One measure of market valuation that has become widely popular is the CAPE, the cyclically adjusted price-earnings ratio. It was developed by Robert Shiller, a professor of economics at Yale University and author of “Irrational Exuberance” (Crown Business, 2006).

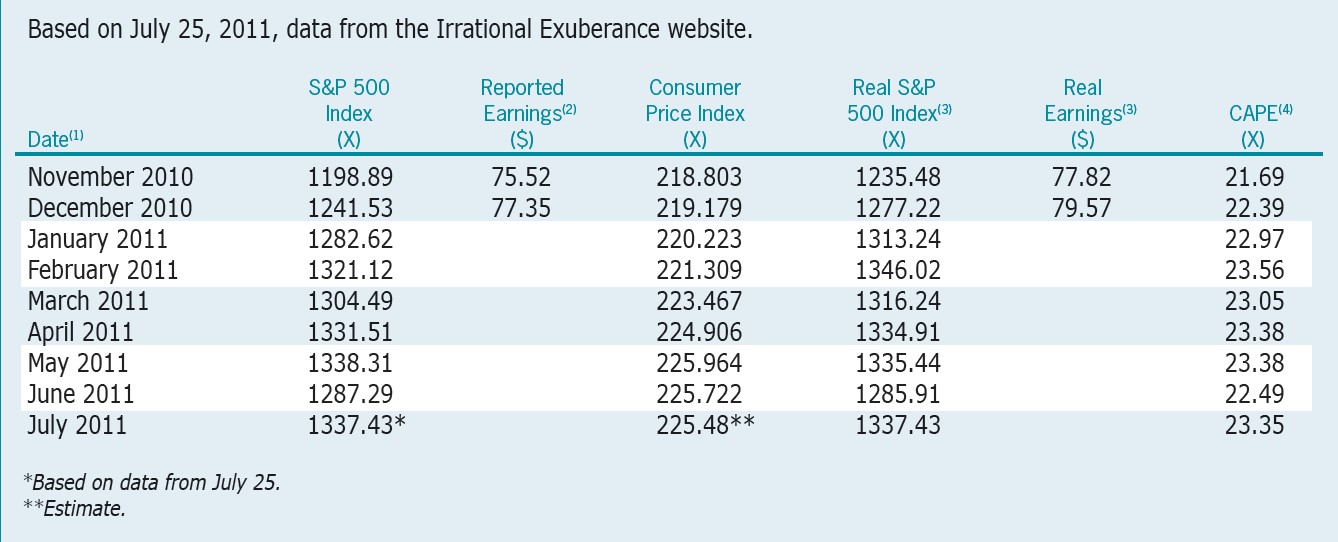

Shiller defines the numerator of the CAPE as the real (“inflation-adjusted”) price level of the S&P 500 index and the denominator as the moving average of the preceding 10 years of S&P 500 real reported earnings, where the U.S. Consumer Price Index (CPI) is used to adjust for inflation. The purpose of averaging 10 years of real reported earnings is to control for business cycle effects. Table 1 provides a detailed example of how the CAPE is determined.

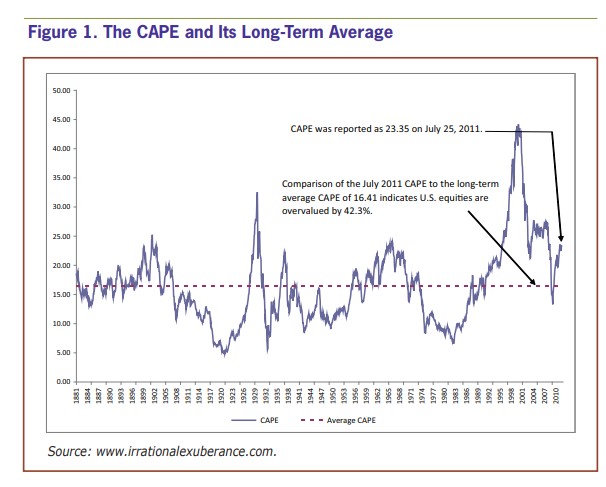

It is frequently suggested that the CAPE should be considered a mean-reverting series. As can be seen in Figure 1, the CAPE was reported as 23.35 during the month of July 2011 on the Irrational Exuberance website (www.irrationalexuberance.com). Per an analysis frequently used in practice, comparing the July 2011 CAPE to its long-term average of 16.41 indicates that U.S. stocks are currently overvalued by 42.3%.

In contrast, on July 22, 2011, Standard & Poor’s reported a price-earnings ratio of 16.17 based on reported earnings for the S&P 500 index. The price-earnings ratio based on operating earnings (which excludes write-offs and other special items) was 14.84. Both of these measures are well below their average since the fourth quarter of 1988, which suggests that stocks are certainly not overvalued to the degree predicted by the CAPE analysis and may actually be undervalued. Thus, investors are left in a quandary as to which measure of valuation is most appropriate.

This article makes the case that the comparison of the July 2011 CAPE to its long-term average provides an overly bearish view of the stock market and that the traditional price-earnings ratio based on either reported earnings or operating earnings is a better measure of the worth of U.S. equities in July 2011. As first used by Shiller in his book, the CAPE was undoubtedly a very useful tool for identifying overvaluation at the height of the late-1990s stock market “bubble.” However, like all other valuation metrics, the CAPE has its limitations, and these limitations derive from how it is computed.

The Length of the Business Cycle

In their classic 1934 book “Security Analysis,” legendary investors Benjamin Graham and David Dodd noted that traditionally reported price-earnings ratios can vary considerably because earnings are strongly influenced by the business cycle. To control for cyclical effects, Graham and Dodd recommended dividing price by a multi-year average of earnings and suggested periods of five, seven or 10 years. Following the Graham-Dodd recommendation, Shiller uses a 10-year moving average of earnings in computing the CAPE.

The problem with this assumption is that the typical or average business cycle has been significantly shorter than 10 years. According to data compiled by the National Bureau of Economic Research, economic contractions have become shorter and expansions longer in recent years. Furthermore, while the business cycle has lengthened in recent years, it is still considerably shorter than 10 years. Measured trough to trough, the average business cycle has been six years and one month for the most recent 11 cycles. Measured peak to peak, the average is five years and six months.

The problem with using a moving average that is longer than the business cycle is that it will overestimate “true” average earnings during a contraction and underestimate “true” average earnings during an expansion. According to the National Bureau of Economic Research, the last recession ended in June 2009 and the U.S. economy is now in an expansion phase. Thus, the average earnings estimate used by the July 2011 CAPE is too low and produces a bearishly biased estimate of value.

Using Shiller’s data, a July 2011 CAPE based on the average of six years of real earnings is 21.26 and the long-term average CAPE based on the average of six years of real earnings is 15.78. Comparison to this average indicates that stocks are overvalued by 34.7%. While still signaling that stocks are overvalued, the degree of overvaluation is much less than the 42.3% estimate provided by the July 2011 CAPE based on a 10-year average of real earnings.

Table 1. Computation of the CAPE

Notes:

- Shiller’s data set begins in January 1871.

- Earnings are reported quarterly and reflect the last four quarters of data. The CAPE uses a linear weighting to determine monthly earnings and does not use earnings estimates but relies on actual data. Reported earnings for first quarter 2011 were not included in the July 25, 2011, CAPE computation.

-

The S&P 500 index and reported earnings are adjusted for inflation using the U.S. Consumer Price Index where real values reflect July 2011 purchasing power. For example:

December 2010 real earnings = $77.35 × (225.48 ÷ 219.179) = $79.57

July 2011 real S&P 500 index = 1337.43 × (225.48 ÷ 225.48) = 1337.43 - The CAPE is computed as the real S&P 500 index divided by the arithmetic mean real earnings over the previous 10 years. For example, the CAPE of 22.39 in December 2010 is the real S&P 500 index in December 2010 of 1277.22 divided by the average real earnings from December 2000 through November 2010. The CAPE of 23.35 in July 2011 is based on the average real earnings from July 2001 to December 2010 because reported earnings for first-quarter 2011 were not included in the July 25, 2011, analysis. If an S&P first-quarter 2011 estimate of $81.31 for trailing four-quarter reported earnings had been included in the analysis, the July 25, 2011, CAPE would have been reported as 23.10 rather than 23.35.

Measuring Inflation

Because earnings and prices are converted to current-period dollars in determining the CAPE, changes in inflation theoretically should not alter its long-term average. However, problems can arise if the method used to measure inflation changes over time. This has indeed been the case, as the Bureau of Labor Statistics frequently changes the manner in which the Consumer Price Index is determined.

Two fairly recent methodological changes to the index have been especially significant. In January 1999, the Bureau of Labor Statistics began using a geometric mean formula in the calculation of most of the basic indexes. The second change took place over a period of years beginning in 1998, when the Bureau of Labor Statistics expanded its use of hedonic regression models for quality adjustments. [Editor’s note: Hedonic models estimate values for individual components that are bundled together.]

According to the bureau, the changes removed biases that caused the Consumer Price Index to overstate the inflation rate. The report that served as the catalyst for the two previously noted changes came to the conclusion in December 1996 that the index was overstating the rate of inflation by 0.8 to 1.6 percentage points a year. The study’s central estimate was an overstatement of 1.1% per year.

Although the best methodology for determining consumer inflation continues to be a hotly debated topic, most agree that the overall result of these recent changes is a lower Consumer Price Index. For example, research from the Bureau of Labor Statistics claims that the use of the geometric mean formula has by itself lowered the CPI measure of inflation by approximately 0.3%. There is also a popular investment website that claims an approximate 7% difference in the annual CPI inflation rate based on methodological changes over the last couple of decades, including the two changes previously mentioned.

The problems that the changes in the measurement of the index create for the CAPE are twofold. First, there is the general “apples-to-oranges” problem as the construction of the index used to determine real earnings and real prices as inputs for the CAPE has changed numerous times since 1871, the first year in Shiller’s data set. Secondly, if one believes that the current methodology produces a lower estimate of inflation, then the current CAPE needs to be adjusted downward to make it comparable to earlier estimates.

In determining the CAPE, reported earnings are adjusted for inflation using the Consumer Price Index, where real values reflect current-period purchasing power. Thus, any upward adjustment to the current-period Consumer Price Index would produce a series of higher real earnings and, therefore, a lower CAPE.

Accounting and Tax Issues

Another problem faced by those making valuation judgments using the CAPE time series is that both accounting standards and corporate taxation policies have changed significantly over time. While Shiller’s data set begins in 1871, the first U.S. national accounting society was not formed until 1887. Thus, public accounting in the U.S. was still in its infancy in the late 1800s, and it should be considered questionable how useful these early earnings numbers are to any analysis that uses them as inputs.

In the early 1900s, U.S. accounting practices typically focused on the presentation of the balance sheet. Balance sheets were drafted mainly to satisfy bankers who were making working capital loan decisions and who cared more about a company’s liquidity than its long-term profitability and solvency. The cash basis of accounting was a widely used means of financial reporting during this time period and it required that firms wait to recognize revenues and expenses until the corresponding cash flows actually occurred. Today, all businesses incorporated in the U.S. must make use of accrual accounting, where revenues and expenses are accounted for when they are incurred, rather than later when cash actually changes hands.

Business practices in the U.S. began to change dramatically in the late 1920s. Bank credit deteriorated in response to the Great Depression, and numerous banks failed. Businesses began to seek financing directly from investors, and corporate stock issuance became a major source of financing. As investors began to replace bankers as the primary users of financial statements, the income statement began to take center stage.

Other factors, such as the rise of income taxation and cost accounting, also shifted the focus to revenues and expenses. In the U.S., the corporate income tax dates back to the Corporation Tax Act of 1909, which instituted an excise tax on corporations based on their income. In 1913, the 16th Amendment to the Constitution made the income tax a permanent fixture of the U.S. tax system. The top corporate marginal tax rate was just 1% from 1909 through 1915 and then gradually rose to 19% in 1938–1939. Thus, corporate income either wasn’t taxed or was taxed at a comparatively low rate for the first 69 years of Shiller’s earnings data.

Corporate taxes rose rapidly during the World War II and Korean War eras. The corporate tax rate on the highest taxable income bracket reached a peak of 52.8% in 1968–1969. The rate has since gradually declined and is at 35% for 2011. In the 1950s, revenue from the federal corporate income tax averaged about 5% of gross domestic product per year. Last decade, corporate tax revenue averaged about 2% of gross domestic product annually, and it is expected to be only about 1.3% in 2011.

Historians usually trace cost accounting concepts in the U.S. back to the late 19th century and the Industrial Revolution. Academics claim, however, that it wasn’t until the 1940s that management accounting techniques began to be taught in the classroom. Activity-based management and costing and interdepartmental cost allocation coverage were substantially new changes in accounting textbooks during the late 1980s. Thus, what informed observers consider modern cost accounting practices were only in place for the last few decades of Shiller’s earnings data.

The passage of the Securities Act of 1933 and the Securities and Exchange Act of 1934 ultimately granted authority to prescribe accounting methods to the newly established U.S. Securities and Exchange Commission (SEC) and required that financial statements filed with the SEC be certified by an independent public accountant. In 1938, the SEC delegated much of its authority to dictate accounting practices to the American Institute of Accountants and its Committee on Accounting Procedures. In 1939, the committee issued its first of 51 Accounting Research Bulletins.

Due to criticism of the committee, the American Institute of Certified Public Accountants replaced it with the Accounting Principles Board in 1959. The board was designed to issue accounting opinions after it had considered previous research studies, and it issued its first of 31 opinions in 1962. In 1973, the Financial Accounting Standards Board (FASB) was formed and it has since issued 168 Statements. Effective July 1, 2009, the Accounting Standards Codification is considered the single source of authoritative U.S. generally accepted accounting principles (GAAP). The codification organizes the many pronouncements that constitute U.S. GAAP into a consistent, searchable database.

The key point to be taken from this brief history of U.S. accounting and corporate taxation is that reported earnings from different time periods are not that comparable for the simple reason that accounting standards, accounting practices, and tax policies have changed considerably. And it certainly seems Greek philosopher Heraclitus’ model of the world, “nothing endures but change,” will fit the future. Accounting practice in the U.S. appears to be headed toward more fair value accounting standards (see next section). Accounting rule-makers are also trying to move U.S. GAAP and International Financial Reporting Standards (IFRS) closer together. IFRS are generally considered to be more principles-based and allow companies to use judgment while applying a set of guidelines.

This discussion should lead one to question the assertion that the CAPE should be expected to mean-revert precisely to its long-term average of 16.41. How can anyone seriously believe that a high-quality comparable for the CAPE of any time period is its long-term average, given that many of the major factors affecting reported earnings are peculiar to specific time periods? Reported earnings from 1871 are not truly comparable to those in 1941, and both of those are not truly comparable to reported earnings in 2011. Thus, a very-long-term time series evaluation of any price-earnings ratio, including the CAPE, should be considered problematic.

Fair Value Accounting

The purpose of this section is twofold. First, it shows how a change in accounting standards can materially impact reported earnings. Second, it provides another reason why the comparison of the July 2011 CAPE to its long-term average presents an overly bearish estimate of the worth of U.S. equities.

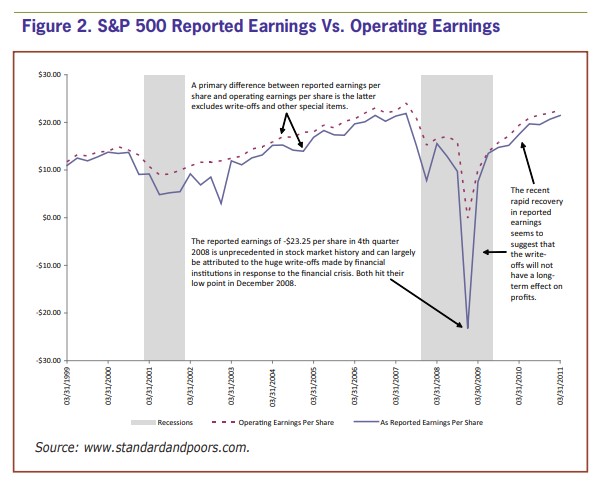

SFAS 157 Fair Value Measurements was issued in September 2006 by FASB and became effective for entities with fiscal years beginning after November 15, 2007. The greatest recent impact of this statement was on “available for sale” investment securities held by banks during the recent financial crisis: These securities must now be reported at fair value each accounting period. The recognition process requires adjustments to the value of these securities as they appear on the balance sheet. The adjustments, in turn, result in the recognition of unrealized gains and losses in reported earnings.

Banks held a significant percentage of assets as investment securities at the beginning of the financial crisis—over $198 billion of mortgage-backed securities were held by large U.S. banks in July 2008. The crisis initially affected securities backed by low-quality subprime mortgages, but it ultimately adversely affected virtually the entire spectrum of non-Treasury fixed-income securities. Quite obviously, there were heightened levels of risk aversion, and some security markets were very illiquid at the peak of the crisis. Bank investment portfolios were clobbered, and the new fair value accounting laws required banks to include these losses in reported earnings.

The timing of the huge unrealized losses in fourth-quarter 2008 matched almost perfectly the large downward move in reported earnings that occurred in the fourth quarter. Certainly the large write-down in the value of available-for-sale securities had a major negative impact on S&P 500 reported earnings.

Furthermore, except for one week, banks have had net unrealized gains on available-for-sale securities since April 21, 2010. This seems to suggest that the huge losses at the height of the financial crisis are unlikely to recur, at least in the short-term, foreseeable future. Yet the CAPE will continue to reflect the impact of these huge unrealized losses for the 10 years following their occurrence.

Figure 2 shows reported earnings per share and operating earnings per share for the S&P 500 from March 1999 to March 2011. Note how quickly reported earnings have recovered from the 2008 low.

Summary and Conclusions

By virtually anyone’s standards (including my own), Robert Shiller is a brilliant and accomplished economist. Likely due in no small part to Shiller’s literary successes, there are numerous investment companies and financial media firms that routinely refer to the CAPE as the “best” measure of equity valuation. This is unfortunate because some investors will respond to this rhetoric and act as if the CAPE always provides the best measure of the worth of equities. This isn’t true, and there will be times where the CAPE is actually a rather poor gauge of value—July 2011 being one of those times.

Comparing the July 2011 CAPE to its long-term average suggests that U.S. equities are 42.3% overvalued. This article presents reasons why that analysis gives an overly bearish assessment of the true worth of U.S. equities. For July 2011, a price-earning ratio based on either trailing 12-month reported earnings or trailing 12-month operating earnings provides a much better measure of value.

Data on the business cycle shows that the typical cycle is much shorter than the 10-year period over which real earnings are averaged to determine the CAPE. Because the CAPE is calculated with a moving average of real earnings that is too long, the July 2011 CAPE reflects reported earnings impacted by both the 2001 and 2007–2009 recessions. Thus, the July 2011 CAPE is using a downwardly biased estimate of “true” average real earnings.

Data used to determine CAPE is adjusted to current-period dollars based on the U.S. Consumer Price Index. To make accurate time series comparisons using a data set that is approaching 141 years in length, but is adjusted for inflation, requires a consistent measure of inflation. Changes have frequently been made to the index, and most believe the current methodology provides a lower estimate of inflation than earlier methodologies. If so, average real earnings used to determine the July 2011 CAPE need to be adjusted upward to make them comparable to earlier estimates.

The manner in which earnings are reported has changed significantly over time due to changes in accounting and tax policies. As a recent example, the move toward more fair value accounting standards resulted in security losses having a devastating effect on the reported earnings of financial institutions during the recent financial crisis. Yet that effect now appears to have been transitory. If an accounting item is deemed non-recurring, it is common practice in security analysis to ignore it when determining underlying earnings. But the CAPE continues to reflect the effect of non-recurring items for the 10 years that follow their initial recognition in reported earnings.

As first used by Shiller in his book “Irrational Exuberance,” the CAPE was a very useful tool for showing that U.S. equities were extremely overvalued in the late 1990s. But the seemingly ubiquitous approach of comparing the CAPE to its long-term average to determine a precise worth for U.S. equities is a flawed form of analysis. Changes in earnings and inflation reporting and the vagaries of the business cycle will frequently doom this sort of approach to failure.

Discussion

FREE REPORT

Get your free copy of our special

report analyzing the tech stocks

most likely to outperform the

market.

Edward from PA posted over 14 years ago:

G from MA posted over 14 years ago:

G from MA posted over 14 years ago:

C from RI posted over 14 years ago:

Jim from FL posted over 14 years ago:

John from FL posted over 14 years ago:

David Merkel from MD posted over 14 years ago:

Elio from IL posted over 14 years ago:

Elio from Uk posted over 14 years ago:

Steve from MN posted over 14 years ago:

D. from MD posted over 14 years ago:

Stephen from MN posted over 14 years ago:

Dominick from WA posted over 14 years ago:

Stephen from MN posted over 14 years ago:

James from OH posted over 14 years ago:

Stephen from MN posted over 14 years ago:

Jason from OH posted over 14 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account