Updated on July 1, 2022

The reason investors buy bonds is to achieve a secure cash flow and to reduce their risks in the stock market. However, bond prices and interest rates are extremely reliant on one another and the relationship between the two needs to be evaluated before pursuing.

If interest rates are at a low level, some investors are concerned that after they purchase bonds, interest rates will rise, and their bonds will decline in value. We examine the validity of this concern, the bond price and interest rate relationship, certain alternatives to individual bonds, as well as our proposed solution to navigating both low and high interest rates.

You should not have to wait until the end of this article to get to our proposed solution to determining if it’s a good time to buy bonds during a low or high interest rate environment: We propose a bond ladder of individual bonds structured to take into account your financial needs and objectives. The bond ladder substitutes for staying in cash and trying to predict the direction of interest rates. A bond ladder will also enhance your appreciation of the value of cash flow and the power of compound interest.

What Happens to Bonds When Interest Rates Rise?

When interest rates rise, the prices of bonds typically fall, and vice versa. This inverse bond and interest rate relationship is sensitive to both changes in expectations as well as to overall inflation. It’s also important to remember that when demand for goods and services rise, the Federal Reserve tends to raise its federal funds target rate to slow down economic growth and prevent inflation from being too high for too long.

Additionally, it’s important to understand how different bonds perform in a rising interest rate environment. Investors are more concerned with interest rate changes in longer-dated bonds because those bonds require them to accept a fixed rate of interest for a longer period of time. Offsetting this risk are higher yields relative to shorter-term bonds.

Movement of bond prices impacts investors when they buy or sell a bond. When a bond is purchased and held to maturity, a bondholder’s return is fixed regardless of what happens with inflation. Bondholders receive all interest (coupon) payments due to them from the time of purchase, plus the face value of the bond.

The Relationship of Bond Prices and Interest Rates

Bond prices and interest rates rise and fall in relation to one another like the two ends of a seesaw. The pivot of the seesaw is the fixed rate of return, called the coupon. The interest rate, and thus the cash flow on the bonds, does not change for the life of the bond.

If you were to purchase bonds with a 5% coupon, you would always have a cash flow of 5%. If you purchased the bonds at face value, (a $10,000 bond selling for $10,000), you would always have a cash flow of $500 per year. If you decided to sell your bonds and interest rates have risen, you would be paid less than $10,000 for your bonds so the new buyer could earn the higher interest rate, let’s say of 5.05%. That buyer would still be paid $500 per year in interest and receive $10,000 when the bonds came due. In a falling interest rate environment, the bonds would now be worth more, perhaps $10,500 for an interest rate of 4.95%. The interest paid would remain the same. The buyer would still receive $10,000 at maturity.

Should I Buy Bonds When Interest Rates Are Rising?

There seems to be no shortage of advice by pundits and brokerage firms about when it is a good time to buy and when it is not a good time to buy bonds. As we update this article in 2022, the Federal Reserve is raising the federal funds rate, which boosts short-term interest rates especially. Longer-term rates are also affected, but not necessarily in the same way. No one really knows how many rate hikes over how long a period it will take to tamp down an 8% inflation rate. That does not stop the media from making dire predictions about the losses that will be inflicted on bondholders in the form of lower market values.

When someone tries to judge whether or not this is a good time to buy bonds based on their expectations for interest rates, they are engaging in market timing. Many studies have shown that market timing does not work.

Unfortunately, no one really knows how the financial markets will react to the next Federal Open Market Committee, the meeting after it and so on. Therefore, we cannot answer the question: Is this a good time to buy bonds? We personally come from a place of not knowing—we know we don’t know the direction of interest rates, and we have not found anyone with a consistent track record of predicting the direction of interest rates.

What we know with certainty is that there are always three possibilities regarding the movement of bond prices and interest rates:

- Interest rates in the future may go up,

- Interest rates may go down or

- Interest rates may stay within the current range.

Bond Investing and Mark-to-Market Accounting

We believe that the mark-to-market accounting concept is clouding individual investors’ understanding of the true nature of bond investing. The concept of mark-to-market means that every day, week, month or year (or multiple times a day), the current price of a bond is compared to the price at which you bought the bond. If interest rates go up, the market value of your bonds go down and you are supposed to feel distressed about your bond investment. If interest rates go down, the market value of your bonds go up and you are supposed to feel happy and contemplate selling and taking your gain.

Although mark-to-market accounting is used by all brokerage firms, we believe that the concept is inappropriate for individual investors who are buying and holding individual bonds until their due date rather than trading their bonds. Why should gains and losses be presented when the bond coupons stay the same? Since the bond coupons do not change whether market interest rates go up or down, the cash flow from the bonds stays the same. You receive the same income stream no matter what the price of your bonds is today or tomorrow.

Mark-to-market accounting is appropriate for bond funds since the funds never come due. The bonds in the fund must be sold when they no longer meet the fund’s maturity specifications. Institutions must use mark-to-market accounting, but individual investors are not required to do so. If you use mark-to-market accounting, you will be terrified of rising interest rates. Brokerage firms like mark-to-market accounting because it encourages investors to buy and sell bonds, rather than hold individual bonds to maturity.

Beginning in January 2022, many investors began to sell their bond mutual funds due to inflation fears. This created a buying opportunity for individual investors, as the highest-quality bonds were offered for sale at lower prices when the mutual funds sold bonds to raise cash. If you owned individual bonds, your statement reflected increasing losses. If you held your position, you would continue to receive the same interest payments as you did before the price decline. Interest payments are not affected by price declines. By June 2022, the flows reversed and the market stabilized somewhat.

What If You Decide It’s Not the Best Time to Buy Bonds? A Look at the Alternatives

Let’s look at the alternatives to buying a portfolio of high-quality individual bonds.

One option is to stay in cash or cash equivalents (short-term Treasuries and insured bank products). Many are investing in these products to deal with the current uncertainties. Before December 2021, short-term interest rates were close to zero. However, it is now possible to find offerings better than 2% in two years and 3% in five years. The danger here is in concentrating your assets in short-term investments that will terminate soon and may leave you exposed to reinvesting at low interest rates.

Investors have been encouraged to invest in riskier asset classes to try to improve their returns, even if they can’t realistically afford the consequences of bad outcomes. Thus, investors have gone heavily into stocks, commodities, collectibles, junk bonds and other risky investments. Many of these investments may be inappropriate for investors who have limited resources and who are nearing retirement or are in retirement because the downside risks are too great. Even dividend-paying stocks come with an uncertain outcome since, unlike bonds, they never come due. The dividend may be cut and prices may decline.

Floating rate notes, frequently issued in times of falling or flat interest rates, are not currently available in a rising interest rate market. While you might think it advantageous to purchase them now, the issuers do not see it in their best interests.

Only the federal government is offering an opportunity for retail buyers of taxable bonds. U.S. Treasury Series I bonds sold at TreasuryDirect.gov increase in value with inflation. You can purchase only $10,000 per year with denominations as small as $50. The current yield is 9.62% until October 2022, when the interest rate will be reset. You must hold I bonds for one year. If you redeem them before five years, you lose the previous three months of interest as a penalty. The gain on I bonds is taxed as ordinary income when you redeem them. If you are in a certain tax bracket, you might not have to pay any taxes on your gains if you use the money for education.

So, if you believe that rates are too low on traditionally safe investments, the risks are too great on commodities and junk bonds and stock prices are subject to the market’s volatility, what strategy should you follow?

Bond Ladders and Interest Rates

Individual investors are not institutions. We don’t live forever. We should focus on our finite lifetime needs and goals, taking into account the risks of investments.

We recommend that you consider the benefits of a custom bond ladder. Briefly, a bond ladder of individual bonds is a strategy to have one or more bonds come due in multiple years. Thus, if you have $100,000 to invest, you might have a $10,000 bond come due in each of 10 different years beginning in 2024 and ending in 2034. This is the simplest form of a bond ladder. Alternatively, you might start your bond ladder in 2029 or later years and end in 2039 and have unequal amounts of bonds in each year.

In the strategy of the bond ladder, we find the solution to the problem of losses being generated from rising interest rates when using mark-to-market accounting. Whether interest rates are rising or falling, your bond ladder of high-quality bonds will produce a consistent cash flow that you can rely on. Every year the bonds you purchased march toward their due dates and have a shorter life span.

If your bond ladder is in place before interest rates go up, you have the upside case when rates rise. This is because as interest rates go up, you will be able to increase your cash flow by reinvesting your bond proceeds (from bonds coming due and bonds being called) and your excess interest income in higher-yielding bonds. For example, if you are getting a 2% return and interest rates rise enough over time to give you a 4% return, your cash flow over time will increase by 50%. Thus, if your bond ladder is in place, rising interest rates will not be a concern but will be your upside case.

Guidelines for Bond Laddering

Consider the following guidelines in the design of your buy-and-hold bond ladder.

First, consider whether there are certain years in which you know you will need cash. For example, if your child or grandchild will begin college in six years, you may want to have one or more bonds come due in years six, seven, eight and nine. If you plan to buy a residence in five years, buy bonds that will come due at that time. Always keep enough of a cash cushion so that you can be a buy-and-hold investor.

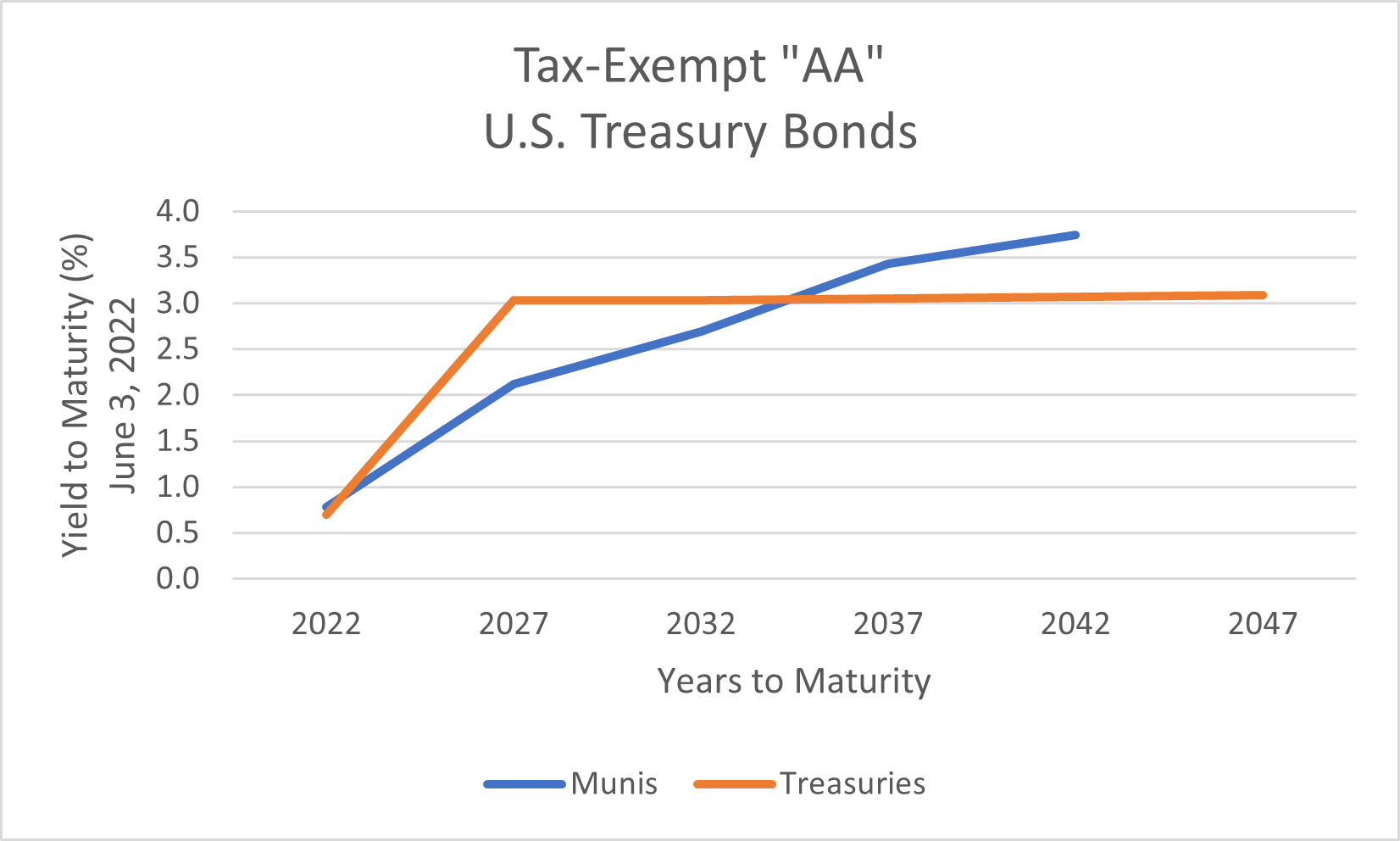

Second, once you have taken care of your known needs for cash, consider the shape of the yield curve. The yield curve is a chart that plots the interest rates being paid by bonds of the same credit quality but different maturities. In the chart, the interest rate is found on the vertical axis and the maturity on the horizontal axis. A current yield curve for AA-rated tax-exempt municipal bonds compared to Treasury bonds is shown below.

The curves change daily depending upon a variety of factors. Generally taxable bonds yield more than tax-exempt bonds, but this is not always the case. This creates a great buying opportunity for those who are interested in tax-exempt bonds.

Third, creating a ladder of short-term bonds will protect you against further increases in interest rates in the near future. However, whatever kind of bonds you purchase for your short ladder, they will provide only a small return in today’s bond market but will not protect you in a falling interest rate scenario. Since the yield curve is currently very steep for municipal tax-exempt bonds, you will receive a lot more return for investing in longer-term bonds than very short-term bonds.

Fourth, keep in mind that every year that passes, the entire bond ladder gets one year shorter. It is wise to maintain a good ladder of maturities and call dates.

Fifth, since we cannot predict what inflation or interest rates will be like in the future, our advice is to get your bond ladder in place instead of trying to determine when the best time to buy bonds is. Waiting for the ideal time before you establish your bond ladder may result in the loss of cash flow while you are waiting if your timing is not precise. There is a cost to waiting.

Our Current Strategy for Buying Bonds in a Rising Interest Rate Environment

In the current environment (June 2022), the yield curve is very steep for tax-exempt municipal bonds, meaning that longer-term bonds may yield a great deal more than short-term bonds. In this environment, we suggest the following strategy.

Purchase bonds that are free of federal income tax for your taxable accounts.

All bonds should generally be rated at least AA by Moody’s and S&P or by at least one of these rating agencies. The bonds should fall into one of the following categories:

- Certain state general obligation bonds generally rated at least AA,

- Certain county and city bonds generally rated at least AA,

- Certain essential services bonds generally rated at least AA or

- Bonds of certain universities generally rated at least AAA.

The bonds should be purchased to form a customized bond ladder designed for your financial needs. If you have no specific needs, we recommend buying bonds with due dates ranging from five to 25 years to maturity with a minimum of six years call protection.

Your customized bond ladder of high-quality bonds will result in the following outcomes:

- Preservation of your wealth,

- Creation of a reliable and predictable cash flow,

- Reduction of your federal income taxes and

- Preservation of wealth for your heirs.

Bond Funds and Rising Interest Rates

When we speak of bonds, we do not include bond funds. There are many differences between individual bonds and bond funds. The following are a few highlights.

Bond funds are not bonds; they are quasi-equities that don’t come due. Individual bonds have a due date. A fund has to sell bonds that no longer meet its objectives and purchase new bonds at current market rates. If interest rates are falling, the bond fund must purchase new bonds at those lower rates. If interest rates are rising and there are many redemptions, the fund must sell bonds into the rising interest rate market in order to meet their redemptions. An alternative for the fund is to keep substantial sums in cash earning nothing, which also lowers the fund’s returns.

If you purchase bond funds, you are making a bet that interest rates will decline. If interest rates were to continue rising for some period of time, you are making a bet that you or the bond fund manager can time the market—turn and trade out before you lose a great deal of money. In January 2022, holders of bond mutual funds started selling their shares as the Fed waited to raise interest rates. The selling trend accelerated as investors became more concerned that inflation was out of control. As rates rose, investors purchased individual bonds to lock in the higher rates. Retail bond investors saw this as a buying opportunity. By comparison, while individual bonds may have the same market volatility as bond funds, as an individual bond approaches maturity its price will move closer to its face value and its volatility will decrease. Whatever the price, the coupon will continue to pay the fixed amount.

Although you can trade out of a bond fund more easily than individual bonds, you can hold individual bonds until their maturity and receive the bond’s face value. You will not have to trade the individual bonds to get your investment back. Trading in and out is expensive and is for professional traders. Individual investors generally find it quite difficult to make two right decisions: when to buy and when to sell. If you sell at a profit, Uncle Sam is the first one to congratulate you and take his share.

It is not possible to determine the cash flow that you will receive on a bond fund because of a number of variables: trading results, future interest rates, expense ratios, trading costs and changes in holdings. Reporting of fund returns varies from fund to fund. The U.S. Securities and Exchange Commission (SEC) 30-day yield is the only true comparable fund yield.

Many bond funds invest in lower-grade (riskier) bonds to stay competitive with other bond funds and to cover their fees and expenses. Some funds are leveraged (use borrowed money) and thus are more volatile than individual bonds. They may be benchmarked to show performance, but the benchmark may itself keep changing. Some funds also use derivatives in the hope of increasing their returns. This will also magnify their losses. In times of rapidly rising interest rates and significant redemptions, mutual funds must sell their best bonds to get the best prices.

Buying Bonds in the Current Interest-Rate Environment

Here are our recommendations for how you should proceed in the backdrop of the current interest rate environment:

- Define your objectives and financial needs.

- Determine your asset allocation between how much of your portfolio you wish to keep safe in a custom bond ladder and how much you will use to speculate.

- Don’t worry about timing interest rates in the market—you probably can’t anyway.

- Set up your custom bond ladder now to generate consistent cash flow.

- Invest your taxable account in high-quality tax-free municipal bonds.

- Sit back and relax knowing if interest rates go up after you establish your bond ladder, that is your upside investment case.

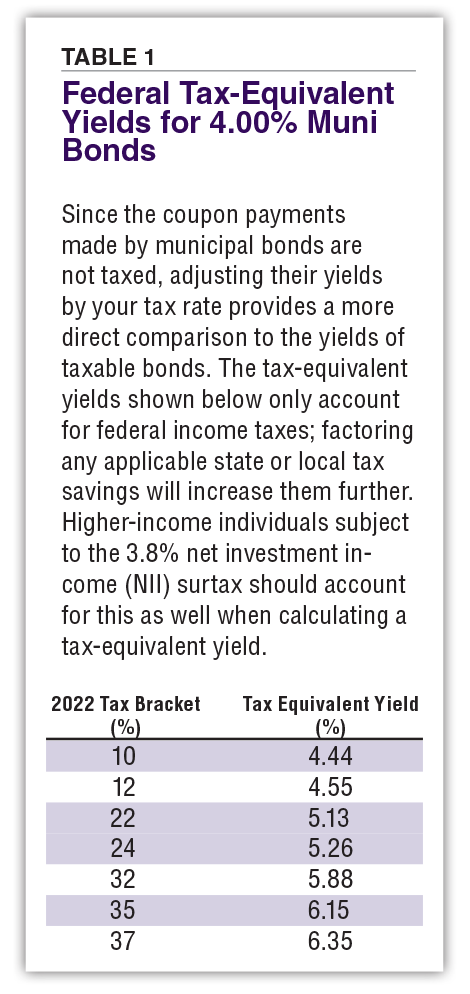

A final and important note for investors in a high tax bracket: The yield to maturity on a long-term high-quality tax-exempt municipal bond in June 2022 is now 4.00% (e.g., Triple-A Oklahoma Housing bonds maturing in 2041 sold at face value). The tax-free equivalent return for a 4.00% yield to maturity for taxpayers in various tax brackets is displayed in Table 1. These may be attractive returns for high-quality investments if predictions of the so-called “new normal” turn out to be accurate.

This article was originally published in the May 2013 AAII Journal. Click here for a PDF of the original article.

Walt B from FL posted over 13 years ago:

Howard... from Oregon. posted over 13 years ago:

Lee from MD posted over 13 years ago:

David from Vermont posted over 13 years ago:

skibutch. from California posted over 13 years ago:

MP from NY posted over 13 years ago:

Jay from California posted over 13 years ago:

Jay from California posted over 13 years ago:

Samuel Dollyhigh from SC posted over 13 years ago:

hildy from Pennsylvania posted over 13 years ago:

SJ from NY posted over 13 years ago:

Hildy from PA posted over 13 years ago:

Ian from Pa posted over 13 years ago:

Charles Rotblut from IL posted over 13 years ago:

Bernie Tarango from CA posted over 13 years ago:

Harry from PA posted over 13 years ago:

James Pier from OH posted over 13 years ago:

Hildy Richelson from PA posted over 13 years ago:

Stephen Sanders from NY posted over 11 years ago:

Hildy Richelson from PA posted over 9 years ago:

TERRY from TX posted over 9 years ago:

Samir Desai from TX posted over 9 years ago:

James Harless from TN posted over 9 years ago:

Bryan Martz from OH posted over 9 years ago:

Rick from CO posted over 6 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account