It is highly likely that as a member of AAII you have savings or retirement money tucked away in a money market mutual fund (MMF), or indeed maybe more than one.

The Investment Company Institute (ICI), the trade association that speaks for the mutual fund industry, cited in its 2013 “Fact Book,” year-end 2011 data attributed to The IRA Investor Database showing that traditional IRA investors allocated 13.9% of their portfolios to money market funds while in their 30s and 13.9% when in their 60s. Overall, ICI stated that retirement account assets in money market funds totaled $379 billion in 2012.

Money fund investors are all given a fund prospectus that spells out the fund’s objective and what types of securities it is allowed to buy or specific security types it is not allowed to hold in its portfolio. The prospectus also covers the benchmark index used to measure investor returns, how the fund allocates its expenses, how to invest in the fund, and other pertinent information.

The prospectus and each accompanying marketing piece issued by a fund provider include some bullet points in bold type intended to make it as clear as humanly possible that a money market fund is an investment product and is not a bank product. Fund providers note in bold letters that a money market fund is not covered by bank insurance. Such communications also include an unambiguous, strong warning that there is a risk that you can lose money by investing in a money market fund. In fact, each fund offering typically includes language that is similar to this: “While the fund’s portfolios seek to maintain a stable net asset value of $1.00 per share, it is possible to lose money investing in the fund.”

Plus, money market funds are subject to regulation by the Securities and Exchange Commission under its Rule 2a-7 to the Investment Company Act of 1940.

These very clear pronouncements and current oversight apparently are not clear enough for a cadre of regulators, mostly on the banking side, or money fund critics who are provided soapboxes by media outlets. They seemingly will not be satisfied until every penny of the $2.6 trillion recently held in U.S. money market fund portfolios is redirected into federally insured bank accounts or the funds themselves are radically restructured. The suggested restructuring would morph money market funds into products equivalent to extremely short-term bond funds. Such a change would likely drive investors into alternative products that, in many cases, are beyond the reach of regulators and provide much less transparency than do money market funds.

Before we discuss the possible next steps affecting money funds and you as a money fund investor, let’s pause for a refresher about how and why they came into being.

A Brief History of Money Market Funds

Bruce R. Bent and a partner launched the first-ever money fund, called The Reserve Fund, in October 1971 with the goal of permitting any investor, large or small, to earn money market rates on their cash holdings. Bent often described his fund as being a “sleep-at-night” stable-value product. The fund was conservatively invested in short-term instruments that were deemed to be extremely safe. It was billed simply: “a dollar in, a dollar out with some interest,” though no guarantees were issued.

Over time, other companies introduced their own money funds, and checking privileges were added. In the super-inflationary period of the late 1970s and early 1980s, even banks created their own funds to stem deposit outflows to retail-oriented money funds, which resulted from mandated limits on allowed interest-rate payouts for banks’ savings products.

Taxable money market funds, which consist of government funds and prime funds, came first. They were later joined by tax-exempt money market funds. Government funds principally invest in “U.S. Treasury obligations and other financial instruments issued or guaranteed by the U.S. government, its agencies or instrumentalities,” according to the ICI. Prime funds, the ICI noted, “invest in a wider variety of high-quality, short-term money market instruments, including Treasury and government obligations, certificates of deposit, repurchase agreements, commercial paper and other money market securities.”

Tax-exempt or tax-free money market funds likewise seek to maintain a stable net asset value of $1 and invest in municipal money market securities. “The dividends of these funds are not taxed by the federal government, nor in some cases are they taxed by states and municipalities,” stated ICI.

Total assets of U.S. money market funds reached $1 trillion in August 1997 and smashed through the $2 trillion barrier in November 2001, iMoneyNet data recorded. The funds’ virtually unblemished success, the simplicity of keeping track of $1-per-share pricing and higher returns than offered by competing bank products, continued to attract investors seeking safe havens during periods of market turbulence or to set aside cash intended for future purposes, first primarily retail then later predominately institutional investors.

Tranquility in money-fund land was disturbed by the financial crisis of 2008 and the blowup of securities packaged with subprime mortgages issued in the U.S. This crisis led to European banks refusing to lend to one another, and the U.S. commercial paper and repurchase agreement (“repo”) markets seizing up. [Editor’s note: The International Capital Market Association defines a repo as an agreement where “one party sells an asset (usually fixed-income securities) to another party at one price at the start of the transaction and commits to repurchase the asset from the second party at a different price at a future date or (in the case of an open repo) on demand.”]

Tranquility disappeared when the first-ever money fund, which by then had been renamed as the Reserve Primary Fund, ran aground in mid-September 2008. Bent’s fund was caught holding large amounts of top-rated but suddenly worthless securities issued by Lehman Brothers when that firm unexpectedly filed for bankruptcy and was not included in a government rescue plan. The Reserve Fund thus became the first retail fund to “break the buck,” meaning its price fell below $1 per share. The fund ceased operations immediately and its shareholders ultimately received about $0.98 on each dollar invested. The fund’s demise prompted a thorough review of money fund structures and operations by the industry itself and by the SEC, which in January 2010 announced changes to Rule 2a-7.

“The SEC’s new rules are intended to increase the resilience of money market funds to economic stresses and reduce the risks of runs on the funds by tightening the maturity and credit quality standards and imposing new liquidity requirements,” the agency said.

Post-Financial Crisis Changes

Taxable funds since the phase-in of the SEC’s amended rules have been required to hold at least 10% of total assets in “daily liquid assets” and at least 30% of assets in “weekly liquid assets.” Liquidity provisions were added to meet reasonable requests by investors to cash in some or all shares. Basically, daily liquid assets are subject to a one-business-day demand feature and feature cash or U.S. Treasury securities, while the fund’s so-called weekly liquidity bucket consists of similar securities with remaining maturities of 60 days or fewer, or that mature or are subject to a demand feature within five business days.

All money market funds are now subject to periodic stress testing. They are also allowed to suspend redemptions if maintaining the “amortized-cost” $1.00 share price is believed to be problematic. Other rule changes include limitation to a 60-day maximum weighted-average maturity for all securities being held in portfolios (it was previously set at 90 days); institution of a new metric, the 120-day weighted-average life based on final maturity dates; and fresh curbs on investments in repos.

The SEC also required fund companies to supply the agency with detailed portfolio information and market-based value for each fund at the end of every month. Funds were additionally required to show investors, through monthly website postings, details about the securities in each fund’s portfolio. Such postings are supposed to appear within five business days after a month ends, enabling investors to better compare one fund’s makeup to another’s. Furthermore, the 2010 money market fund amendments also gave fund families until October 31, 2011, to be able to process transactions at a variable price other than $1 per share.

Proposed Additional Changes

The SEC chairman at the time, Mary Schapiro, made it known that while she was head of the regulatory body, she personally would continue to press for variable net asset values (NAVs) to supplant the long-established constant net asset value pricing for all funds. Her reasoning was that investors would be shown that pricing of the securities held in money fund portfolios fluctuates each day due to market forces. She feared that the share price of $1.00 was being misinterpreted by many as being a “bank-like” guarantee.

In August 2012, the SEC held up a planned discussion of mandating a floating net asset value for money funds and other suggested further changes to Rule 2a-7. This occurred after three of the five members requested a staff study about the funds’ ability to withstand financial upsets in Europe, the downgrading of U.S. government debt by a major rating agency and other market developments since the 2010 amendments were adopted. That report was issued on November 30, 2012.

In the meantime, Schapiro had taken her arguments for further money-fund regulation to the Financial Stability Oversight Council (FSOC), a body created by the Dodd-Frank Act on which she served due to her SEC position. Five of the 10 voting members of the FSOC regulate banks or depository-type institutions. Then-Treasury Secretary Timothy Geithner and Schapiro pushed through a package of several alternative structural reforms “to address the risks posed by money market funds” on November 13, 2012.

The FSOC continues to study assigning the systemic-risk label to money market funds and other so-called nonbanks operating in the “shadow-banking system.” The council first called for replacing the stable net asset value, based on amortized-cost accounting and/or penny rounding (see the box below for explanation), with a floating net asset value, which would not always be at $1 based on market values of securities held in a portfolio, a concept that the SEC had rejected several times previously after study.

SEC rules currently state that fund managers must “periodically ‘shadow price’ the amortized-cost net asset value of the fund’s portfolio against the mark-to-market net asset value of the portfolio. If there is a difference of more than one-half of 1% (or $0.005 per share), the fund’s board of directors must consider promptly what action, if any, should be taken, including whether the fund should discontinue the use of the amortized-cost method of valuation and re-price the securities of the fund below (or above) $1.00 per share, an event colloquially known as ‘breaking the buck.’”

Other ideas advanced by the FSOC for public comment included creating NAV buffers and delaying redemptions of the full amount of cash put in by investors of troubled funds for up to 30 days. The FSOC made clear it would send its final recommendations to the SEC for action, if it has not acted on its own.

Commissioner Troy Paredes, while appearing at the iMoneyNet Money Market Expo (MMX) on March 12, 2013, declared that “It’s paramount that money-fund reform be decided within the commission.” New SEC Chairman Mary Jo White, who officially assumed her role on April 10, 2013, stated at her Senate confirmation hearing that she believed securities regulators should set the future course for regulation of money funds, as they are investment products. SEC Commissioner Daniel Gallagher has been quoted as indicating that money-fund reform should be taken up by the commission within the next two months, or by mid-June 2013.

The SEC, for its part, has focused in the past on ways to discourage some investors from fleeing funds rumored to be in trouble. If some investors pulled out of perceived troubled money market funds, other slower-acting investors would be left to bear the costs of winding down an ill-fated fund.

“Fundamentally, we have to ask, ‘What are we solving for?,’ which explains the need to focus on data analysis, on the economics, and on the costs and benefits of any proposed reforms,” Paredes told the Money Market Expo audience in March. “If you think that what really happened was a massive run from risk, getting rid of the buck doesn’t solve the problem because a run-from-risk isn’t addressed by a floating NAV,” an apparent allusion to the failure of floating-NAV French money market funds at the height of the 2008 crisis. “If regulation solves the wrong problem and drives investors into less-regulated products, we will have damaged an enormously effective investment product, incurred substantial costs and created rather than mitigated risk in the financial system,” Paredes added.

Money market funds, meantime, continue to be the object of some media scorn. A March 29, 2013, commentary by MarketWatch columnist Rex Nutting claimed that money market funds are riskier than ever.

“Money market funds, thought to be one of the safest investments, are actually some of the most dangerous. They are still vulnerable to the same kind of bank run that nearly pushed the global economy over the brink in 2008, and there’s no plan by the industry or by its regulators to fix that vulnerability,” Nutting wrote. “Current U.S. law prohibits the kind of federal guarantee that, in 2008, stopped the bank run before it could bring down the financial system. The next run on these shadowy bank-like institutions could be fatal.”

Federated Investors, which runs the third-largest U.S. money market fund complex by assets, was quick to provide a rebuttal to Nutting’s piece, noting that 60 million investors as well as corporations and state and local governments understand the disclaimers cited earlier that money funds are investments and are not akin to banks. Money funds, Federated stated, unlike banks and other financial-services companies, did not need “to get rid of any toxic assets in the aftermath of Lehman’s bankruptcy, AIG’s rescue or other bailouts. Money fund portfolios were sound, but the global liquidity crisis prevented the funds from selling assets. The industry pleaded for liquidity in the system, not insurance for fund companies, it claimed.

The Federated response also faulted the MarketWatch columnist for ignoring the 2010 SEC reforms. The company argued that those reforms have proven to be effective in bolstering longstanding rules, while helping carry the funds through the Greek debt crisis, downgraded U.S. government debt, and debate over the U.S. budget and debt-ceiling impasse, covering all redemption requests as assets declined 10% during the summer 2011 events.

“Most recently, in January of this year [2013] money-fund industry leaders took additional steps and began publicly reporting the daily net asset [market] value of money market funds [also called the variable, ‘shadow’ or floating net asset value]—another initiative Mr. Nutting fails to mention. The bottom line is that money funds are well-regulated and the system, particularly in light of the 2010 amendments, is running smoothly,” Federated declared.

Brian Reid, chief economist at the ICI, while presenting at the Money Market Expo in March, pointed out differences between banks and money funds. “Banks have modest amounts of capital, heavy leverage, no explicit liquidity requirements, long-dated, illiquid, nonmarketable loans, with significant credit risk and almost no transparency about their assets and liabilities.” They are vulnerable to runs by depositors, he added. Money funds, by contrast “are not leveraged, have requirements to maintain mandated levels of liquidity and hold short-dated liquid, high-quality, marketable securities with minimal credit risk. They publish their portfolios monthly, and they are not guaranteed by the U.S. government.”

Funds are also able to routinely accommodate asset outflows because the short-dated securities they hold “trade in liquid and diverse markets. That type of volatility in a bank’s balance sheet would cripple it,” he commented.

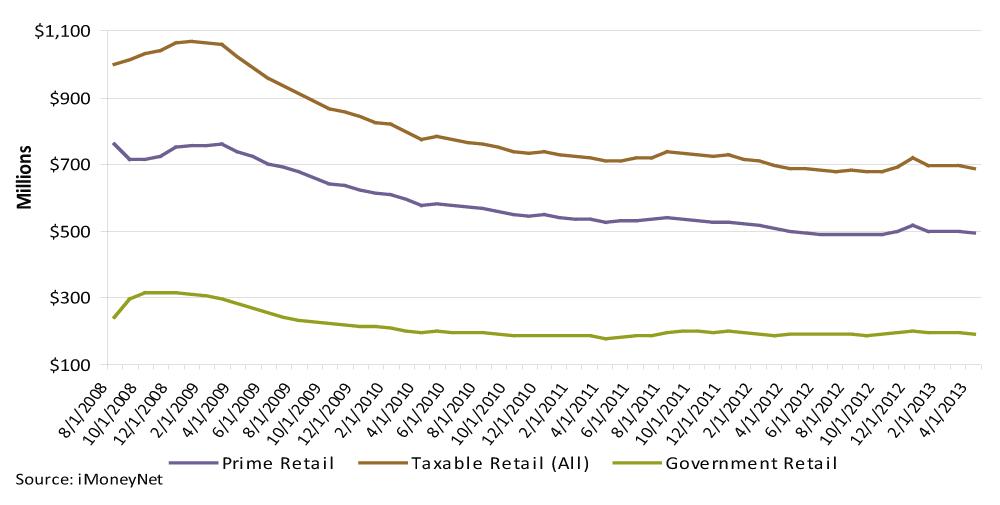

iMoneyNet portfolio holdings data demonstrates that prime retail funds are being operated even more conservatively than before the Reserve Fund’s collapse in September 2008. Holdings of U.S. Treasury and “other U.S.” government-backed securities have increased to a combined 17% of total assets as of April 9, 2013, up from a combined 9% on September 2, 2008. Holdings of commercial paper have been reduced, which is mainly due to reduced supply.

The SEC’s Paredes, answering questions at the iMoneyNet event, stated his belief that prime institutional funds, which sustained large outflows immediately after the Reserve Fund went down as investors sought safety in Treasury money market funds, should be the focus of “reform approaches” rather than retail, Treasury and tax-free money funds.

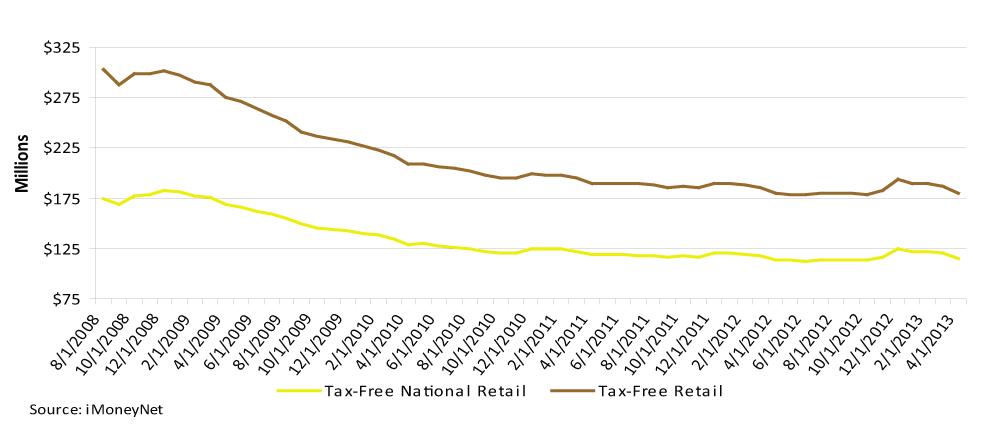

Figures 1 and 2 show that prime and government retail fund assets and tax-free retail fund assets tracked by iMoneyNet have dipped since August 2008, but the declines could be considered modest due to the prolonged near-zero interest-rate environment. The Federal Open Market Committee has held its federal funds target rate at between zero and 0.25% since December 2008.

Nancy Prior, president of Money Markets at Fidelity Investments, the largest money-fund complex with assets exceeding $415 billion, in an address at Money Market Expo, noted that “more than 450 banks have failed since the financial crisis began.” Prior argued that the 2010 SEC amendments “have made money market mutual funds more resilient. Further action is simply not warranted.”

She further observed, “A floating NAV is not the answer. It would impose burdensome tax, accounting and recordkeeping requirements for investors. Moreover, there is no evidence to suggest it would prevent outflows in a crisis. It won’t reduce risk in the system. Our customers have told us, loudly and clearly, that they have little or no interest in a product with a floating NAV or one that continually limits access to their funds.”

Prior urged regulators, as they press ahead, to narrowly focus on solving problems related to the ability of money market mutual funds to “sustain large, abrupt redemptions in times of severe market stress. Because Treasury, government, municipal and retail prime money market mutual funds do not pose the liquidity, credit and redemption risks that the FSOC and SEC have identified as a concern, these types of funds should be excluded from any additional reform measures,” she declared.

As that event in Orlando wrapped up, a consensus seemed to emerge that that would be the most likely avenue for the SEC to explore as it regroups under new leadership, with the FSOC watching closely as events proceed.

Conclusion

The SEC has taken steps supported by the industry to make funds “safer,” with evidence showing that fund portfolios are being run more conservatively than ever before. Many firms that did not operate money market funds as a core business have been weeded out of the industry due to low rates and the expenses associated with complying with the regulatory requirements added in 2010, making their continued fund operations uneconomical. Table 1 shows the highest-yielding retail money market funds as of May 7, 2013.

|

7-Day Compound Yield (%)* |

Assets ($ Mil) |

Phone Number | ||

| Government Retail Money Funds | ||||

| 1. Selected Daily Govt Fund/Cl D |

0.14

|

21.6

|

(800) 243-1575

|

|

| 2. Direxion US Govt MMF/Cl A |

0.09

|

20.0

|

(800) 851-0511

|

|

| 3. First Amer Govt Oblig/Cl A |

0.02

|

252.0

|

(800) 677-3863

|

|

| 3. Lord Abbett US Govt & Govt SE MMF/A |

0.02

|

547.1

|

(888) 522-2388

|

|

| Government Average |

0.01

|

|

||

| Prime Retail Money Funds | ||||

| 1. Invesco MMF/Investor Class |

0.09

|

168.5

|

(800) 659-1005

|

|

| 2. Meeder MMF/Retail |

0.08

|

68.1

|

(800) 325-3539

|

|

| 3. Schwab Cash Reserves |

0.06

|

35,904.6

|

(800) 435-4000

|

|

| 4. Capital Assets Fund/Preferred MMP |

0.05

|

1.8

|

(800) 730-1313

|

|

| 4. Delaware Cash Reserve/Class A |

0.05

|

222.2

|

(800) 362-7500

|

|

| 4. PNC Money Market Fund/Cl A |

0.05

|

265.6

|

(800) 622-3863

|

|

| Prime Average |

0.01

|

|

||

| Tax-Free National Retail Money Funds | ||||

| 1. Invesco Tax-Exempt Cash Fund/Inv |

0.20

|

8.5

|

(800) 659-1005

|

|

| 2. Alpine Municipal MMF/Inv |

0.08

|

214

|

(888) 785-5578

|

|

| 3. Vanguard Tax-Exempt MMF |

0.05

|

17,108.1

|

(800) 662-7447

|

|

| 4. PNC Tax-Exempt MMF/Cl A |

0.02

|

41.7

|

(800) 622-3863

|

|

| 4. Western Asset T-F Reserves/Cl N |

0.02

|

59.5

|

(800) 331-1792

|

|

| Tax-Free National Average |

0.02

|

|

||

| *Highest compounded (effective) rate of return to shareholders reported to Money Fund Report for the past seven days for period ended May 7, 2013. | ||||

| Source: iMoneyNet Inc., an Informa Financial company,Westborough, Mass. 01581; www.imoneynet.com. | ||||

The issue facing the industry and investors who rely on money funds is: Will regulators harm or kill a product that is admittedly not risk-free, in the interest of attempting to eliminate all risk? As Commissioner Paredes asked, “What are we solving for?”

Stable NAV Accounting Methods

Current money market fund regulation, SEC Rule 2a-7(a)(2) of the Investment Company Act of 1940, defines the amortized-cost method as “the method of calculating an investment company’s net asset value [per share] whereby portfolio securities are valued at the fund’s acquisition cost as adjusted for amortization of premium or accretion of discount rather than at their value based on current market factors.” Rule 2a-7(a)(20) defines the penny-rounding method of pricing as the method of computing a fund’s price per share “for purposes of distribution, redemption and repurchase whereby the current net asset value per share is rounded to the nearest one percent.”

Roger from Louisiana posted over 13 years ago:

harryrich from Ohio posted over 13 years ago:

Charles Rotblut from IL posted over 12 years ago:

John from Kentucky posted over 12 years ago:

Charles Rotblut from IL posted over 12 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account