Related

Financial Planning

By understanding the complexities and making smart claiming decisions, couples can add more to their lifetime benefits than singles can.

In this third article in a three-part series on claiming Social Security benefits, we discuss claiming strategies for married couples.

The good news for a couple is that they can often add more to their cumulative lifetime benefits than a single individual can by using a smart claiming strategy. The bad news is the claiming decision is much more complex. Much of the complexity revolves around the rules governing spousal benefits and survivor’s benefits.

The strategies in this article assume that no one besides the couple themselves can receive benefits based on either spouse’s earnings record. If children or parents can receive benefits based on the couple’s earnings record, the material presented here is not sufficient to make the claiming decision. The strategies further assume no pension is received by either spouse from work not covered by Social Security (e.g., public-school teachers, police officers, firefighters and other government employees). Finally, the strategies are based on the current promises of the Social Security system. The U.S. Congress may make changes at its discretion.

In last month’s article (“Social Security Strategies for Singles,” November 2013 AAII Journal Financial Planning column), we presented two of four key points for determining when to begin benefits. Couples will need to consider all four points as part of their decision process. The four key points are:

For clarity and to avoid the endless use of “his or her,” we assume the spouse and later widow is the wife. Spousal benefits are benefits the wife receives based on the husband’s earnings record when he is alive, while survivor’s benefits are benefits the wife receives based on her husband’s earnings record after he has passed. The rules are the same for a husband, however.

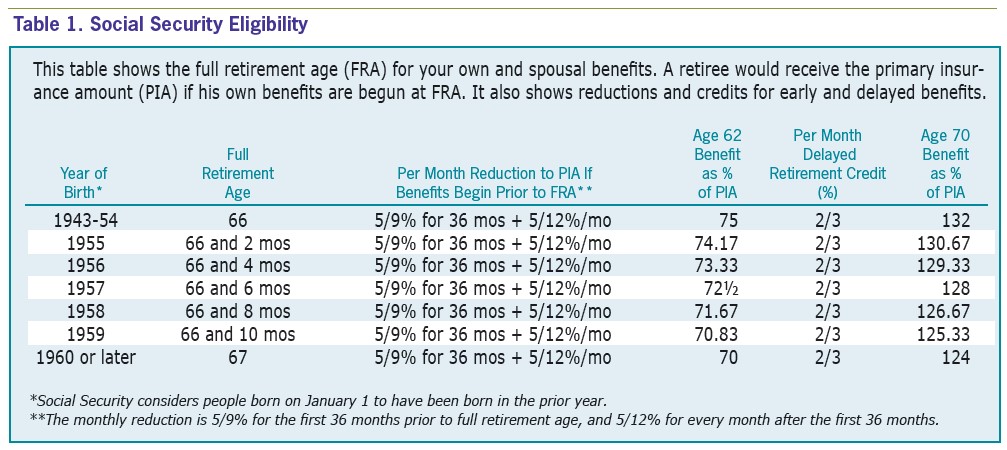

We begin this article with a brief review of survivor’s benefits. First, there is a separate full retirement age (FRA) for survivor’s benefits. The full retirement age we have previously discussed in this series of articles applies to benefits based on your own earnings record and spousal benefits; the full retirement age for survivor’s benefits applies to survivor’s benefits only. The full retirement age for survivor’s benefits is 66 for someone born in 1945 to 1957. It increases two months per year thereafter and is 67 for someone born in 1962 or later. (As we stated in the series’ first article (“Social Security Basics,” October 2013 AAII Journal), Social Security rules consider people to attain an age the day before their birthday. So, according to the Social Security Administration (SSA), someone born on January 1 has a full retirement age of someone born on December 31 of the prior year.)

Second, survivor’s benefits can begin at 60. If claimed at 60, the reduction is 28.5%. If begun at full retirement age for survivor’s benefits or later, it is the full survivor’s benefit. If survivor’s benefits are begun between age 60 and the full retirement age for survivor’s benefits, the reduction is a pro rata share of the maximum reduction of 28.5%. There are no delayed retirement credits earned by delaying survivor’s benefits beyond full retirement age for survivor’s benefits.

Third, if the widow is at least age 70 at the death of her husband, the wife/widow will generally receive the larger of her own benefits or her unreduced survivor’s benefits, where her survivor’s benefit is usually her husband’s benefit amount at his death (but it can be a higher amount). Since most widows are at least 70 when their husband dies, this statement covers most cases. If the widow is younger than 70, it may not be in her best interest simply to continue the higher of her own benefits or her survivor’s benefits. Due to space limitations, we cannot cover those strategies in this article. For more information, read our book, “Social Security Strategies” (2011).

Claiming strategies for couples often revolve around spousal benefits. Rules governing spousal benefits include the following:

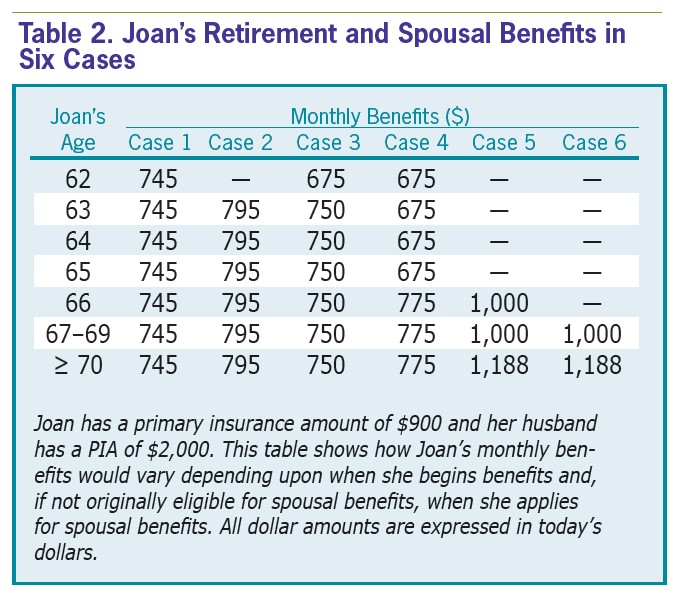

An example covering six cases should help clarify spousal benefits. Suppose Joan is age 62 with a primary insurance amount of $900, and Bill is age 65 with a primary insurance amount of $2,000. Both have full retirement ages of 66. Table 2 summarizes the cases. All dollar amounts are expressed in today’s dollars.

Case 1: If Bill has already begun benefits, Joan can apply for spousal benefits today. Since she is younger than her full retirement age, but eligible for spousal benefits, she is deemed to be applying for both her own retirement benefits and spousal benefits. At 62, the benefit based on her earnings record is $675 a month, [75% × $900] as explained in Table 1, which shows the age requirements for Social Security eligibility and is republished from the aforementioned first article in this series in the October 2013 issue. Her spousal benefit at 62 is $70 [70% × ($1,000 – $900)], where $1,000 is the base spousal benefit (that is, half his primary insurance amount), $900 is her primary insurance amount, so ($1,000 – $900) is her unreduced spousal benefit. She only receives 70% of this amount because she is applying for spousal benefits 48 months before attaining full retirement age. The reduction to 70% is calculated as 70% = 1 – (25/36% × 36 months) – (5/12% × 12 months) since she is starting spousal benefits 48 months before attaining full retirement age. So, she receives $745, which is $675 (her own benefit at 62) + $70 (her spousal benefit at 62).

Case 2: Bill has not already begun benefits. One year hence at his full retirement age, he files and suspends benefits based on his earnings record. If Joan files at that time at 63, she is deemed to be applying for both her own benefits and spousal benefits because she is eligible for both. Benefits based on her earnings record are $720 a month (80% × $900). Spousal benefit at 63 is $75, or 75% × ($1,000 – $900). The ($1,000 – $900) is her unreduced spousal benefit, but she only receives 75% of this amount because she is applying for spousal benefits 36 months before attaining full retirement age. So, her total benefit is $795, which is $720 + $75.

Case 3: Joan files today at 62. Since Bill has not filed for benefits, Joan is not yet eligible for spousal benefits. Today, she begins her own benefits of $675 a month as explained in Case 1. In one year, he files and suspends, which makes her eligible for spousal benefits. She files for spousal benefits at age 63 and receives $75 [75% × ($1,000 – $900)] in spousal benefits, where 75% is her spousal benefits fraction when applying 36 months before attaining full retirement age as explained in Case 2. Her total benefits at 63 are $750, or $675 (her own benefits at 62) + $75 (her spousal benefits at 63).

Case 4: Like Case 3, Joan files today at 62. Since she is not yet eligible for spousal benefits, she begins retirement benefits based on her earnings record of $675 a month. In one year, Bill files and suspends, which makes her eligible for spousal benefits. However, unlike in Case 3, Joan defers spousal benefits until she attains full retirement age. At full retirement age, she begins spousal benefits and receives $775. The calculation is $675 (for her own benefits at 62) + ($1,000 – $900) in additional spousal benefits, where ($1,000 – $900) is her unreduced spousal benefit at full retirement age. She gets this full unreduced spousal benefit because she applied for it at full retirement age or later. In short, as in Case 3, Joan may add spousal benefits when Bill files and suspends his benefits, but as in Case 4 she may also delay adding spousal benefits until a later date, which would likely be at her full retirement age.

Case 5: If Joan applies for benefits at full retirement age (66) and Bill has filed for his benefits, she will receive a $900 retirement benefit based on her record + $100 spousal benefit, [$1,000 – $900], for a combined benefit of $1,000 a month. However, she should make a restricted application for spousal benefits only of $1,000 a month, half of his primary insurance amount. Then, when she turns 70, she can switch to benefits based on her earnings record of $1,188, [132% of $900], where 32% reflects her delayed retirement credits. Warning: If, at full retirement age, Joan does not restrict her application to a “spouse only” benefit, the Social Security Administration will likely assume she is applying for her $900 retirement benefit + $100 spousal benefit. In this case, she would not be able to switch at 70 to $1,188 because she would not receive the delayed retirement credits since she began her own benefits at full retirement age.

Case 6: If Joan applies for benefits at 67 (and Bill has filed for his benefits), she will receive $972 retirement benefits based on her record, which reflects 12 months of delayed retirement credits, plus $28 in spousal benefits, [$1,000 – $972], for a combined benefit of $1,000 a month. As discussed in Case 5, at 67 Joan should restrict her application to a “spouse only” benefit of $1,000, half of Bill’s primary insurance amount. Then, when she turns 70, she can switch to her retirement benefit of $1,188, which is 132% of $900.

In short, let’s consider two situations. First, if Joan makes a restricted application for spousal benefits only after attaining full retirement age, her spousal benefit will be the base spousal amount, half of Bill’s primary insurance amount. Second, Joan applies for her retirement benefits before full retirement age and applies for spousal benefits on or after the date she applies for her retirement benefits. In equation form, her retirement benefit = her primary insurance amount × reduced benefit factor, where the reduced benefit factor is less than 1 as explained in Table 1. In equation form, her spousal benefit = (base spousal benefit – her primary insurance amount) × spousal reduction factor, where the spousal reduction factor is less than 1 if she applies for spousal benefits before full retirement age and 1 if she applies at full retirement age or later. In such situations, both retirement benefits and spousal benefits are calculated separately, reduced separately when applicable with their own reduction factors, and then added together.

Two lessons apply to couples. In addition, as we shall see, Lesson 1 also has implications for couples. So we repeat it here. For clarity, we assume the husband has the higher primary insurance amount, but the rules are the same if the wife has the higher primary insurance amount.

Lesson 1: If a single individual lives to age 80, the cumulative lifetime benefits will be approximately the same no matter what age benefits begin.

Lesson 2: The relevant life expectancy for the decision as to when the spouse with the higher primary insurance amount should begin benefits based on his earnings record is the life expectancy of the second spouse to die, while the relevant life expectancy for the decision as to when the spouse with the lower primary insurance amount should begin benefits based on her record is the life expectancy of the first spouse to die.

Consider a married couple, both age 62. Assume the husband has a primary insurance amount of $2,000, while his wife has a primary insurance amount of $700. They both have full retirement ages of 66 for all benefits. How long will payments last for benefits based on his earnings record, and how long will payments last for benefits based on her record? After the death of the first spouse—and it doesn’t matter which spouse dies first—the surviving spouse gets the higher earner’s benefits. So, benefits based on the higher earner’s record will continue until the second spouse dies. Therefore, the relevant life expectancy for the spouse with the higher primary insurance amount is the life expectancy of the second spouse to die. Now, let’s consider the claiming strategy for the spouse with the lower primary insurance amount. She can begin benefits at any age between 62 and 70. But how long will benefits based on her earnings record last? The answer is that these benefits will last until the first spouse dies. Thus, the relevant life expectancy for the decision as to when the lower primary insurance amount spouse should begin benefits is the life expectancy of the first spouse to die.

Lesson 3: If at least one spouse lives well beyond the age when the spouse with the higher primary insurance amount would turn 80, then the couple’s cumulative lifetime benefits will be higher if he delays benefits based on his record until age 70.

We present an example that will lead a couple to making an informed claiming decision. However, as we shall see, an informed decision is not always an optimal decision.

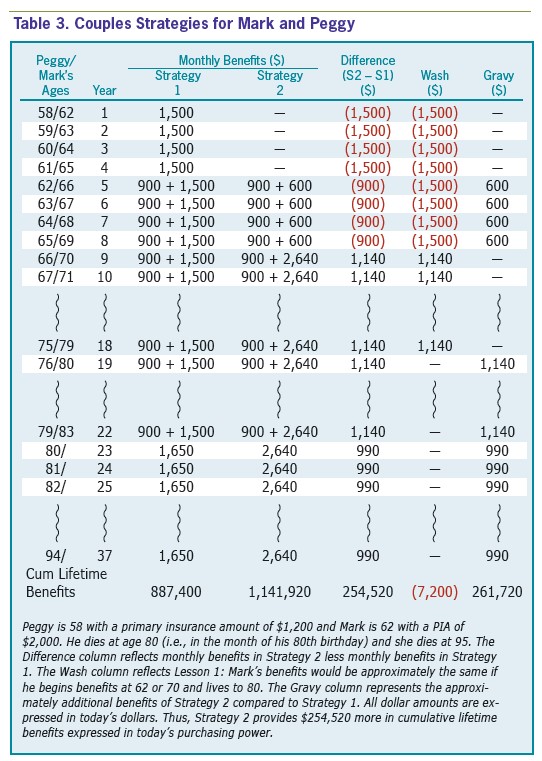

Mark, age 62, has a primary insurance amount of $2,000 and Peggy, age 58, has a primary insurance amount of $1,200. They both have full retirement ages for all benefits of 66. Mark has a life expectancy of 84 and Peggy has a life expectancy of 95. For simplicity, we assume their first month of benefits would be paid in January so there are 12 monthly payments in the first year. Table 3 summarizes two of their claiming strategies. All dollar amounts are expressed in today’s dollars. For example, monthly benefits may rise from $1,500 in one year to $1,530 the next year due to a 2% cost of living adjustment (COLA), but prices would also be 2% higher. Thus the $1,500 would remain constant when expressed in today’s dollars. Also, based on the real yield of approximately 0% on Treasury Inflation-Protected Securities (TIPS) at the time we are writing this article, the present value of this $1,530 is $1,500.

In Strategy 1, they both begin benefits at 62. Mark receives $1,500 a month for the first four years. Then Peggy turns 62 and receives $900 a month for a combined monthly benefit of $2,400. After Mark dies (estimated at age 84 when Peggy would be 80), Peggy receives $1,650 a month until her death. Her higher benefits reflect a little-known rule whereby, because he applied for benefits before full retirement age and she is older than full retirement age for survivor’s benefits at his death, she gets the larger of his $1,500 or 82.5% of his primary insurance amount, which is $1,650.

In Strategy 2, Peggy begins benefits in four years, when she turns 62, of $900 a month and Mark begins spousal benefits only at that time of $600 a month, half of her primary insurance amount; since Mark has attained full retirement age, he can file for spousal benefits only and later switch to benefits based on his earnings record. When Mark turns 70, he switches to benefits based on his earnings record of $2,640 a month. After Mark’s death, Peggy retains his $2,640 monthly benefits.

The Difference (S2 - S1) column in Table 3 shows the difference in monthly benefits between Strategy 2 and Strategy 1. The columns labeled Wash and Gravy separate this Difference column into two components. The Wash column shows the difference between Mark’s benefits if he was single, lived until age 80, and began benefits at 70 instead of 62. As we stated in last month’s article, if a single individual lives to age 80, the cumulative lifetime benefits will be approximately the same no matter what age benefits begin. The Wash column reflects this lesson. By delaying his own benefits from 62 until 70, he loses $1,500 a month for eight years but gets an extra $1,140 a month for 10 years—these amounts are approximately offsetting. Therefore, the column labeled Gravy represents the approximate additional cumulative lifetime benefits from Strategy 2 compared to Strategy 1. In terms of cumulative benefits, these Gravy components are like free goods.

The Gravy column contains two components. The first is Mark’s $600 a month in spousal benefits from his full retirement age through age 69. A study by Munnell, Golub-Sass, and Karamcheva (“Strange but True: Claim Social Security Now, Claim More Later,” Center for Retirement Research, April, no. 9-9, 2009) called this the claim-now-and-more-later advantage. By delaying benefits based on his earnings record from age 62 until 70, he gets the additional $1,140 a month. From Lesson 1, $1,500 a month from age 62 until Mark turns 80 is comparable to $2,640 a month from age 70 until 80. However, he also gets the $600 a month in spousal benefits, which is like a free good. The second component of the Gravy column is the additional $1,140 a month beginning when Mark turns 80 until he dies at 84 and then the additional $990 a month until the second partner dies, in this case Peggy when she turns 95. In one of our research reports (“Social Security: When to Start Benefits and How to Minimize Longevity Risk,” Journal of Financial Planning, vol. 23, no. 3, 49-59, 2010), we called this the joint-lives advantage. Notice that the time horizon of this joint-lives advantage is from the time the spouse with the high primary insurance amount, Mark, would have been 80 until the death of the second spouse. Furthermore, if Peggy was, say, 10 years younger than Mark or she had an especially long life expectancy, this advantage will tend to be even larger since it would last until the second spouse dies.

The example illustrates that the relevant life expectancy for the benefits of the spouse with the higher primary insurance amount is the lifetime of the second partner to die. Peggy receives survivor’s benefits based on the higher primary insurance amount spouse’s earnings record, and this payment continues until the death of the second spouse. From Lesson 3, as long as at least one spouse lives well beyond the age when the spouse with the higher primary insurance amount would be 80, then the higher primary insurance amount spouse should delay benefits based on his record until 70.

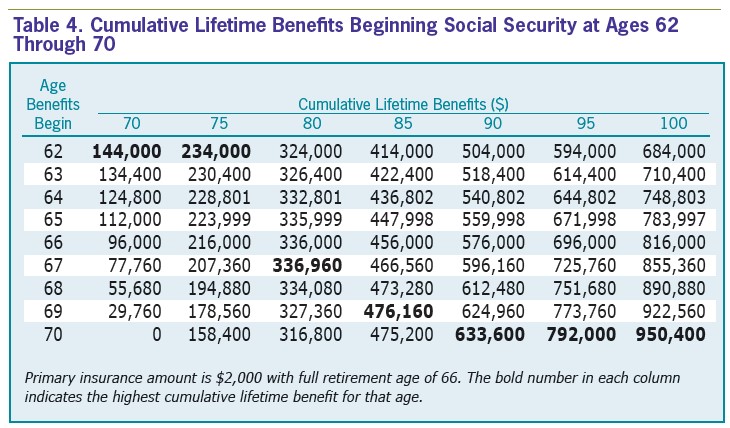

The second half of Lesson 2 says that Peggy’s benefits only last until the first spouse dies. Based on life expectancies, Peggy would be 80 when Mark dies. From Lesson 1, her cumulative benefits are approximately the same no matter what age benefits begin. In fact, from Table 4, it appears that she should begin her benefits at age 67 because this is the age (rounded to nearest whole year) when cumulative lifetime benefits based on her record would be maximized. Thus following Lesson 2, Mark and Peggy might follow Strategy 3, where Mark begins his benefits at 70 and Peggy begins her benefits at 67. We call this an informed strategy. Although not shown in the table, Strategy 3 would provide about $233,500 more cumulative lifetime benefits than Strategy 1. However, Strategy 3 would provide about $21,000 less in cumulative lifetime benefits than Strategy 2. In Strategy 2, Peggy begins benefits at 62, which makes Mark eligible for four years of spousal benefits of $600 a month. If she waits until she is 67 to start benefits, Mark would not receive spousal benefits. Whether Mark receives spousal benefits and, if so, the size of these monthly benefits depend upon their relative ages and the sizes of their primary insurance amounts. Furthermore, if the relative sizes of their primary insurance amounts were different or if Peggy was older, the best strategy may be yet another strategy.

This example illustrates that following the advice embedded in Lessons 1 through 3 leads to an informed claiming strategy. But this informed strategy is not always the optimal strategy.

We emphasize four key points in our series that will help most single individuals and couples make informed decisions as to when to claim Social Security benefits.

Unfortunately, following these four points will not always lead to an optimal claiming decision. The latter requires a detailed understanding of rules governing spousal and survivor’s benefits and lots and lots of hours studying their implications and how they apply to each specific situation.

Nevertheless, we have shown that following these four points can materially affect the financial well-being of a single retiree or retired couple.

Financial Planning

Financial Planning

Charles M. from NY posted over 12 years ago:

P Chiaravalli from MI posted over 12 years ago:

Robert Mann from MI posted over 12 years ago:

Randy T from Delaware posted over 12 years ago:

Bob G from CO posted over 12 years ago:

Herbert Ng from CA posted over 12 years ago:

Norm L from Massachusetts posted over 12 years ago:

Mian from FL posted over 12 years ago:

Kenton Kelly from MN posted over 12 years ago:

Bob G from CO posted over 12 years ago:

John Samsell from WA posted over 12 years ago:

Mark Gaines from CA posted over 12 years ago:

Tim Soles from TX posted over 12 years ago:

George Bradshaw from NC posted over 12 years ago:

Jack from OH posted over 12 years ago:

David Dudley from CT posted over 12 years ago:

David Dudley from CT posted over 12 years ago:

Ken Owenby from GA posted over 12 years ago:

Mark Landt from CO posted over 12 years ago:

George from WI posted over 11 years ago:

Christopher Viscomi from VT posted over 10 years ago:

D Randall Spydell from CO posted over 10 years ago:

Eric Tarini from MA posted over 10 years ago:

Tony Hausner from MD posted over 10 years ago:

Charles Rotblut from IL posted over 10 years ago:

john bates from california posted over 10 years ago:

Thomas from IL posted over 10 years ago:

Charles Rotblut from IL posted over 10 years ago:

You need to log in as a registered AAII user before commenting.

Log InCreate an account