukavena from NY posted over 11 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account